At Health to Wealth Ventures, I’ve always believed that true wealth begins with good health. That’s why I’ve made the decision to openly document my experience with Transcranial Magnetic Stimulation (TMS) as I work toward recovery from depression and reclaiming the best version of myself.

A hiker walks along a rocky mountain trail at sunrise with a stunning mountain range ahead.

This week marked the completion of another week of treatment.

The journey hasn’t been easy, but it has been worthwhile. Like many people beginning TMS, I’ve experienced moments of hope, fatigue, mental fog, and emotional ups and downs. While I’m still early in the process and not expecting overnight results, I’ve already noticed small signs that encourage me to keep moving forward.

One lesson this experience has reinforced is that recovery is rarely linear. Healing takes patience, consistency, and the willingness to trust the process even on the difficult days.

Outside of treatment, I’ve remained committed to healthy habits that support both my physical and mental well-being. Daily walks, exercise, preparing healthy meals, maintaining routines, and leaning on family and friends have all become important pieces of my recovery. TMS is one tool, but lasting wellness comes from caring for the whole person.

By sharing this journey, my hope is that others battling depression realize they are not alone. Mental health deserves the same attention and compassion as physical health, and seeking treatment is a sign of strength not weakness.

A glowing, ethereal river winds through lush green hills under a twilight sky.

As Dwayne “The Rock” Johnson once said, “Depression never discriminates.” Those simple words remind us that mental illness can affect anyone, regardless of success, background, or circumstance.

I’m optimistic about the weeks ahead and committed to seeing this treatment through. Once I complete my full course of TMS, I’ll publish a comprehensive update sharing my experience, what I’ve learned, and whether the treatment helped me achieve the recovery I’ve been working toward.

Thank you for following along and for your continued encouragement. If sharing my story helps even one person take the first step toward getting help, then this journey will have an impact far beyond my own recovery.

Remember: Your health is your greatest investment, and investing in your mental health is one of the most valuable decisions you can make.

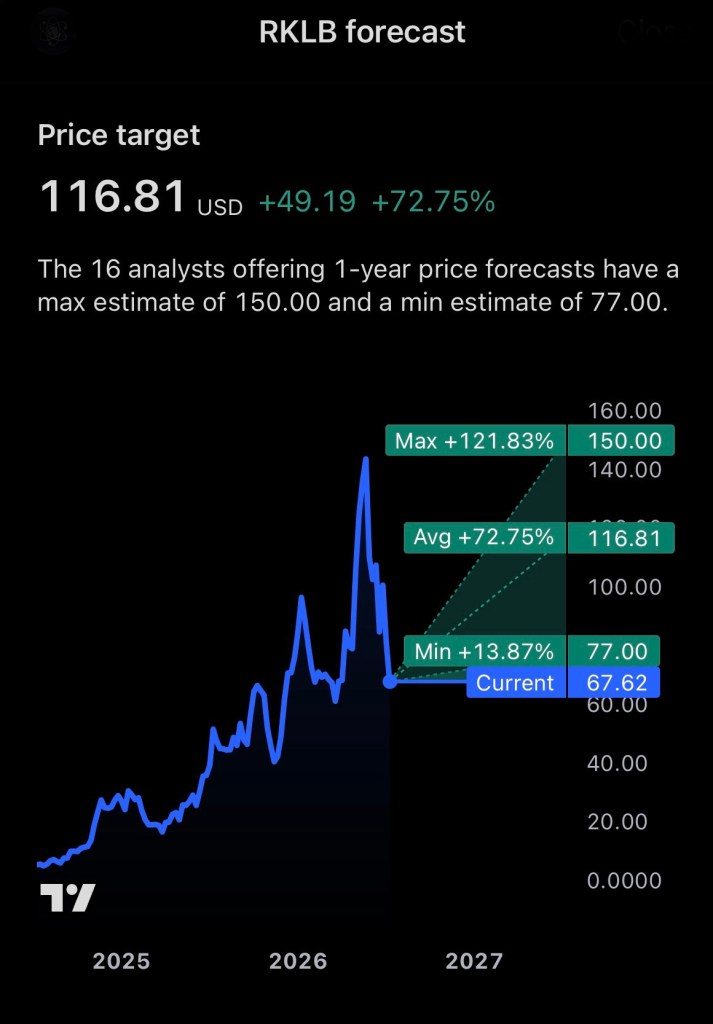

Rocket Lab Corporation (NASDAQ: RKLB) has grown from a niche small-satellite launch company into one of the world’s leading publicly traded space technology companies. Founded in 2006 by aerospace engineer Peter Beck, the company has successfully diversified beyond rocket launches by manufacturing satellites, spacecraft components, and providing end-to-end space systems for commercial, civil, and defense customers. Its Electron rocket has become one of the most frequently launched small orbital launch vehicles, while its next-generation Neutron rocket is expected to significantly expand the company’s capabilities in the medium-lift launch market.

Rocket Lab shares closed at $67.62 on Friday, July 17, 2026, recovering slightly after a volatile week that saw the stock decline more than 11% on July 16. Despite the recent correction, the company remains one of the fastest-growing names in the commercial space industry, with investors closely watching several major catalysts that could influence its long-term trajectory.

Reasons for Long-Term Upside

Neutron Rocket Development

The single largest catalyst for Rocket Lab is the development of its reusable Neutron launch vehicle. Designed to compete for larger commercial, government, and national security missions, Neutron has the potential to dramatically increase Rocket Lab’s revenue opportunities while improving launch economics. Successful execution could transform Rocket Lab from a niche launch provider into a direct competitor within the medium-lift launch market.

Diversified Revenue Streams

Unlike many emerging space companies, Rocket Lab has built a diversified business model. Through its Space Systems division, the company generates revenue from satellite manufacturing, spacecraft components, solar power systems, reaction wheels, flight software, and mission operations. This diversification reduces dependence on launch revenue alone and provides more stable long-term growth.

Growing Government Business

Rocket Lab continues to strengthen relationships with NASA, the U.S. Department of Defense, and the U.S. Space Force. On July 17, the company was among several launch providers included in an expanded $17 billion National Security Space Launch Phase 3 contract ceiling, reinforcing its position as an important supplier for future government launch opportunities. While future task orders are not guaranteed, inclusion demonstrates continued confidence in Rocket Lab’s capabilities.

Expanding Commercial Space Economy

Demand for satellite deployment continues to accelerate as communications, Earth observation, defense, and scientific missions expand globally. Rocket Lab is well positioned to benefit from this long-term secular trend thanks to its vertically integrated business model.

Risks Investors Should Consider

A satellite releases numerous small CubeSats into Earth’s orbit against a starry backdrop.

Execution Risk

Rocket Lab’s valuation assumes continued execution across multiple high-profile projects. Delays in Neutron development, unexpected engineering challenges, or launch failures could negatively affect both financial performance and investor sentiment.

