When renewing your registration or handling certain vehicle-related matters at the Department of Motor Vehicles (DMV), you may be asked to provide an FS-1. For many drivers, the request sparks confusion—but the form is a crucial part of verifying compliance with state insurance laws.

What Is an FS-1? An FS-1, sometimes called a “Certificate of Insurance,” is an official document issued by your auto insurance company. It confirms that you currently carry liability insurance that meets or exceeds the minimum coverage required by your state. Unlike a regular insurance ID card, the FS-1 is not something you automatically receive when you buy a policy; it’s generated only when the DMV requests it.

Why the DMV Requests an FS-1 The DMV may request an FS-1 for several reasons, including:

Registration Renewals: To confirm your vehicle has active coverage before issuing new tags.

New Vehicle Registration: When adding a car to the road for the first time, proof of proper insurance is mandatory.

Insurance Verification Programs: States often run audits to catch lapsed or fraudulent insurance, and an FS-1 is one way to confirm coverage directly from your insurer.

After Accidents or Violations: If you’ve been cited for driving uninsured or been involved in a crash, the DMV may require the FS-1 to prove you now carry valid insurance.

What the FS-1 Does The FS-1 serves as an official communication between your insurance company and the DMV. Unlike simply showing your insurance card, the FS-1 provides legal assurance that your coverage is valid, active, and issued by a licensed carrier. It protects the state—and other drivers on the road—by helping ensure that every registered vehicle is financially responsible in case of an accident.

The Bottom Line If the DMV asks you for an FS-1, don’t panic. It doesn’t necessarily mean you’re in trouble—it simply means they need official verification of your insurance. Contact your insurance agent or company right away, and they can file the FS-1 directly with the DMV on your behalf.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As I’ve gotten older, I’ve realized that taking care of my mind is just as important as taking care of my body. It’s not just about preventing memory lapses; it’s about staying sharp, curious, and engaged with life. Over the years, I’ve adopted several habits that I truly believe have helped me keep my brain in good shape—and the science backs it up.

Exercise Is My Non-Negotiable I’ve found that moving my body daily, whether it’s a brisk walk, yoga, or light weightlifting, doesn’t just keep me physically fit—it clears my mind. Research shows that exercise increases blood flow to the brain and encourages the growth of new brain cells. I can feel the difference in my focus and energy on the days I move versus the days I don’t.

Food as Brain Fuel What I eat has changed a lot. I’ve cut back on processed foods and leaned more into fresh vegetables, fruits, nuts, and fish. The Mediterranean diet, which many doctors recommend, isn’t just about longevity—it’s about mental clarity. When I eat clean, my thoughts feel sharper and my mood steadier.

Protecting My Sleep In my younger years, I thought burning the candle at both ends was normal. Now, I treat sleep like medicine. Deep sleep helps my brain “clean house,” and when I get a solid 7–8 hours, my memory and problem-solving are noticeably better.

The Power of People I’ve learned that socializing isn’t just about fun—it’s brain protection. Conversations, laughter, and community keep me engaged and emotionally balanced. Isolation, on the other hand, makes my mind feel sluggish.

Challenging My Mind Daily Reading books, doing puzzles, or even trying to learn new skills keeps my brain on its toes. Recently, I started learning a new language—it’s humbling, but I can feel my brain stretching in ways it hasn’t in years.

Managing Stress the Hard Way Stress used to be my constant companion. Over time, I noticed how it clouded my judgment and wore me down mentally. Now, I practice mindfulness and deep breathing. Even a few minutes of stillness in the morning changes how my entire day feels.

Checking In on My Health Finally, I don’t ignore routine checkups anymore. Managing blood pressure, cholesterol, and overall health directly affects brain health. I’ve seen too many people neglect this, only to face cognitive issues later in life.

At the end of the day, brain health is not about one magic trick—it’s about small, consistent habits. For me, it’s a mix of movement, nourishment, rest, connection, curiosity, peace of mind, and medical awareness. And I can honestly say, these practices make me feel sharper, more alive, and ready for whatever comes next.

