GIS, one of the most recognizable consumer staples companies in the United States, has increasingly attracted income-focused investors as its stock price has declined significantly from recent highs. Known for household brands such as Cheerios, Pillsbury, Häagen-Dazs, Betty Crocker, and Blue Buffalo, General Mills now offers one of the highest dividend yields in the packaged food sector.

As of May 2026, shares of General Mills are trading near multi-year lows around the mid-$30 range after previously trading above $55 within the past year. The decline has pushed the company’s dividend yield above 7%, a level rarely seen for a mature consumer staples company with decades of dividend history.

Strong Dividend Remains a Key Attraction

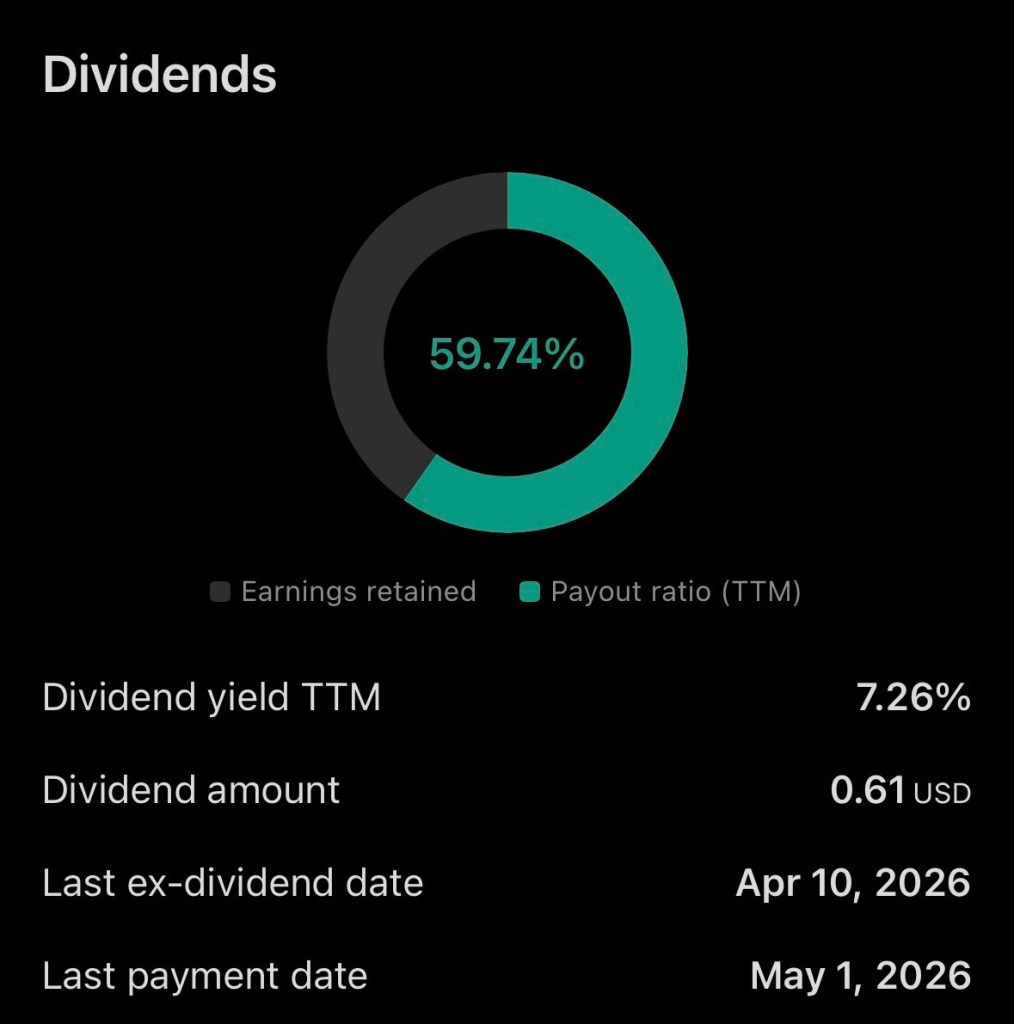

General Mills currently pays an annual dividend of approximately $2.44 per share, translating to a dividend yield above 7%. The company has maintained consistent quarterly dividend payments and has modestly increased its payout in recent years. The payout ratio remains near 60%, which many analysts still consider manageable for a stable consumer products company.

For income investors, the yield alone may make GIS an attractive defensive holding during periods of market volatility and economic uncertainty. Consumer staples companies historically perform better during slower economic periods because consumers continue purchasing essential food products regardless of broader market conditions.