Intense Competition

Rocket Lab competes against well-funded companies including SpaceX, Blue Origin, Firefly Aerospace, Relativity Space, and several emerging international launch providers. Maintaining technological leadership while preserving margins will remain a significant challenge.

Premium Valuation

Although the recent selloff has reduced some of the market’s enthusiasm, Rocket Lab still trades at a valuation that reflects considerable future growth expectations. Investors are paying for tomorrow’s potential earnings rather than today’s profitability, making the stock particularly sensitive to execution disappointments.

Market Volatility

Rocket Lab remains a high-beta growth stock. The shares have experienced substantial price swings throughout 2026 as investors rotate between growth sectors and reassess valuations across the aerospace industry. Investors should be prepared for continued volatility despite the company’s favorable long-term outlook.

Investment Outlook

Rocket Lab remains one of the most compelling growth stories in the commercial space sector. The combination of a growing launch business, expanding Space Systems division, increasing government partnerships, and the anticipated debut of Neutron provides multiple avenues for future growth.

However, investors should recognize that Rocket Lab is still an execution-driven investment. While the long-term opportunity appears significant, meaningful risks remain, particularly surrounding product development timelines, competition, and market valuation.

For investors with a long-term investment horizon and a tolerance for volatility, Rocket Lab may represent an attractive opportunity to participate in the continued expansion of the global space economy.

Disclosure

Disclosure: I currently hold a long position in Rocket Lab Corporation (NASDAQ: RKLB). The opinions expressed in this article are solely my own and are intended for informational and educational purposes only. This article does not constitute investment advice or a recommendation to buy or sell any security. Investors should conduct their own research and consult with a licensed financial professional before making any investment decisions.

Mental health is often a topic that families struggle to talk about. We may know about physical illnesses that run in our families heart disease, diabetes, cancer but we don’t always discuss depression, anxiety, trauma, or other mental health challenges with the same openness.

Recently, I found myself reflecting on my father’s story and how family experiences can shape the way we understand mental health.

A large tree with roots naturally forming a heart shape in a sunlit forest

My father suffered a heart attack at a relatively young age. He was a heavy smoker, and his heart health was something that impacted our family. After that heart attack, he told me he had taken lithium, explaining that it was for his heart. Looking back, I now understand that lithium is not typically used as a heart medication. It is most commonly associated with mood stabilization, particularly for conditions such as bipolar disorder and certain forms of treatment-resistant depression.

The truth is, I may never know exactly why he took it. Medical records are not always available, and sometimes family members remember medications or diagnoses differently than they were documented. But the conversation made me think about something deeper: the connection between trauma, mental health, and family history.

My father experienced a devastating loss when his brother was shot and killed by his wife. They were extremely close, and a tragedy like that can leave a lasting emotional impact. Severe trauma and grief can contribute to depression, anxiety, PTSD, and other mental health struggles. While we cannot assume exactly what my father experienced or what treatment he needed, it reminds me that emotional wounds can be just as real as physical ones.

That realization has also caused me to reflect on my own mental health journey.

I have been working through depression and other challenges, and I am now beginning a new chapter by starting Transcranial Magnetic Stimulation (TMS) therapy. TMS is a noninvasive treatment that uses magnetic pulses to stimulate specific areas of the brain involved in mood regulation. For many people who have not found enough relief through medication alone, TMS can provide another option.

Starting TMS is not about giving up on previous treatments it is about continuing to search for what works. Mental health treatment is often a process of finding the right combination of therapies, medications, lifestyle changes, support systems, and self-awareness.

A glowing brain surrounded by radiant light beams breaking through darkness

As I begin this journey, I want to share a few lessons I have learned:

1. Family history matters. Understanding the experiences, struggles, and challenges within our families can provide important context for our own health journeys.

2. Trauma can affect generations. Painful events do not always end when the event is over. Grief, loss, and trauma can influence how people cope, communicate, and seek help.

3. Mental health deserves the same attention as physical health. We would never tell someone with heart disease to simply “push through it.” Depression and other mental health conditions deserve compassion, treatment, and support.

4. Healing is not always a straight line. Sometimes progress comes from trying something new, adjusting course, and being willing to ask for help.

At Health to Wealth Ventures, the goal has always been to look at the complete picture of health, mind, body, finances, safety, and quality of life. True wealth is not just measured by what we own; it is also measured by our ability to enjoy life, maintain relationships, and take care of ourselves.

My TMS journey is just beginning. I don’t know exactly what the outcome will be, but I do know this: seeking help is a sign of strength, not weakness.

By sharing our stories, we can help remove the stigma around mental health and remind others that they are not alone in their journey toward healing.

Health is the foundation. Wealth is the opportunity. Together, they create a life worth living.

Auto insurance policies are not always kept for their full term. Whether a policyholder sells a vehicle, finds a better rate, moves to another state, or simply decides to switch carriers, insurance policies are often canceled before their expiration date.

What many consumers don’t realize is that not all cancellations are calculated the same way. Depending on who initiates the cancellation and when it occurs, the refund amount may vary significantly.

The three most common types of auto insurance cancellations are Pro-Rata, Short-Rate, and Flat Cancellations.

A car insurance policy, calculator, cash, and keys on a wooden desk

What Is a Pro-Rata Cancellation?

A pro-rata cancellation occurs when the insurance company cancels the policy or when a cancellation is processed without any penalty.

Under a pro-rata cancellation, the policyholder receives a refund for all unused premium on a straight-line basis.

Example

Assume:

Annual premium: $1,200

Policy term: 12 months

Policy canceled after 3 months

The policyholder used 25% of the coverage period and is entitled to a refund of the remaining 75%.

Premium paid: $1,200

Earned premium: $300

Refund: $900

No cancellation fee is deducted.

Common Reasons for Pro-Rata Cancellations

Insurance company non-renews or cancels coverage

Vehicle is totaled and coverage ends

State regulatory requirements mandate a full refund calculation

Certain carrier-specific cancellation provisions

What Is a Short-Rate Cancellation?

A short-rate cancellation is the most common form of cancellation when the policyholder voluntarily cancels coverage before the policy expires.

With a short-rate cancellation, the insurer retains slightly more premium than the exact amount earned. This creates a financial penalty intended to offset administrative costs associated with issuing and canceling the policy.

Example

Assume:

Annual premium: $1,200

Policy canceled after 3 months

Unearned premium: $900

Instead of receiving the full $900 refund, the carrier applies a short-rate penalty.

Potential refund:

Unearned premium: $900

Short-rate penalty: $45

Refund issued: $855

The exact penalty varies by carrier and state regulations.