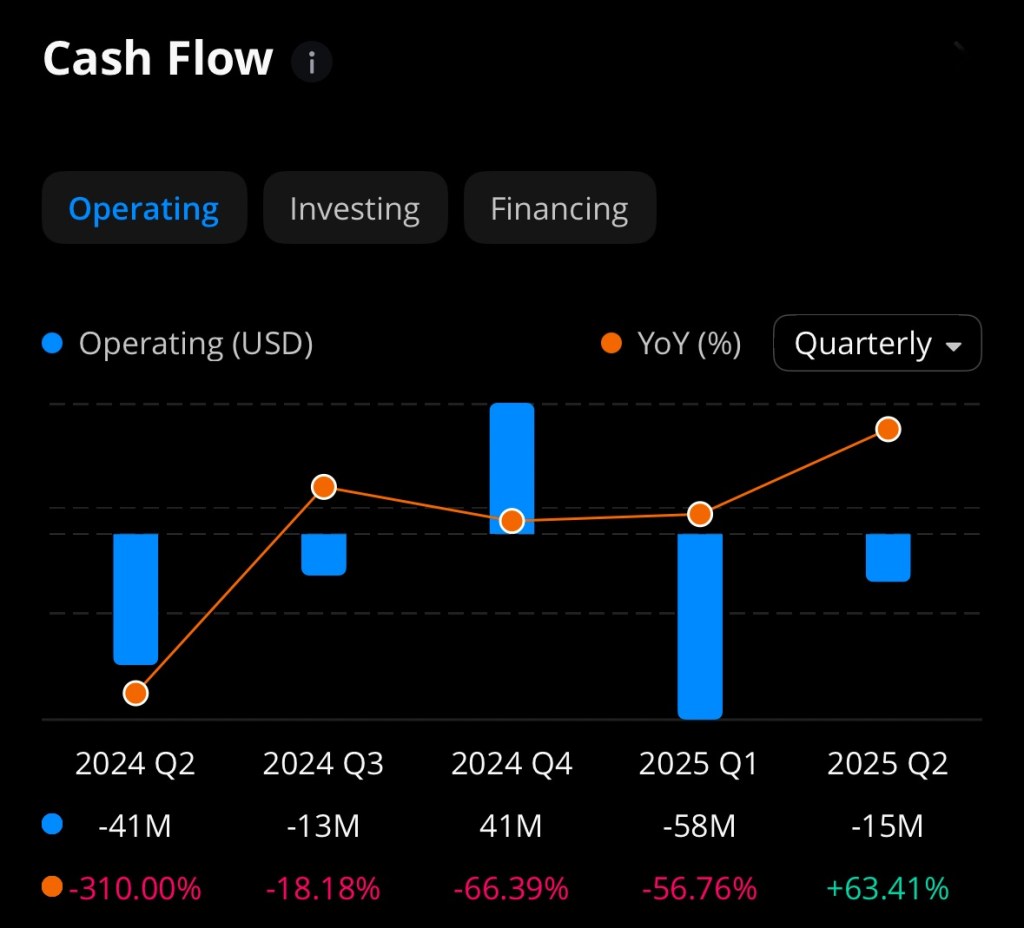

Conduent Incorporated, the business-process-services company spun out from Xerox, reported mixed results through early 2025 as it works to convert cost cuts and restructuring into sustainable profit. The shares trade at a low single-digit price level, making the company a high-beta, speculative play for investors who believe management can consistently deliver margin improvement and free cash flow growth. (Conduent Investor)

Key headlines (what just happened)

Conduent reported second-quarter 2025 results in early August with revenue of roughly $754 million and GAAP net loss on a standalone basis (but continued improvements in adjusted metrics were highlighted by management). (Conduent Investor)

The company’s market capitalization sits in the hundreds of millions (Yahoo Finance shows market cap in the ~$440–460M range around current quotes), while enterprise value is notably higher because of net debt on the balance sheet. The stock price is trading near $2.80–$3.00 per share as of this writing. (Yahoo Finance)

Balance-sheet and financial-position analysis

Using the company filings and aggregated financial data, the balance-sheet picture for Conduent in the most recent filings shows several important characteristics:

