Rocket Lab Corporation (NASDAQ: RKLB) has grown from a niche small-satellite launch company into one of the world’s leading publicly traded space technology companies. Founded in 2006 by aerospace engineer Peter Beck, the company has successfully diversified beyond rocket launches by manufacturing satellites, spacecraft components, and providing end-to-end space systems for commercial, civil, and defense customers. Its Electron rocket has become one of the most frequently launched small orbital launch vehicles, while its next-generation Neutron rocket is expected to significantly expand the company’s capabilities in the medium-lift launch market.

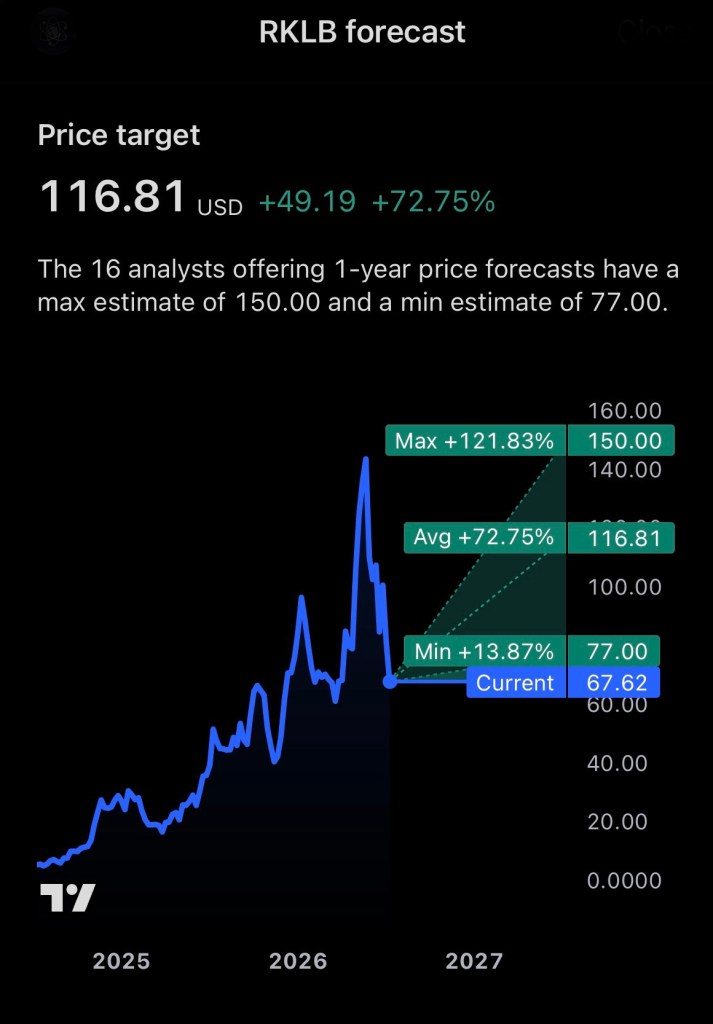

Rocket Lab shares closed at $67.62 on Friday, July 17, 2026, recovering slightly after a volatile week that saw the stock decline more than 11% on July 16. Despite the recent correction, the company remains one of the fastest-growing names in the commercial space industry, with investors closely watching several major catalysts that could influence its long-term trajectory.

Reasons for Long-Term Upside

Neutron Rocket Development

The single largest catalyst for Rocket Lab is the development of its reusable Neutron launch vehicle. Designed to compete for larger commercial, government, and national security missions, Neutron has the potential to dramatically increase Rocket Lab’s revenue opportunities while improving launch economics. Successful execution could transform Rocket Lab from a niche launch provider into a direct competitor within the medium-lift launch market.

Diversified Revenue Streams

Unlike many emerging space companies, Rocket Lab has built a diversified business model. Through its Space Systems division, the company generates revenue from satellite manufacturing, spacecraft components, solar power systems, reaction wheels, flight software, and mission operations. This diversification reduces dependence on launch revenue alone and provides more stable long-term growth.

Growing Government Business

Rocket Lab continues to strengthen relationships with NASA, the U.S. Department of Defense, and the U.S. Space Force. On July 17, the company was among several launch providers included in an expanded $17 billion National Security Space Launch Phase 3 contract ceiling, reinforcing its position as an important supplier for future government launch opportunities. While future task orders are not guaranteed, inclusion demonstrates continued confidence in Rocket Lab’s capabilities.

Expanding Commercial Space Economy

Demand for satellite deployment continues to accelerate as communications, Earth observation, defense, and scientific missions expand globally. Rocket Lab is well positioned to benefit from this long-term secular trend thanks to its vertically integrated business model.

Risks Investors Should Consider

Execution Risk

Rocket Lab’s valuation assumes continued execution across multiple high-profile projects. Delays in Neutron development, unexpected engineering challenges, or launch failures could negatively affect both financial performance and investor sentiment.

Intense Competition

Rocket Lab competes against well-funded companies including SpaceX, Blue Origin, Firefly Aerospace, Relativity Space, and several emerging international launch providers. Maintaining technological leadership while preserving margins will remain a significant challenge.

Premium Valuation

Although the recent selloff has reduced some of the market’s enthusiasm, Rocket Lab still trades at a valuation that reflects considerable future growth expectations. Investors are paying for tomorrow’s potential earnings rather than today’s profitability, making the stock particularly sensitive to execution disappointments.

Market Volatility

Rocket Lab remains a high-beta growth stock. The shares have experienced substantial price swings throughout 2026 as investors rotate between growth sectors and reassess valuations across the aerospace industry. Investors should be prepared for continued volatility despite the company’s favorable long-term outlook.

Investment Outlook

Rocket Lab remains one of the most compelling growth stories in the commercial space sector. The combination of a growing launch business, expanding Space Systems division, increasing government partnerships, and the anticipated debut of Neutron provides multiple avenues for future growth.

However, investors should recognize that Rocket Lab is still an execution-driven investment. While the long-term opportunity appears significant, meaningful risks remain, particularly surrounding product development timelines, competition, and market valuation.

For investors with a long-term investment horizon and a tolerance for volatility, Rocket Lab may represent an attractive opportunity to participate in the continued expansion of the global space economy.

Disclosure

Disclosure: I currently hold a long position in Rocket Lab Corporation (NASDAQ: RKLB). The opinions expressed in this article are solely my own and are intended for informational and educational purposes only. This article does not constitute investment advice or a recommendation to buy or sell any security. Investors should conduct their own research and consult with a licensed financial professional before making any investment decisions.

References

ChartExchange. (2026). Rocket Lab Corporation (NASDAQ: RKLB) stock statistics. https://chartexchange.com/symbol/nasdaq-rklb/

Investing.com. (2026, July 18). Rocket Lab historical price data. https://www.investing.com/equities/vector-acquisition-historical-data

Rocket Lab Corporation. (2026). About Rocket Lab. https://www.rocketlabcorp.com

U.S. Department of Defense. (2026, July 17). National Security Space Launch Phase 3 contract modifications. Referenced via community discussion.

Wikipedia contributors. (2026). Rocket Lab. https://en.wikipedia.org/wiki/Rocket_Lab