Typical Short-Rate Fees

Many carriers use:

5% of the unearned premium

10% of the unearned premium

A fixed cancellation fee ranging from $25 to $75

A state-approved short-rate table

Why Insurers Use Short-Rate Cancellations

Insurance companies incur expenses when policies are issued, including:

Underwriting costs

Policy processing

Commission payments

Administrative expenses

Short-rate penalties help recover a portion of those costs when a customer leaves before the policy term ends.

What Is a Flat Cancellation?

A flat cancellation treats the policy as though it never existed.

The insurer returns 100% of the premium paid and no coverage is considered to have been in force.

Example

Assume:

Annual premium: $1,200

Policy purchased today

Customer discovers duplicate coverage and cancels before the policy effective date

Refund:

Premium paid: $1,200

Refund issued: $1,200

No premium is earned by the insurer.

Common Reasons for Flat Cancellations

Policy canceled before the effective date

Coverage obtained in error

Duplicate policies discovered

Underwriting declines coverage before policy inception

No claims or coverage exposure occurred

Comparing the Three Types of Cancellations

Cancellation Type

Refund Method

Penalty Applied?

Typical Situation

Flat Cancellation

100% refund

No

Policy never takes effect

Pro-Rata

Refund of unused premium

No

Insurer initiates cancellation

Short-Rate

Refund of unused premium minus fee

Yes

Customer voluntarily cancels

How Much Could Cancellation Fees Cost?

Consider a policy with a remaining unearned premium of $600:

Method

Refund

Flat Cancellation

$600

Pro-Rata Cancellation

$600

Short-Rate (5% Penalty)

$570

Short-Rate (10% Penalty)

$540

Short-Rate + $50 Fee

$550

While the difference may seem small, policyholders with higher premiums can lose hundreds of dollars when a short-rate penalty applies.

What Consumers Should Do Before Canceling

Before switching auto insurance companies:

Verify the effective date of your new policy.

Ask your current carrier whether a short-rate penalty applies.

Request the exact refund amount in writing.

Confirm there are no cancellation fees.

Avoid any lapse in coverage that could increase future insurance premiums.

Many consumers focus solely on the new premium savings and overlook cancellation penalties that can reduce the benefit of switching carriers.

A silver car under a transparent garage model on an October 2023 calendar.

The Takeaway Here

Understanding the difference between flat, pro-rata, and short-rate cancellations can help consumers make more informed decisions when changing auto insurance coverage. While flat and pro-rata cancellations generally provide the greatest refund, short-rate cancellations may reduce the amount returned through penalties or administrative fees.

Before canceling any auto policy, ask your insurance company or agent how the refund will be calculated. A simple phone call could prevent an unexpected deduction and help ensure a smooth transition to your new coverage.

Disclosure: This article is intended for educational purposes only. Cancellation rules, refund calculations, and fees vary by insurance carrier and state regulations. Consumers should consult their insurance policy and carrier for specific cancellation provisions.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Rising Costs Are Changing the Homeowners Insurance Conversation

Homeowners are facing some of the highest insurance premiums in decades for homeowner’s insurance. Inflation, severe weather events, increased construction costs, and rising litigation expenses have forced many insurers to reevaluate their risk exposure. In states such as Florida, Texas, California, and Louisiana, homeowners have experienced significant premium increases and, in some cases, reduced carrier availability.

As insurance costs continue to rise, many homeowners are asking the same question: “Am I carrying the right coverage, or am I paying for protection I may never use?”

The answer depends on your individual situation, but understanding the major components of a homeowners policy can help you make informed decisions.

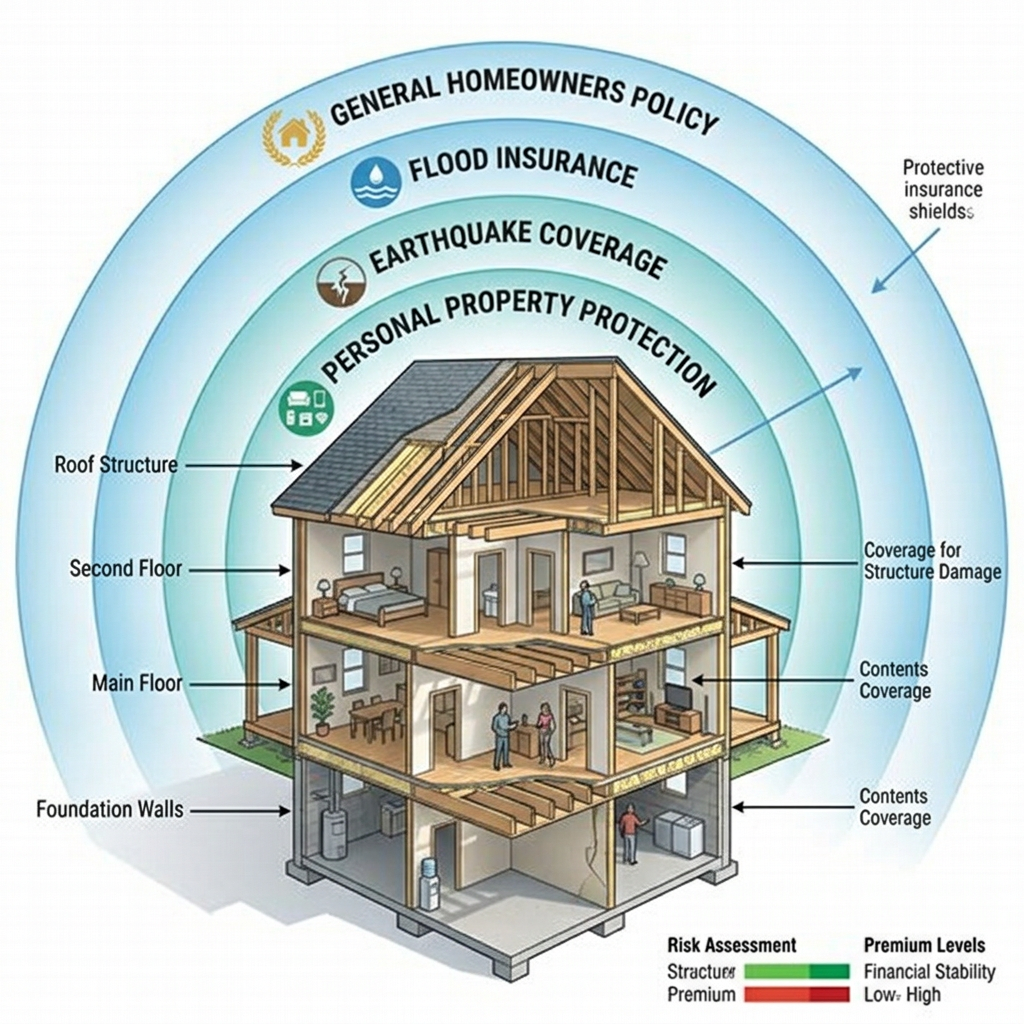

A cross-section of a home illustrating various insurance coverage layers and protections.