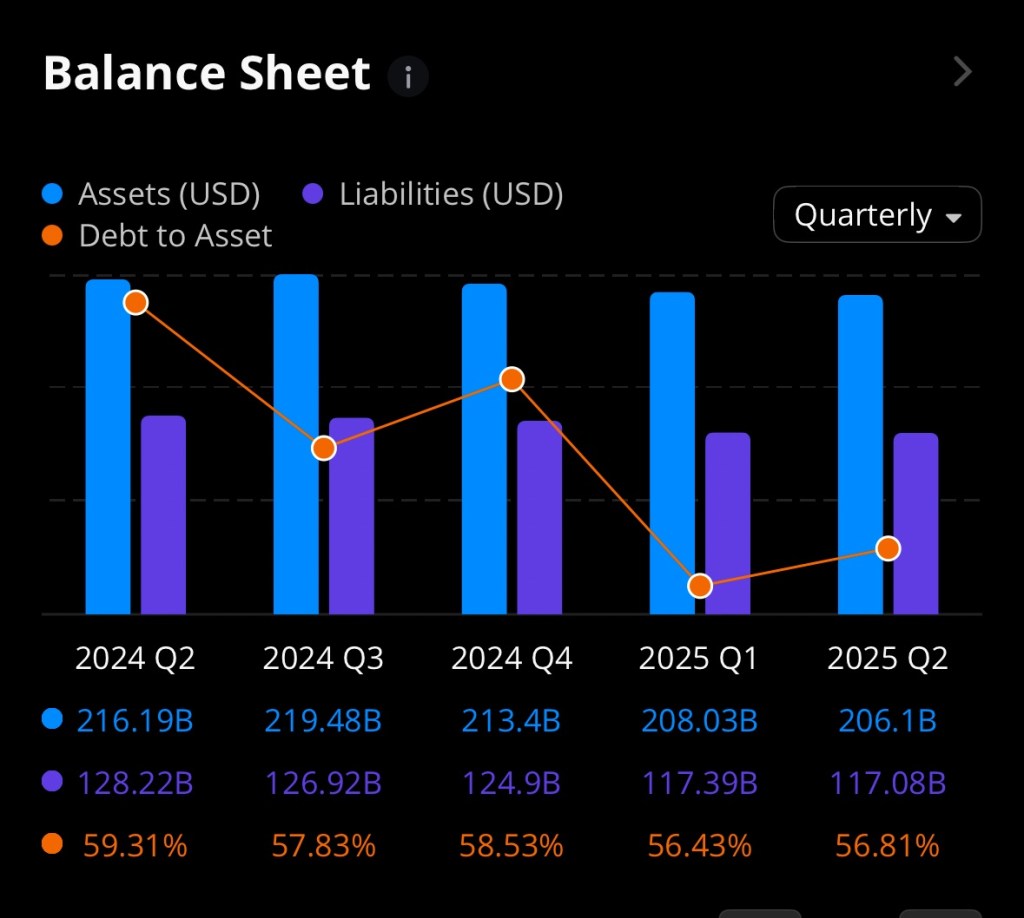

Total assets / liabilities: Conduent’s total assets in recent annual/quarterly filings have been in the low-to-mid billions (annual totals around $2.6B–$3.2B), with total liabilities making up a substantial portion of that base. That translates to relatively thin shareholder equity compared with larger peers. (Yahoo Finance+1)

Leverage / net debt: Total long-term debt has historically been material — recent snapshots put total debt roughly in the high hundreds of millions to over $1B (enterprise value and total debt differ by source and date) — and net cash/(debt) has been negative (i.e., net debt). StockAnalysis and other aggregators show net debt in the several-hundred-million range. That means Conduent’s EV is meaningfully larger than its market cap. (StockAnalysis+1)

Liquidity: Management has emphasized cash on hand and the revolving credit facility as sources of near-term liquidity in SEC filings and the latest 10-Q/earnings commentary; operating cash flow is a key metric to watch as the company seeks to deleverage. The company stated it believes its cash, projected operating cash flow and its revolving credit line support near-term needs. (Conduent Investor+1)

Interpretation: Conduent is a balance-sheet–constrained turnaround: not insolvent, but carrying leverage that raises the bar for operational execution. If revenue growth stalls or free cash flow fails to materialize, debt servicing and refinancing risk become real constraints.

Income-statement & cash-flow highlights

Revenue trend: Revenues have been in the ~$3.3B range on an annual basis (2023–2024 levels per public filings and financial aggregators), with sequential quarter fluctuations due to contract timing and divestitures. Recent quarters in 2025 showed revenue in the mid-$700M range per quarter. (Yahoo Finance+1)

Profitability: GAAP results have cycled between losses and small profits in recent years; management prefers adjusted EBITDA/adjusted metrics that show margin improvement after restructuring. For investors, the question is whether adjusted profit improvement converts to consistent GAAP profitability and positive operating cash flow. (Conduent Investor+1)

Cash flow: Free-cash-flow generation has been variable. The company highlights projected cash flow from operations as a pillar of its liquidity, but historical net debt and working-capital swings mean investors should track quarterly cash-flow statements, not just headline operating results. (Conduent Investor+1)

Valuation and risks

Valuation: On a trailing basis Conduent’s P/E (when positive) and EV multiples are compressed versus stable peers because of the elevated leverage and inconsistent earnings. Market cap (sub-$500M range) compared with enterprise value near ~$1B indicates investors price in significant debt and execution risk. (Yahoo Finance+1)

Catalysts for upside: sustained adjusted-EBITDA growth, consistent GAAP profitability, meaningful free cash flow, and visible debt reduction would be strong upside catalysts. Contract wins or higher-margin mix (e.g., digital-services expansion) could improve investor sentiment. (Conduent Investor)

Downside risks: failure to convert adjusted metrics to real cash, large contract losses, macro pressure on customers (public-sector budgets, transportation spending shifts), or refinancing stress on debt.

Recommendation (straight answer)

For conservative investors: Conduent is not suitable. The balance sheet shows leverage and earnings volatility; until management demonstrably converts adjusted profits into recurring GAAP profits and consistent positive free cash flow, the stock is a speculative holding at best. (StockAnalysis+1)

For risk-tolerant investors / traders seeking gains: Conduent’s low absolute market cap and depressed share price create asymmetric upside if execution improves. That makes it a potential high-risk, event-driven trade — buy only a small allocation, be prepared for high volatility, and plan an exit strategy tied to specific milestones (e.g., two to three consecutive quarters of positive operating cash flow or a material debt-reduction announcement). Use strict position sizing and stop rules. (Conduent Investor)

What to watch next (actionable checklist)

Quarterly cash-flow from operations (is it consistently positive?). (Conduent Investor)

Net debt trend — any sustained debt paydown or refinancing on better terms. (StockAnalysis)

Revenue mix — growth in higher-margin digital services vs. legacy BPO work. (Conduent Investor)

This article relied on Conduent’s investor relations releases and SEC filings, plus market data aggregators (Yahoo Finance, StockAnalysis, Macrotrends, Nasdaq) for pricing, market cap and historical financial statements. Key sources: Conduent investor releases and 10-Q/10-K filings, Yahoo Finance price & key statistics, and StockAnalysis balance-sheet pages. (StockAnalysis+3Conduent Investor+3Conduent Investor+3)

Bottom line: Conduent is a turnaround story with a leveraged balance sheet. If you believe management will convert improved adjusted margins into recurring cash and pay down debt, the stock offers speculative upside from a depressed base. If you require capital preservation and predictable returns, this is better left alone. Keep position sizing small, watch cash flow and net-debt trends, and tie any buy decision to concrete operational milestones. (Conduent Investor+1)

References

Conduent Incorporated. (2025, August 6). Conduent reports second quarter 2025 results [Press release]. Conduent Investor Relations. https://investor.conduent.com

Conduent Incorporated. (2025). Form 10-Q for the quarterly period ended June 30, 2025. U.S. Securities and Exchange Commission. https://www.sec.gov

High Dividend Yield & Track Record Target currently pays $4.56 annually ($1.14 per quarter), translating into a robust ~4.9% yield on today’s ~$93 share price (StockAnalysisTipRanks). The company has increased its dividend for 54 consecutive years, a hallmark Dividend King that inspires investor confidence (NasdaqStockAnalysis). Its most recent raise (1.8%) was declared in June 2025, effective with the $1.14 quarterly payment on Sept 1, 2025 (ex-div Aug 13) (Target Corporation).

Payout Coverage & Sustainability Target retains a payout ratio of roughly 52%—meaning it distributes just over half of earnings as dividends, leaving room to reinvest and buffer downturns (KoyfinStockAnalysis). It also generated ~$2.9 B in free cash flow over the past 12 months, comfortably above its roughly $2 B annual dividend obligation (Nasdaq).

Valuation Lean vs Peers At a P/E near 11×, Target trades well below peers like Walmart (~37×), suggesting the market has priced in current headwinds—offering potential upside if operational trends normalize over time (Nasdaq).

🧾 Balance Sheet Overview (as of latest trailing 12 mo / August 2025)

Target maintains a healthy asset base, anchored by substantial property, inventory, and cash buffers. Long‐term debt is sizable but manageable given recurring cash flow. Equity has grown steadily (~$14.7 B in FY 2024 to ~$15.4 B TTM), with tangible book value per share near $34—over one-third of share price (StockAnalysis).