Financial Performance Shows Both Strengths and Challenges

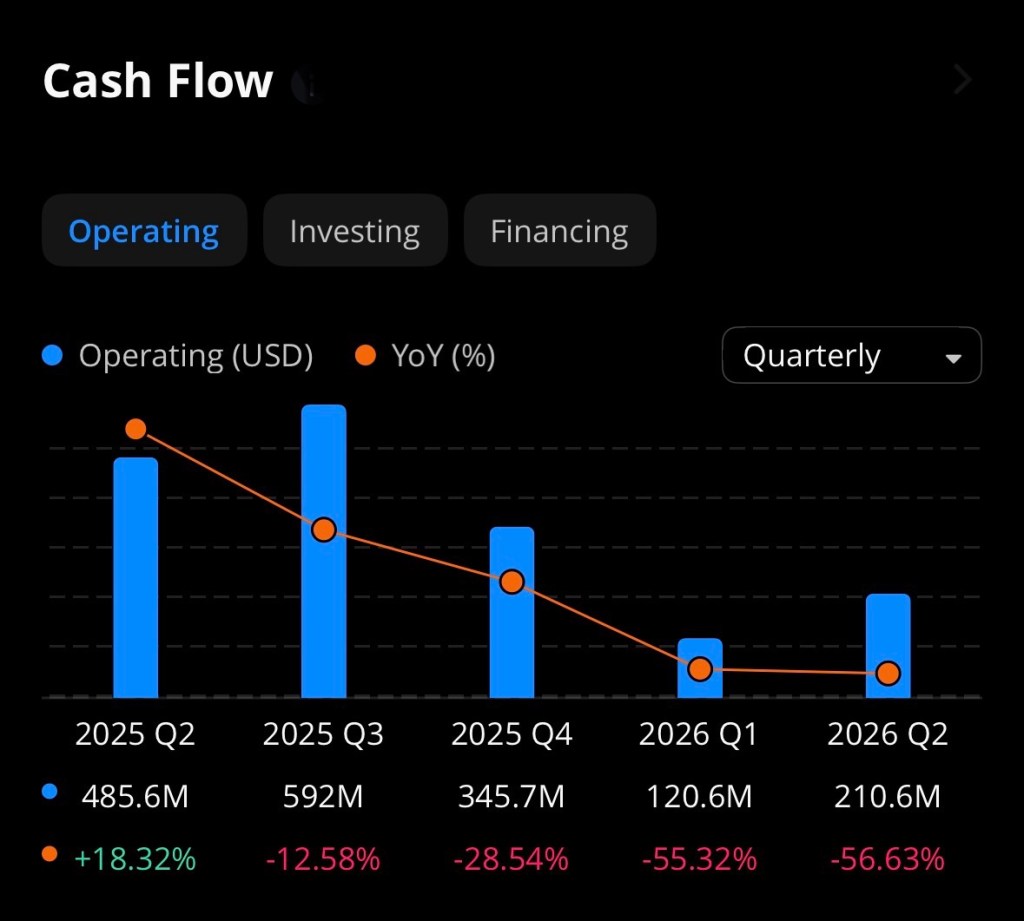

While the dividend remains attractive, General Mills has faced operational headwinds over the past year. Revenue has declined modestly, with trailing twelve-month revenue around $18.4 billion, down more than 6% year-over-year. Earnings and profit margins have also softened as consumers increasingly seek lower-cost alternatives amid inflationary pressures.

The company recently reduced portions of its fiscal 2026 guidance, citing weaker consumer demand and increasing competition from private-label food brands. Management has acknowledged that shoppers are becoming increasingly price sensitive and are prioritizing value-based purchases.

Despite these challenges, General Mills continues to generate substantial cash flow and maintains strong brand recognition across multiple product categories. The company is also investing heavily in innovation, protein-focused products, pet food expansion, and operational efficiencies aimed at improving long-term growth.

Why Some Investors See Upside Potential

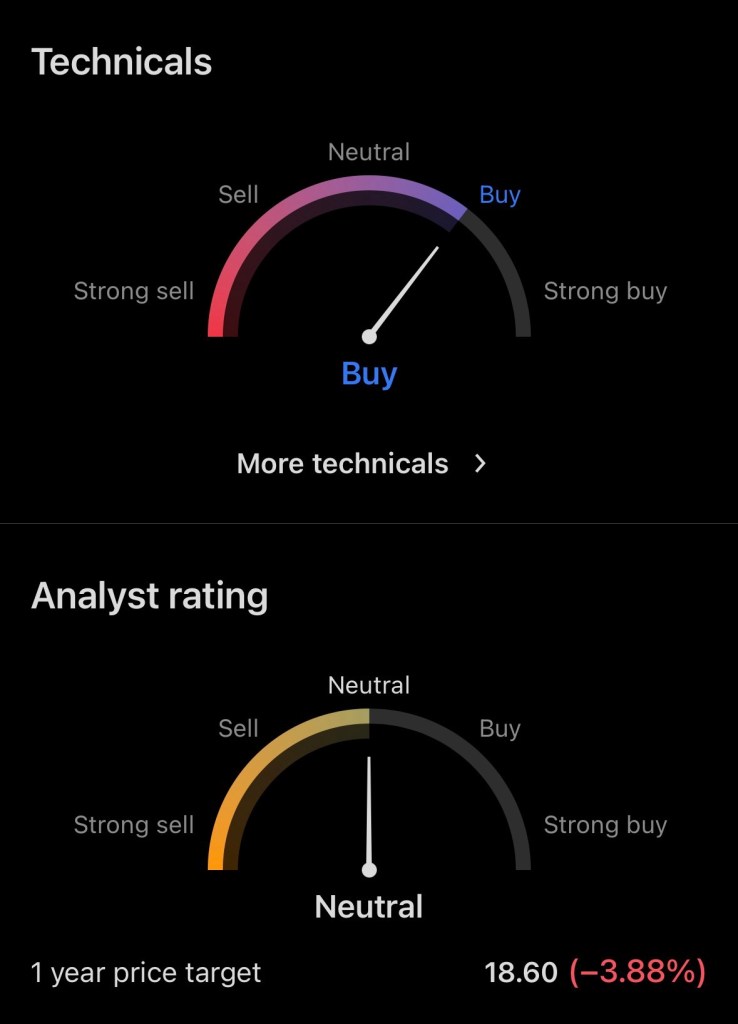

Although sentiment surrounding GIS has weakened, several valuation metrics suggest the stock could offer upside potential at current levels.

General Mills currently trades at a price-to-earnings ratio below 9, substantially lower than many competitors in the consumer staples sector. Analyst price targets average around $42 per share, implying potential upside of nearly 18% from recent trading levels.

Bullish investors argue that much of the negative outlook may already be reflected in the current stock price. If inflation moderates, consumer spending stabilizes, and management successfully executes its growth initiatives, GIS could potentially see both earnings stabilization and multiple expansion over the next 12 to 24 months.

Additionally, the combination of a high dividend yield and possible capital appreciation may appeal to long-term dividend growth investors seeking total return opportunities.

Risks Investors Should Monitor

Despite the attractive valuation and dividend yield, risks remain. Persistent inflation, changing consumer habits, private-label competition, and margin compression could continue pressuring earnings. The packaged food industry also faces ongoing challenges from shifting dietary preferences and increased competition from health-focused brands.

Investors should also monitor debt levels, input cost inflation, and whether the company can successfully restore organic sales growth over upcoming quarters.

Final Thoughts

General Mills appears to represent a classic value-versus-growth debate. The company is no longer viewed as a high-growth stock, but its depressed valuation, established global brands, and substantial dividend yield could present an opportunity for patient investors willing to accept slower growth and near-term volatility.

For dividend-focused portfolios, GIS may warrant consideration as a high-income consumer staples holding, particularly if management can stabilize sales trends and maintain strong free cash flow generation.

Disclosure

The author currently owns a position in General Mills ($GIS). This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research before making investment decisions.

References (APA Format)

MacroTrends. (2026). General Mills revenue 2012–2026. Retrieved May 21, 2026, from MacroTrends

Reuters. (2026, February 17). General Mills’ forecast cut from demand hit rattles packaged-food stocks. Retrieved May 21, 2026, from Reuters

Stock Analysis. (2026). General Mills (GIS) dividend history, dates & yield. Retrieved May 21, 2026, from Stock Analysis Dividend Page

Stock Analysis. (2026). General Mills (GIS) financials & income statement. Retrieved May 21, 2026, from Stock Analysis Financials

Stock Analysis. (2026). General Mills (GIS) stock price & overview. Retrieved May 21, 2026, from Stock Analysis Overview

MarketWatch. (2026). Cheerios parent General Mills says it will sacrifice some profit to drive sales amid cautious consumers. Retrieved May 21, 2026, from MarketWatch Article