Coverages Most Homeowners Should Consider Keeping

Dwelling Coverage

Dwelling coverage protects the structure of your home from covered losses such as fire, wind, hail, and other insured perils.

One of the biggest mistakes homeowners make is underinsuring their property. Construction costs have risen dramatically over the last several years, making it more expensive to rebuild a home after a total loss.

Consider: Reviewing your dwelling limit annually to ensure it reflects current rebuilding costs—not necessarily the market value of your home.

Personal Property Coverage

Furniture, electronics, clothing, appliances, and personal belongings can add up quickly. Many homeowners underestimate the value of their possessions until they experience a major loss.

Consider: Creating a home inventory and verifying that your coverage limits are sufficient.

Liability Coverage

Liability coverage protects you if someone is injured on your property or if you accidentally cause damage to another person’s property.

Medical expenses and lawsuits can quickly become expensive.

Consider: Increasing liability limits to $300,000 or $500,000 if your insurer offers affordable options.

Loss of Use Coverage

If your home becomes uninhabitable due to a covered loss, loss-of-use coverage helps pay for temporary housing and living expenses.

This coverage can be invaluable following major storms, fires, or water damage claims.

Coverages Worth Reviewing

High Deductibles vs. Low Deductibles

Many homeowners carry deductibles established years ago when premiums were much lower.

Increasing your deductible from $500 to $2,500 or even $5,000 could significantly reduce annual premiums.

Trade-Off: You’ll pay more out-of-pocket if a claim occurs.

Personal Property Limits

Some homeowners may be carrying higher limits than necessary if they have downsized or replaced expensive items.

Consider: Reviewing current belongings and adjusting coverage accordingly.

Scheduled Personal Property

Items such as jewelry, collectibles, artwork, firearms, and high-end electronics often require additional endorsements.

If you no longer own these items, removing unnecessary endorsements may reduce premium costs.

Additional Structures Coverage

Coverage for detached garages, sheds, fences, and other structures may be higher than needed if structures have been removed or reduced in value.

A periodic policy review can identify potential savings.

Important Coverages Many Homeowners Overlook

Water Backup Coverage

Standard homeowners policies typically do not cover sewer or drain backup losses.

A relatively inexpensive endorsement can help protect against costly water damage.

Flood Insurance

Many homeowners incorrectly assume flood damage is covered under a standard homeowners policy.

In reality, flood losses are generally excluded.

Even homes outside designated flood zones can experience flooding due to heavy rainfall, hurricanes, or drainage issues.

Ordinance or Law Coverage

Building codes change over time. If your home suffers significant damage, you may be required to rebuild portions of it to current code standards.

Ordinance or law coverage helps pay these additional expenses.

Equipment Breakdown Coverage

Many insurers now offer protection for HVAC systems, electrical panels, water heaters, and other major home systems.

This coverage can provide value for homeowners concerned about unexpected repair costs.

When Filing Small Claims May Cost More Than It Saves

A common misconception is that insurance should be used for every loss.

In reality, frequent claims can impact eligibility, renewal options, and future premiums.

For example, filing multiple water damage claims within a few years could make it more difficult to obtain favorable rates in the future.

Homeowners should evaluate whether a smaller loss justifies filing a claim or whether paying out-of-pocket may be the better financial decision.

A scale balancing a miniature house and stacks of coins representing home value.

Final Thoughts

Homeowners insurance should not be viewed as a “set it and forget it” product. As property values, rebuilding costs, and personal circumstances change, coverage needs evolve as well.

A yearly policy review can help identify gaps in protection, uncover potential savings opportunities, and ensure your home remains adequately insured against today’s risks.

The goal is not necessarily to buy the cheapest policy available. Instead, homeowners should focus on balancing affordability with meaningful protection because saving a few dollars today could become extremely costly after a major loss.

Disclosure: This article is for informational purposes only and should not be considered insurance, legal, or financial advice. Coverage availability, exclusions, and policy terms vary by insurer and state. Consult a licensed insurance professional regarding your specific situation.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

The artificial intelligence revolution has created a new generation of technology winners, and few companies have captured investor attention as quickly as CoreWeave (NASDAQ: CRWV). Since its public debut in 2025, CoreWeave has transformed from a niche cloud computing provider into one of the most closely watched AI infrastructure companies in the market.

As demand for artificial intelligence computing continues to accelerate, investors are asking a simple question: Does CoreWeave still have room to run?

Two technicians walk through a massive AI data center filled with illuminated server racks.

A Brief History of CoreWeave

CoreWeave was founded in 2017 and originally focused on cryptocurrency mining infrastructure. As demand for high-performance computing evolved, management pivoted toward providing specialized cloud infrastructure powered by NVIDIA graphics processing units (GPUs). That decision would prove transformational.

The company went public on the Nasdaq under the ticker CRWV in March 2025, pricing its initial public offering at $40 per share and raising approximately $1.5 billion to expand its AI cloud platform.

Since then, CoreWeave has become one of the leading providers of AI-focused cloud infrastructure, serving customers that require enormous amounts of computing power for training and operating large language models and other AI applications.

What’s Driving the Stock?

Several developments have fueled investor enthusiasm during 2026.

Most notably, CoreWeave became the first cloud provider to deploy NVIDIA’s new Vera Rubin NVL72 AI systems, reinforcing its position at the forefront of next-generation AI infrastructure. The announcement helped drive a significant rally in the stock and further strengthened the company’s strategic relationship with NVIDIA.

Earlier this year, NVIDIA expanded its partnership with CoreWeave and invested an additional $2 billion in the company. The two firms announced plans to accelerate the development of large-scale AI infrastructure and AI factories over the coming decade.

The company has also reported remarkable growth in customer demand. CoreWeave disclosed a revenue backlog of approximately $99.4 billion as of March 31, 2026, providing significant visibility into future revenue streams. Major customers include some of the largest names in artificial intelligence and cloud computing.

The Bull Case: Why Investors Remain Excited

Several factors support the bullish argument for CoreWeave.

Explosive AI Demand

Artificial intelligence remains one of the fastest-growing sectors in technology. Companies are racing to build increasingly sophisticated AI models, and all of them require massive amounts of computing power. CoreWeave’s infrastructure is specifically designed to meet that demand.

Strategic NVIDIA Relationship

Few companies have a closer relationship with NVIDIA than CoreWeave. Access to next-generation hardware before competitors could provide a significant advantage as AI workloads continue to grow.

Massive Revenue Backlog

A backlog approaching $100 billion gives investors confidence that demand remains strong despite concerns about the broader economy. Few newly public companies can point to this level of contracted business.

Industry Leadership

CoreWeave has established itself as one of the premier “AI-native” cloud providers. As enterprises increasingly adopt AI, the company may be positioned to capture a growing share of infrastructure spending.

The Bear Case: Risks Investors Should Consider

Despite its impressive growth, CoreWeave is not without risks.

Capital Intensive Business Model

Building AI infrastructure is extraordinarily expensive. CoreWeave continues to spend billions on data centers, GPUs, and power capacity. Management recently increased its capital expenditure outlook as demand for AI hardware continues to surge.

Profitability Remains a Challenge

Although revenue growth has been exceptional, the company continues to report significant net losses. Investors are betting that future scale will eventually generate substantial profits. If growth slows before profitability improves, valuation concerns could emerge.

Customer Concentration

A meaningful portion of CoreWeave’s business comes from large AI companies and hyperscale cloud providers. Any reduction in spending from major customers could affect future growth rates.

Valuation Risk

Many AI-related companies trade at premium valuations based on expectations of future growth. If the AI spending cycle cools or investors become more cautious, high-growth stocks like CoreWeave could experience significant volatility.

Is There Still Upside Ahead?

The answer largely depends on whether investors believe AI infrastructure demand will continue expanding over the next decade.

Supporters argue that artificial intelligence is still in its early innings and that the demand for compute power will continue to grow exponentially. If that thesis proves correct, CoreWeave could remain one of the primary beneficiaries of the AI buildout. Recent analyst targets and market commentary suggest many on Wall Street still see meaningful upside potential from current levels.

However, investors should recognize that CoreWeave remains a high-growth, high-risk company. The business must continue executing flawlessly while managing enormous capital expenditures and eventually demonstrating sustained profitability.

Bottom Line

CoreWeave has rapidly emerged as one of the most important infrastructure providers powering the AI revolution. The company’s strategic relationship with NVIDIA, enormous revenue backlog, and leadership position in AI cloud computing have helped fuel investor enthusiasm.

While the stock may continue to benefit from the expanding AI ecosystem, investors should remember that rapid growth often comes with substantial volatility. CoreWeave represents both the promise and the risks of investing in one of the market’s most exciting sectors.

For investors willing to tolerate uncertainty, CRWV remains one of the purest publicly traded plays on the future of artificial intelligence infrastructure.

Disclosure

The author owns shares of CoreWeave (NASDAQ: CRWV). This article is for informational and educational purposes only and should not be considered investment advice. Investors should conduct their own research and consult a qualified financial advisor before making investment decisions.

References

CoreWeave. (2025, March 27). CoreWeave announces pricing of initial public offering. Retrieved from CoreWeave Investor Relations

CoreWeave. (2026, May 7). CoreWeave reports strong first quarter 2026 results. Retrieved from CoreWeave Investor Relations

Understanding the Coverages That Protect More Than Just Your Car

When shopping for auto insurance, many drivers focus on finding the lowest premium possible. While saving money is important, reducing coverage can sometimes create much larger financial risks down the road. Three coverages that often generate questions are Uninsured Motorist Coverage, Comprehensive Coverage, and Collision Coverage.

These coverages can add cost to a policy, but they may also provide critical protection when life throws an unexpected curveball.

A car is shielded by a glowing electric barrier during a storm.

Uninsured Motorist Coverage: Protection From Other Drivers’ Mistakes

Despite laws requiring auto insurance in most states, millions of drivers continue to operate vehicles without coverage or with limits too low to fully pay for damages they cause.

Uninsured Motorist (UM) Coverage helps protect you if you’re injured by a driver who has no insurance. In many states, Underinsured Motorist Coverage (UIM) may also help when the at-fault driver’s policy limits are insufficient to cover your losses.

Example

Imagine you’re stopped at a red light and another driver rear-ends your vehicle. You suffer injuries requiring physical therapy and miss several weeks of work. Later, you discover the other driver has no insurance.

Without Uninsured Motorist Coverage:

You may have to rely on your health insurance.

Lost wages may not be fully covered.

Recovering damages could require legal action against someone who may have limited assets.

With Uninsured Motorist Coverage:

Your own policy may help pay medical expenses, lost wages, and other covered damages.

Reasons You Might Consider Leaving It Off

You have substantial personal assets and alternative protection strategies.

You live in an area with relatively low uninsured driver rates.

Budget constraints make affordability the top priority.

However, many insurance professionals consider UM coverage one of the most valuable protections available because it safeguards you from risks you cannot control.

Comprehensive Coverage: Protection Against Life’s Surprises

Comprehensive Coverage protects against losses that are generally not caused by a collision.

Common examples include:

Theft

Vandalism

Falling objects

Fire

Flooding

Hail damage

Animal strikes

Example

You walk outside one morning and discover a large tree branch has fallen on your parked vehicle during a storm.

Without Comprehensive Coverage:

You pay the repair bill entirely out of pocket.

With Comprehensive Coverage:

Your insurance company may cover repairs after your deductible is applied.

Another Example

A vehicle owner in Florida parks overnight and wakes up to find their car submerged after a major storm causes flash flooding.

Comprehensive Coverage may help cover the damage, while basic liability insurance would not.

Reasons You Might Consider Leaving It Off

Your vehicle has a very low market value.

The annual premium approaches the value of the vehicle itself.

You could comfortably replace the vehicle from savings if it were totaled.

For many drivers, comprehensive coverage provides peace of mind against unpredictable events that occur when the vehicle isn’t even being driven.

Collision Coverage: Protection for Your Vehicle

Collision Coverage helps pay for damage to your vehicle when it collides with another vehicle or object, regardless of fault.

Example

You’re backing out of a parking space and accidentally strike a concrete pole.

Without Collision Coverage:

You are responsible for all repair costs.

With Collision Coverage:

Your policy may pay for repairs after your deductible.

Another Example

A driver loses control during heavy rain and slides into a guardrail. The vehicle sustains $12,000 in damage.

With Collision Coverage:

The policy may cover repairs, less the deductible.

Without Collision Coverage:

The owner must absorb the entire loss.

When It May Make Sense to Drop Collision Coverage

There are situations where removing collision coverage can be financially reasonable.

Consider:

The vehicle’s value has significantly declined.

You have sufficient savings to replace the vehicle.

The premium and deductible together provide little financial benefit compared to the vehicle’s actual cash value.

For example, carrying collision coverage on a vehicle worth only $2,500 may not always make economic sense if the annual premium is high.

A Simple Rule of Thumb

Many insurance professionals suggest periodically reviewing your vehicle’s value. As vehicles age, the cost-benefit analysis of comprehensive and collision coverage changes.

Ask yourself:

What is my vehicle worth today?

Could I afford to replace it tomorrow?

How much would a major repair affect my finances?

Am I comfortable assuming more risk in exchange for lower premiums?