🔍 Business Momentum & Outlook

Recent performance (Q2 FY 2025): Net sales declined ~0.9% YoY and comp sales fell ~1.9%, though digital sales rose ~4.3%. Operating income slipped ~19% to $1.3 B. Full-year EPS guidance remains at $8.00–$10.00 GAAP (adjusted ~$7–$9) (Target Corporation).

Strategic tailwinds: Investments in same-day fulfillment via Shipt, modernization of logistics, and omnichannel integration are expected to drive margin recovery (expected to improve toward ~6% by FY 2028) (University of Iowa).

💡 Investment Case: Why Consider TGT

Reliable, high income: ~4.9–5.0% yield, backed by decades of increases.

Dividend sustainability: Strong cash flow vs payout; modest payout ratio.

Undemanding valuation: Trading at low P/E, offering value if business stabilizes.

Long-term turnaround potential: Operational improvements could bolster margins and share price over time.

Risks include macro-sensitive retail environment, margin pressures, inventory mismanagement, and stiff competition. However, the dividend acts as a buffer while strategic moves take root.

📌 Bottom Line

For income-focused investors looking to pair dividend yield with capital appreciation potential, Target (TGT) stands out as a compelling blended opportunity. Its long-standing dividend credibility, backed by solid free cash flow and a durable balance sheet, makes it a defensive anchor in a portfolio. Coupled with low valuation and a clear path to operational recovery, TGT offers both yield today and upside tomorrow.

Disclosure: I currently hold a position in Target Corporation (NASDAQ: $TGT). This article reflects my personal opinions and analysis, and is not intended as financial advice. Please conduct your own research or consult a financial advisor before making any investment decisions.

Success is often measured in numbers—bank accounts, investments, or even social media followers—the deeper meaning of being both healthy and wealthy can sometimes get lost. For me, the phrase isn’t about chasing material excess, but about balance, fulfillment, and sustainability in both body and mind.

Health as the Foundation Health is more than the absence of illness; it’s the daily practice of treating your body and mind with respect. For me, that includes maintaining energy to do the things I love, fueling my body with good food, and taking time to reduce stress. Without health, even the greatest fortune feels empty. Wealth is meaningless if you don’t have the strength or clarity to enjoy it.

Wealth Beyond Money When I think of being “wealthy,” I don’t immediately picture luxury cars or sprawling mansions. Instead, I see freedom—the freedom to spend time with loved ones, pursue passions, and give back to the community. True wealth, to me, includes financial security, but also peace of mind, strong relationships, and opportunities to grow.

Healthy and Wealthy Together The two go hand in hand. Being healthy allows me to work toward financial stability with focus and determination. Being financially stable allows me to invest in my health—whether that’s quality healthcare, nutritious food, or the ability to take time off when I need it. Together, they create a cycle that builds not just a lifestyle, but a legacy.

A Personal Vision Ultimately, “healthy and wealthy” means living in a way that supports long-term happiness. It’s about waking up each day with energy, knowing I have the resources to handle life’s challenges, and feeling grateful for both the small and big wins. To me, that’s real success—being rich in health, rich in love, and rich in purpose.

Pfizer Inc. ($PFE), one of the world’s largest pharmaceutical companies, continues to make a strong case for long-term investors seeking both stability and income. While the stock has faced recent volatility due to a decline in COVID-19 vaccine sales, its solid fundamentals, diversified pipeline, and consistent dividend payouts remain key reasons why investors may want to hold shares for the long haul.

Pfizer currently offers an attractive dividend yield—well above the S&P 500 average—making it a compelling choice for income-focused portfolios. The company has a long track record of reliable dividend payments and has shown commitment to rewarding shareholders even during periods of industry and market uncertainty. With a payout ratio supported by its robust cash flow, Pfizer’s dividend looks sustainable in the years ahead.

Beyond dividends, Pfizer’s pipeline of treatments in oncology, immunology, and rare diseases provides investors with growth opportunities outside of its COVID-19 products. Recent strategic acquisitions, such as the purchase of Seagen to bolster its oncology portfolio, reinforce the company’s long-term vision. These moves are designed to balance near-term headwinds with future revenue expansion.

Financial Snapshot: Strengths and Weaknesses

Strengths

Dividend Yield & Stability: Pfizer’s dividend yield is significantly higher than the S&P 500 average, appealing to income-focused investors.

Strong Balance Sheet: Despite recent revenue declines, Pfizer maintains healthy cash reserves and strong operating cash flow, supporting its dividend and acquisition strategy.

Attractive Valuation: Shares are trading at a discount compared to peers in the pharmaceutical sector, offering a margin of safety for value investors.

Diversified Revenue Base: Expansion in oncology, vaccines, and rare diseases provides multiple future growth drivers beyond COVID-19.

Weaknesses

COVID-19 Dependency Hangover: A sharp decline in vaccine and antiviral demand has pressured revenue, highlighting reliance on pandemic-era products.

R&D Risk: Heavy investment in research and development may not always lead to successful approvals, leaving earnings vulnerable.

Debt from Acquisitions: The Seagen deal adds to Pfizer’s debt load, which, while manageable, could strain resources if integration challenges arise.

Patent Expirations: Like many pharmaceutical giants, Pfizer faces long-term risks from patent cliffs that could erode future revenue streams.

Stock Price Outlook: 1 to 5 Years

Pfizer’s current share price reflects market concerns over post-COVID revenue declines, but its fundamentals suggest room for recovery.

12-Month View (2025–2026): Analysts see potential for modest gains, with shares trading in the $32–$38 range as the market digests lower vaccine revenues but begins to price in oncology and pipeline growth. The dividend will continue to anchor returns even if share price growth is muted.

3-Year View (2027): As new oncology therapies, rare-disease drugs, and vaccine innovations mature, Pfizer could see revenue stabilize and return to growth. A reasonable target range could be $40–$48 per share, supported by mid-single-digit revenue growth and steady dividends.

5-Year View (2029–2030): If Pfizer successfully integrates Seagen, brings key drugs to market, and manages upcoming patent expirations, long-term investors could see shares trading in the $50–$60 range. Dividend reinvestment along the way would enhance total returns, making Pfizer a solid long-term hold for income plus growth.

While uncertainty remains in the short term, Pfizer’s combination of a reliable dividend, undervaluation relative to peers, and a promising pipeline suggests patient investors may be rewarded over a 5-year horizon.

Disclosure: I currently hold a position in Pifzer (NASDAQ: $PFE). This article reflects my personal opinions and analysis, and is not intended as financial advice. Please conduct your own research or consult a financial advisor before making any investment decisions.

When it comes to protecting wealth and passing it on to loved ones, many families are discovering that a simple will may not be enough. Increasingly, individuals are turning to trusts as a more effective way to manage their assets and provide security for beneficiaries. While wills remain common, trusts offer unique advantages that make them an essential tool in modern estate planning.

A trust is a legal arrangement in which a trustee manages assets on behalf of beneficiaries. Unlike a will, which becomes public during probate, a trust can keep family financial matters private while ensuring assets are distributed according to the grantor’s wishes.

Avoiding Probate Delays and Costs One of the main reasons individuals choose a trust is to avoid probate—the court-supervised process of distributing an estate after death. Probate can take months or even years, and legal fees can significantly reduce what heirs actually receive. With a trust, assets are transferred more quickly and with fewer administrative costs.

Tax Efficiency and Asset Protection Certain types of trusts can also provide tax advantages. For high-net-worth individuals, this can mean minimizing estate taxes, while others use trusts to shield assets from creditors or lawsuits. Parents of minor children often create trusts to ensure their children’s financial needs are met in the event of an untimely death.

Control Over Distribution Unlike a will, which typically results in a lump-sum transfer of assets, a trust allows for customized distribution. For example, beneficiaries can receive funds at certain ages, in installments, or for specific purposes such as education or healthcare. This level of control provides peace of mind for those worried about heirs’ financial responsibility.

Peace of Mind for Families “Trusts aren’t just for the wealthy,” says estate planning attorney Sarah Mitchell. “They’re tools that provide structure, protection, and clarity—things every family can benefit from. For many clients, it’s about peace of mind knowing their loved ones are taken care of.”

As life expectancy increases and wealth is passed down through generations, experts predict that more families will explore trusts as part of their financial planning. Whether it’s avoiding probate, protecting assets, or ensuring responsible inheritance, trusts are becoming a cornerstone of modern estate planning.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Some quantitative models project a steep upward trajectory. One forecasting service estimates an average December 2025 price of $34.67, with a low of $32.18 and a high of $35.72—implying over 100% upside from current levels (StockScan). If investor sentiment catches up with this model, the stock could indeed flirt with $40 before year-end.

2. Financing Strength and Cash Position

As of March 31, 2025, Oscar Health reported a fortified balance sheet: $4.86 billion in cash, equivalents, and investments, up from $3.97 billion at the end of 2024. Total assets rose 21% YoY, while operating cash flow increased 38% (Michael Burry’s Insights). This cash cushion gives Oscar flexibility to invest in growth, navigate regulatory headwinds, and drive further value.

3. Strategic Expansion Through New Partnerships

Oscar’s deal with Hy-Vee to launch “Hy-Vee Health with Oscar” in Des Moines, covering about 400,000 employees in the individual marketplace starting Jan 1, 2026, signals a bold move into employer-backed coverage. The ICHRA model aims to save businesses 20–30% and deliver substantial cost-savings to employees-this could create significant scale and margin tailwinds (Benzinga).

4. Accelerating Revenue Growth

While Q2 revenue of $2.86 billion fell slightly short of the $2.91 billion estimate, it still marked a 29% increase YoY. The company reaffirmed its full-year 2025 revenue guidance at $12–12.2 billion (versus Wall Street’s $11.32 billion estimate), underscoring underlying growth momentum (BenzingaYahoo FinanceStockAnalysis).

5. Valuation Appears Undervalued for Growth Potential

Oscar trades at over 101x forward EV/EBITDA, a lofty multiple—but some analysts argue this valuation is justified by its “quality characteristics” and disruptive business model (StockStory). Others see it as deeply undervalued despite near-term uncertainty tied to ACA policy risks (Seeking Alpha+1).

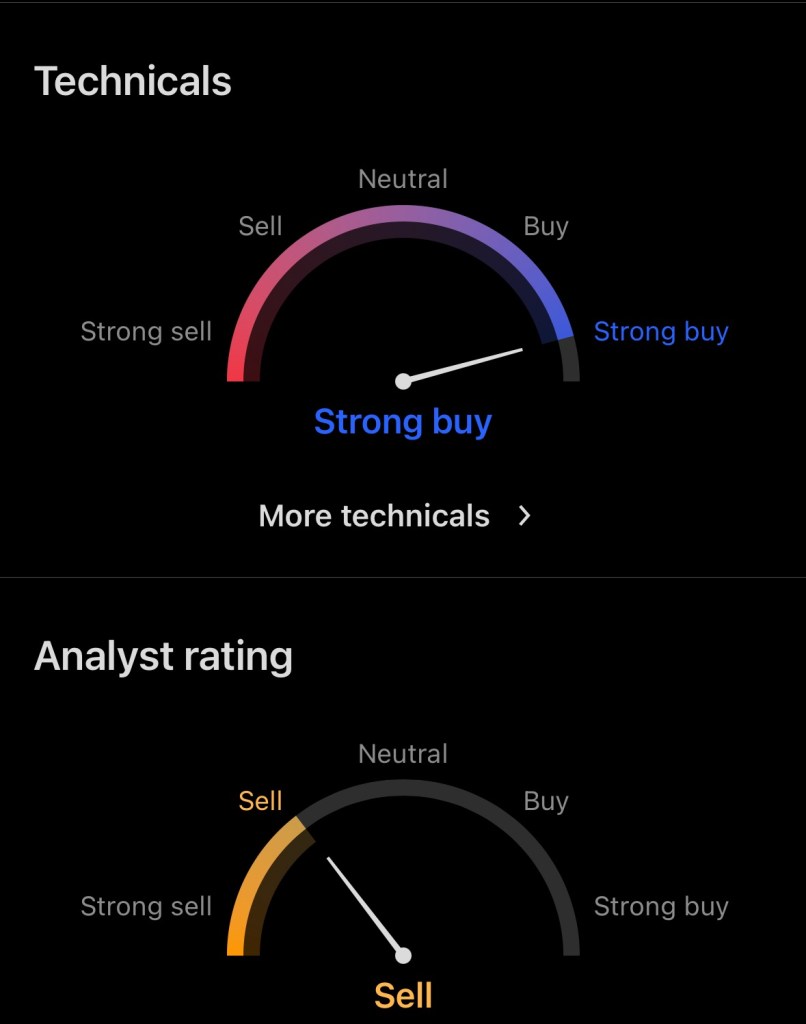

Skeptical Market Sentiment: Many brokerages hold “Sell,” “Hold,” or “Neutral” ratings. Notably, Piper Sandler cut its target from $14 to $13, citing uncertainties around risk adjustments and path to profitability (Benzinga). MarketBeat’s consensus is “Strong Sell,” and TipRanks flags a “Downside potential” of ~30% (MarketBeat).

Profitability Still Out of Reach in 2025: OSCR is expected to operate at a loss—losses projected around $200–300 million for the year (Yahoo Finance). Its Q2 GAAP loss was $0.89/share, and medical loss ratio (MLR) swelled from 79% in 2024 to 91.1% in Q2 2025 (BenzingaStockAnalysis). These factors dampen bullish expectations.

Headlines-Style Article: “Oscar Health: Can It Make the Leap to $40 by Christmas 2025?”

New York, August 23, 2025 – Oscar Health Inc. (NYSE: OSCR) currently trades near $16.98, buoyed by stellar revenue growth, robust liquidity, and a landmark new partnership but Wall Street’s confidence remains tepid.

Why $40 isn’t implausible:

Long-term algorithmic forecasts place December 2025 prices in the low-$30s, including a possible high of $35.72 (StockScan).

Strengthened cash position of $4.86 billion, coupled with rising operating cash flows, enhances the company’s financial flexibility (Michael Burry’s Insights).

Innovative ventures like the Hy-Vee collaboration, targeting 400,000 employees, position Oscar to disrupt cost structures and tap new revenue streams (Benzinga).

A confirmed revenue guidance of $12–12.2 billion highlights strong underlying demand despite macro-healthcare headwinds (Yahoo FinanceStockAnalysis).

Profitability is still elusive: projected operational losses of up to $300 million in 2025, and increased medical loss ratios (MLR) eroding margins (BenzingaYahoo FinanceStockAnalysis).

Sentiment skews negative, with ratings from “Hold” to “Strong Sell” prevailing, reflecting elevated policy-related and insurance-market risks (MarketBeat).

Final Thoughts: While consensus targets place Oscar Health under $15, a confluence of strong cash reserves, growth initiatives, and bullish long-term models could propel the stock into the low $30s by Christmas-though doing so would require sustained execution and favorable market sentiment in the face of continued near-term challenges.

Disclaimer: The author holds a position in $OSCR Oscar Healthcare and this article should not be considered financial advice. Always conduct your own research before making any investment decisions.

When it comes to motorcycles, boats, golf carts, and ATVs, most people think about the thrill of the ride, the open water, or a sunny day on the course-not the financial risks. But accidents, theft, and unexpected liabilities don’t take a holiday, and that’s why insurance for your recreational “toys” is worth serious consideration.

Required vs. Optional Coverage

The first step in understanding toy insurance is knowing what’s required by law and what’s optional.

Motorcycles: Like cars, most states require liability insurance if you’re taking your motorcycle on public roads. This covers injury or damage you may cause to others, but not your own bike. Collision and comprehensive coverage—protecting your motorcycle against accidents, theft, or weather damage are optional but highly recommended.

Boats: While boat insurance isn’t federally mandated, some states and marinas require proof of coverage. Even if it’s not required, carrying liability and property protection can shield you from costly repairs or lawsuits if an accident occurs on the water.

ATVs & Dirt Bikes: If you’re riding on private land, insurance is usually optional. However, many state parks, trails, and off-road areas require proof of coverage to operate. Considering the high rate of ATV accidents and theft, insuring your four-wheeler is a smart move.

Golf Carts: Most neighborhoods and golf courses don’t require golf cart insurance, but if you’re using the cart on public roads-or even just around your community-liability coverage can protect you if an accident happens. Some homeowners’ policies provide limited coverage, but standalone golf cart insurance can fill the gaps.

Why You Should Insure Even When It’s Optional

Just because coverage isn’t required doesn’t mean it isn’t essential. Repair costs, medical bills, or liability lawsuits can quickly outweigh the value of your toy itself. Theft is another growing concern-ATVs, motorcycles, and even boats are among the most commonly stolen recreational vehicles.

Insurance not only protects your investment but also your financial stability. For many, the peace of mind of knowing that a fun weekend won’t turn into a financial nightmare is worth the modest premium.

A Smarter Way to Protect Your Fun

Your recreational vehicles are more than just “toys”-they’re part of your lifestyle. