Rising Costs Are Changing the Homeowners Insurance Conversation

Homeowners are facing some of the highest insurance premiums in decades for homeowner’s insurance. Inflation, severe weather events, increased construction costs, and rising litigation expenses have forced many insurers to reevaluate their risk exposure. In states such as Florida, Texas, California, and Louisiana, homeowners have experienced significant premium increases and, in some cases, reduced carrier availability.

As insurance costs continue to rise, many homeowners are asking the same question: “Am I carrying the right coverage, or am I paying for protection I may never use?”

The answer depends on your individual situation, but understanding the major components of a homeowners policy can help you make informed decisions.

Coverages Most Homeowners Should Consider Keeping

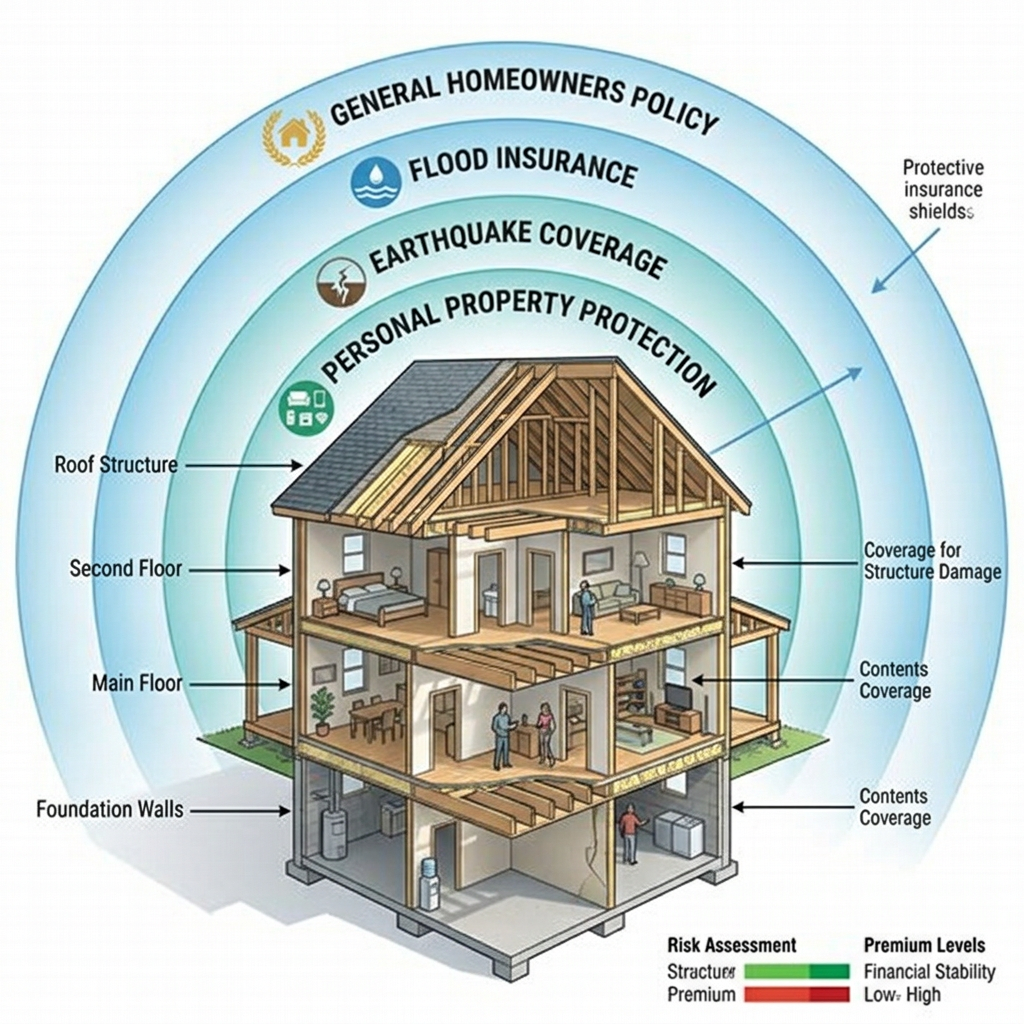

Dwelling Coverage

Dwelling coverage protects the structure of your home from covered losses such as fire, wind, hail, and other insured perils.