A blue car parked with digital icons showing theft, fire, flood, and collision coverage

Final Perspective

Auto insurance isn’t just about satisfying state requirements, it’s about protecting your financial future. Uninsured Motorist, Comprehensive, and Collision Coverage each address different risks that can lead to significant out-of-pocket expenses.

While there are legitimate reasons to decline these coverages, drivers should carefully evaluate the potential savings against the financial consequences of a major accident, theft, storm, or uninsured driver. The cheapest policy is not always the least expensive option when an unexpected loss occurs.

As with any insurance decision, reviewing your coverage annually and discussing your needs with a licensed insurance professional can help ensure your protection keeps pace with your changing circumstances.

Disclaimer: This article is for educational purposes only and is not insurance, legal, or financial advice. Coverage availability, policy terms, exclusions, and requirements vary by state and insurance carrier. Consult a licensed insurance professional regarding your specific situation.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Across the country, homeowners are facing rising insurance premiums as insurance companies respond to increasing claims, inflation, severe weather events, and aging housing stock. While many homeowners focus on shopping for lower rates, one of the most overlooked factors affecting premiums is the condition of the home itself.

Insurance companies are paying closer attention than ever to property maintenance. Advances in aerial imagery, satellite technology, drones, and property inspection software allow insurers to identify potential hazards without ever stepping inside a home.

The result? A roof nearing the end of its life, deteriorating plumbing, outdated electrical systems, or neglected exterior maintenance can lead to premium increases, non-renewal notices, or even cancellation of coverage.

Neatly arranged hand tools contrast with nearby construction rubble and damaged wall.

Why Maintenance Matters

Insurance is based on risk. The greater the likelihood that a claim will occur, the higher the premium charged to insure that risk.

For example:

An aging roof is more likely to leak or sustain storm damage.

Old plumbing systems increase the risk of water damage claims.

Outdated electrical systems increase fire risk.

Dead trees and damaged siding create additional exposure during severe weather events.

From an insurer’s perspective, a well-maintained home represents a lower probability of costly claims.

The Hidden Cost of Deferred Maintenance

Many homeowners postpone repairs to save money. Unfortunately, the long-term costs can be much greater.

Consider a roof that should have been replaced five years ago. Not only may the homeowner face higher premiums, but a future claim could be limited or denied if the damage is determined to result from wear and tear rather than a sudden covered event.

Similarly, a small plumbing leak left unaddressed can eventually lead to thousands of dollars in water damage and mold remediation expenses.

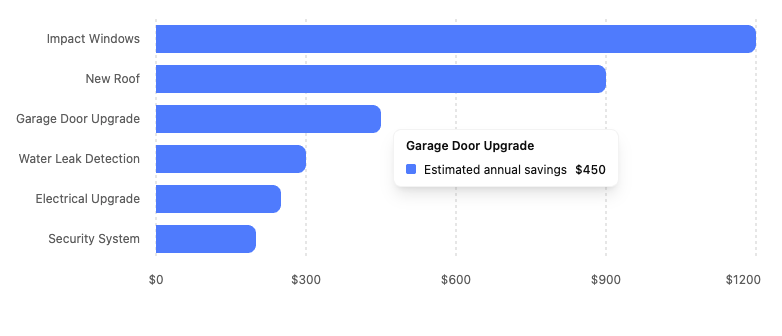

Estimated Repair Costs and Potential Insurance Benefits

The following estimates represent typical costs in today’s market. Actual costs vary based on location, home size, and materials used.

Home Improvement

Estimated Cost

Potential Insurance Impact

New Roof

$12,000 – $30,000

Lower premiums and improved eligibility for coverage

Electrical Panel Upgrade

$2,000 – $6,000

Reduced fire risk may qualify for credits

Whole Home Re-Plumbing

$4,000 – $15,000

Reduced water damage exposure

Hurricane Impact Windows

$10,000 – $30,000

Significant wind mitigation discounts in many states

HVAC Replacement

$5,000 – $12,000

Reduced risk of system-related losses

Water Leak Detection System

$500 – $2,500

Discounts offered by some insurers

Garage Door Wind Upgrade

$1,500 – $5,000

Windstorm mitigation credits

Exterior Painting and Siding Repair

$3,000 – $15,000

Improves insurability and property condition scores

Tree Removal Near Structure

$500 – $5,000

Reduces storm-related claim risk

Security System Installation

$300 – $2,000

Potential theft and fire protection discounts

Estimated Annual Premium Savings

While every insurer is different, homeowners may see reductions ranging from modest to substantial depending on the improvement completed.

Potential annual homeowners insurance savings

Illustrative annual savings after major home improvements. Actual savings vary by insurer, location, and home characteristics.

Florida Homeowners Face Unique Challenges

Homeowners in Florida have experienced some of the nation’s largest insurance premium increases in recent years. Windstorm exposure, hurricane losses, litigation costs, and reinsurance expenses have dramatically impacted the market.

For Florida homeowners, improvements such as:

New roofs

Impact-resistant windows

Reinforced garage doors

Updated roof-to-wall connections

can often produce meaningful insurance savings through wind mitigation programs while simultaneously strengthening the home against future storms.

The Takeaway

Your home is likely your largest financial asset. Maintaining it properly not only protects its value but can also help keep insurance costs under control.

Before renewing your homeowners insurance policy, consider reviewing the age and condition of major systems throughout your home. A repair that seems expensive today may ultimately save thousands of dollars in future claims, prevent coverage issues, and reduce annual insurance premiums for years to come.

Disclosure: This article is intended for educational purposes only and should not be considered insurance, legal, or financial advice. Insurance eligibility, discounts, and premiums vary by carrier, location, and individual underwriting guidelines.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

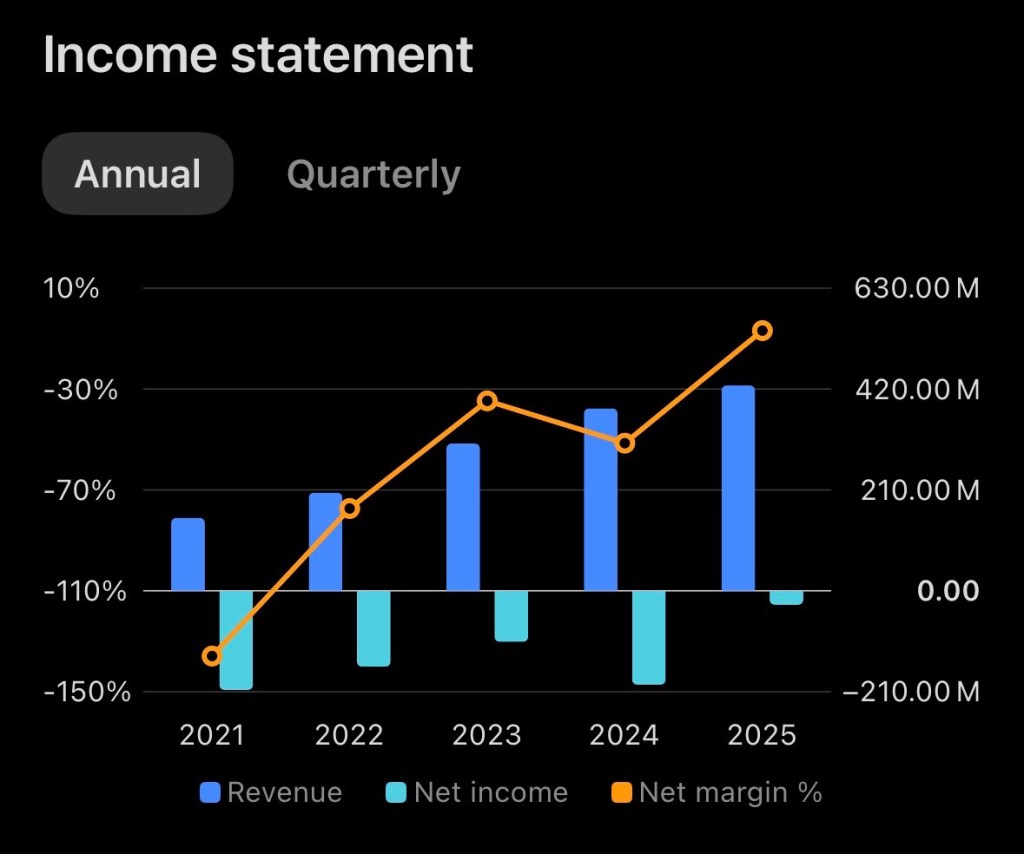

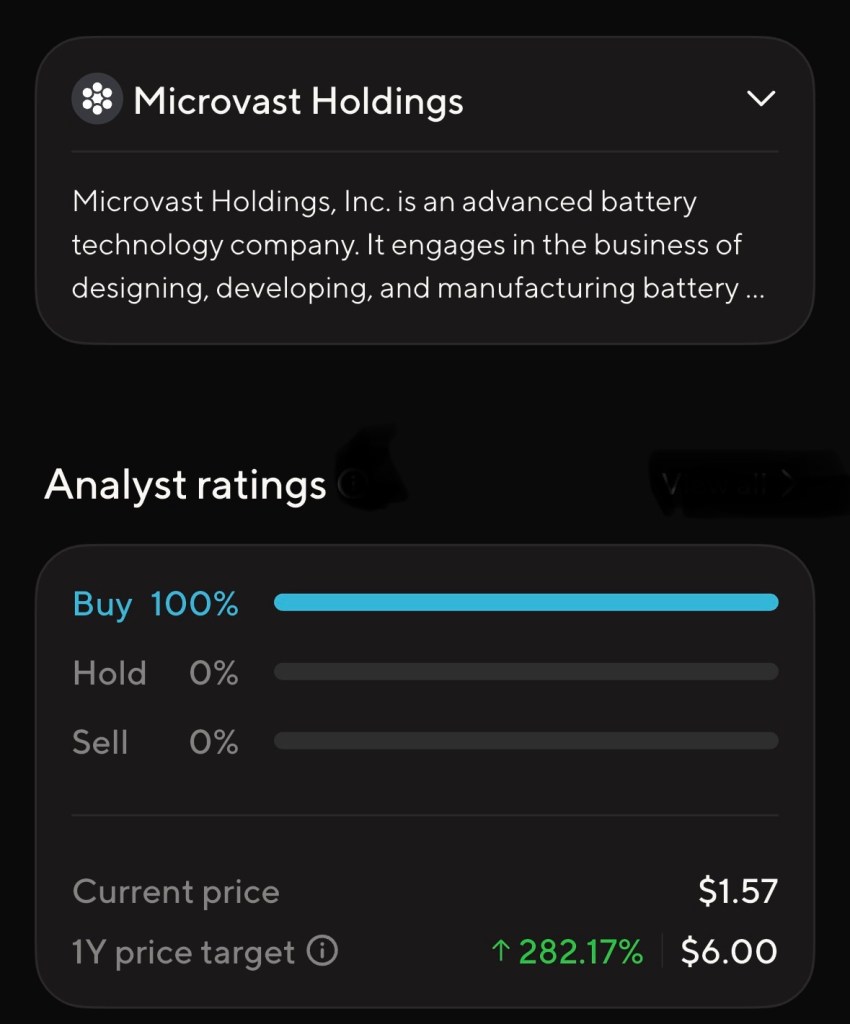

Microvast Holdings has become one of the more polarizing names in the electric vehicle and energy storage sector. Supporters view the company as an undervalued battery innovator with growing global manufacturing capacity, while critics point to volatile earnings, geopolitical concerns, and persistent financial risks.

As of late May 2026, shares of MVST have traded near the low single digits after significant volatility over the last several years. Despite the sharp decline from post-SPAC highs, many investors continue to speculate that the company could benefit from the long-term expansion of electrification, commercial EV adoption, and energy storage demand.

A large automated factory floor producing battery modules

The History of Microvast

Founded in 2006 in Houston, Texas, Microvast focuses on lithium-ion battery systems for commercial vehicles, energy storage systems, and industrial applications. The company developed operations across the United States, China, and Germany while building expertise in battery chemistry, separators, electrolytes, and fast-charging systems.

The company gained broader investor attention in 2021 when it went public through a SPAC merger during the peak of EV enthusiasm. Like many SPAC-era companies, MVST initially traded at elevated valuations as investors aggressively pursued battery and clean-energy names.

Microvast later faced controversy surrounding its China operations and the cancellation of a proposed $200 million U.S. Department of Energy grant intended to support battery manufacturing expansion. That decision intensified investor concerns about geopolitical exposure and supply-chain dependency.

Still, the company continued expanding production capacity and investing in next-generation battery technologies. Management has emphasized commercial transportation markets rather than competing directly in the intensely competitive passenger EV battery space.

Current Financial Picture

Microvast’s recent financial results present a mixed picture.

For full-year 2025, the company reported record revenue of approximately $427.5 million, representing year-over-year growth of 12.6%. Gross margins improved materially, and losses narrowed significantly compared with prior years.

However, 2026 has started on a weaker note. In first-quarter 2026 results, revenue fell 48% year over year to $60.6 million due to regulatory pressures, geopolitical uncertainty, delayed OEM platform launches, and softer demand in certain international markets.

While the company remained GAAP profitable during the quarter because of accounting-related gains, adjusted earnings deteriorated sharply. Adjusted EBITDA turned negative, and the company disclosed ongoing operational headwinds tied to tariffs, logistics costs, and reduced factory utilization.

Balance sheet concerns also remain a factor. Some analysts continue monitoring debt levels and liquidity closely as the company works toward sustainable profitability.

Why MVST Could Be a Good Investment

Exposure to Long-Term EV and Energy Storage Growth

The global battery market is expected to expand substantially over the next decade as commercial transportation fleets, grid storage systems, and industrial electrification continue growing. Microvast already operates internationally and has established manufacturing infrastructure that could benefit if demand accelerates.

Vertical Integration

Unlike some battery competitors, Microvast develops multiple components internally, including cathodes, separators, and electrolytes. Investors bullish on the company believe this could improve margins and reduce dependence on third-party suppliers over time.

Improving Historical Revenue Trend

Although 2026 began weakly, revenue growth from 2022 through 2025 was substantial. Company reports show revenue more than doubling during that period while gross profit expanded meaningfully.

Commercial Vehicle Niche

Microvast focuses heavily on buses, industrial fleets, heavy equipment, and commercial transportation. Some investors believe this niche could prove more stable than the intensely competitive passenger EV market dominated by larger battery producers.

Why MVST Could Be a Poor Investment

Financial Volatility

The largest concern surrounding MVST remains inconsistent financial performance. Revenue swings, negative adjusted earnings, and ongoing cash burn have created significant uncertainty. The recent 48% quarterly revenue decline demonstrates how vulnerable the business remains to external disruptions.

Geopolitical Risk

Microvast’s operational footprint includes China, which continues generating political and regulatory concerns among some U.S. investors and policymakers. Tariffs, export controls, and shifting trade policies could continue impacting margins and investor sentiment.

Intense Competition

The battery sector is crowded with large, well-capitalized competitors. Companies across China, South Korea, Japan, Europe, and the United States continue investing aggressively in battery manufacturing capacity and chemistry innovation.

Speculative Nature of the Stock

MVST remains a speculative small-cap growth company. Stocks in this category often experience extreme volatility, dilution risk, and rapid shifts in investor sentiment. The company’s share price history reflects that reality.

Investment Outlook

Microvast represents a classic high-risk, high-reward investment profile. Bulls see an undervalued battery technology company positioned for long-term electrification trends. Bears see a financially unstable company operating in a fiercely competitive industry with geopolitical baggage and inconsistent execution.

For investors considering MVST, the key questions may revolve around whether management can stabilize revenue growth, maintain margin improvements, and achieve sustainable profitability before capital markets become less accommodating for speculative growth companies.

Disclosure

The author owns a position in MVST. This article reflects personal opinions and is intended for informational and educational purposes only. It should not be considered financial advice or a recommendation to buy or sell securities. Investors should conduct their own due diligence and consider their risk tolerance before investing.

Over the past few years here, one thing has become clear: the topics that matter most are the ones that impact everyday people in real life. From protecting families financially to improving personal health and building long-term wealth, the conversations shared across social media have focused on practical advice, real experiences, and personal growth.

Here’s a look back at some of the biggest themes that resonated with readers and followers alike.

A scenic dirt path leads to a city skyline at sunset, with glowing navigation and connectivity icons along the trail.

Insurance Isn’t Just a Bill… It’s a Financial Safety Net

One recurring topic has been the importance of understanding insurance beyond the monthly premium. Conversations around auto insurance scores, homeowner protection, life changes, and shopping for coverage highlighted how important it is to make informed decisions.

Many drivers don’t realize that constantly switching insurance companies can sometimes hurt their long-term pricing and stability. Insurance history, payment consistency, claim frequency, and credit-related factors often play a role in how rates are calculated. The key message shared over time has been simple:

✅ Shop smart ✅ Compare coverage… not just price ✅ Understand what you’re buying ✅ Protect yourself before problems happen

There were also important discussions about protecting families after the loss of a spouse. Topics included updating estate documents, reviewing beneficiaries, adjusting homeowners and auto insurance policies, and making sure financial accounts are organized during difficult times.

Health and Sleep Matter More Than We Admit

Another major focus centered around health and quality of life, especially sleep.

Personal experiences discussing CPAP therapy opened conversations for many people struggling silently with exhaustion, poor sleep quality, and untreated sleep apnea. The message was relatable because it focused on real-life improvements instead of medical jargon.

Many readers connected with the idea that better sleep can improve:

Energy levels

Mood and mental clarity

Blood pressure

Productivity

Overall quality of life

The discussions also honestly addressed the adjustment period that comes with CPAP use, reminding people that long-term health improvements often require patience and consistency.

Mental Health Conversations Continue to Break Stigma

Mental health awareness became another important topic throughout the years. Rather than focusing only on diagnoses or labels, the message centered around perseverance, growth, and finding purpose despite difficult seasons.

The overall tone remained encouraging:

Every day is another opportunity to keep moving forward.

Readers responded positively to honest conversations about stress, emotional struggles, and the importance of seeking support while continuing to pursue productive and meaningful lives.

Investing Conversations Focused on Long-Term Thinking

Investment-related discussions also attracted strong engagement, especially around dividend-paying companies and emerging growth opportunities.

Articles and commentary involving companies like General Mills (GIS) and Ondas Holdings (ONDS) explored the balance between stability and growth potential.

Topics included:

Dividend investing

Market volatility

Long-term portfolio strategy

Risk management

Emerging technology opportunities

One consistent theme stood out:

📈 Investing is not about chasing hype every day it’s about building disciplined habits over time.

Transparency also remained important, with disclosures shared whenever positions in discussed companies were personally owned.

A vintage scale balancing symbols of health, money, technology, and family.

Technology, Sustainability, and Everyday Innovation

Discussions around sustainability and technology showed how rapidly the world is changing. Topics ranged from electric vehicles and smart homes to how innovation is reshaping the insurance industry itself.

As more households adopt connected devices and cleaner technologies, conversations emphasized how these changes may impact:

Insurance pricing

Risk assessment

Home safety

Driving habits

Long-term financial savings

The growing overlap between technology and personal finance continues to create opportunities for consumers willing to stay informed.

Why These Conversations Connected With People

The reason these topics gained attention is because they were grounded in real life.

They weren’t just about headlines or trends they focused on:

✔ Protecting families ✔ Improving health ✔ Building financial stability ✔ Encouraging personal growth ✔ Preparing for the unexpected

In a social media environment often dominated by negativity and noise, practical conversations that educate, encourage, and empower people continue to stand out.

Key Takeaway

Over the years, these discussions have shown that everyday decisions can have a lasting impact. Whether it’s reviewing an insurance policy, improving sleep, investing for the future, or simply finding ways to stay positive during difficult times, small steps often create meaningful long-term results.

The conversations will continue because life keeps evolving, and staying informed matters more than ever.