One of the biggest mistakes homeowners make is underinsuring their property. Construction costs have risen dramatically over the last several years, making it more expensive to rebuild a home after a total loss.

Consider: Reviewing your dwelling limit annually to ensure it reflects current rebuilding costs—not necessarily the market value of your home.

Personal Property Coverage

Furniture, electronics, clothing, appliances, and personal belongings can add up quickly. Many homeowners underestimate the value of their possessions until they experience a major loss.

Consider: Creating a home inventory and verifying that your coverage limits are sufficient.

Liability Coverage

Liability coverage protects you if someone is injured on your property or if you accidentally cause damage to another person’s property.

Medical expenses and lawsuits can quickly become expensive.

Consider: Increasing liability limits to $300,000 or $500,000 if your insurer offers affordable options.

Loss of Use Coverage

If your home becomes uninhabitable due to a covered loss, loss-of-use coverage helps pay for temporary housing and living expenses.

This coverage can be invaluable following major storms, fires, or water damage claims.

Coverages Worth Reviewing

High Deductibles vs. Low Deductibles

Many homeowners carry deductibles established years ago when premiums were much lower.

Increasing your deductible from $500 to $2,500 or even $5,000 could significantly reduce annual premiums.

Trade-Off: You’ll pay more out-of-pocket if a claim occurs.

Personal Property Limits

Some homeowners may be carrying higher limits than necessary if they have downsized or replaced expensive items.

Consider: Reviewing current belongings and adjusting coverage accordingly.

Scheduled Personal Property

Items such as jewelry, collectibles, artwork, firearms, and high-end electronics often require additional endorsements.

If you no longer own these items, removing unnecessary endorsements may reduce premium costs.

Additional Structures Coverage

Coverage for detached garages, sheds, fences, and other structures may be higher than needed if structures have been removed or reduced in value.

A periodic policy review can identify potential savings.

Important Coverages Many Homeowners Overlook

Water Backup Coverage

Standard homeowners policies typically do not cover sewer or drain backup losses.

A relatively inexpensive endorsement can help protect against costly water damage.

Flood Insurance

Many homeowners incorrectly assume flood damage is covered under a standard homeowners policy.

In reality, flood losses are generally excluded.

Even homes outside designated flood zones can experience flooding due to heavy rainfall, hurricanes, or drainage issues.

Ordinance or Law Coverage

Building codes change over time. If your home suffers significant damage, you may be required to rebuild portions of it to current code standards.

Ordinance or law coverage helps pay these additional expenses.

Equipment Breakdown Coverage

Many insurers now offer protection for HVAC systems, electrical panels, water heaters, and other major home systems.

This coverage can provide value for homeowners concerned about unexpected repair costs.

When Filing Small Claims May Cost More Than It Saves

A common misconception is that insurance should be used for every loss.

In reality, frequent claims can impact eligibility, renewal options, and future premiums.

For example, filing multiple water damage claims within a few years could make it more difficult to obtain favorable rates in the future.

Homeowners should evaluate whether a smaller loss justifies filing a claim or whether paying out-of-pocket may be the better financial decision.

Final Thoughts

Homeowners insurance should not be viewed as a “set it and forget it” product. As property values, rebuilding costs, and personal circumstances change, coverage needs evolve as well.

A yearly policy review can help identify gaps in protection, uncover potential savings opportunities, and ensure your home remains adequately insured against today’s risks.

The goal is not necessarily to buy the cheapest policy available. Instead, homeowners should focus on balancing affordability with meaningful protection because saving a few dollars today could become extremely costly after a major loss.

Disclosure: This article is for informational purposes only and should not be considered insurance, legal, or financial advice. Coverage availability, exclusions, and policy terms vary by insurer and state. Consult a licensed insurance professional regarding your specific situation.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.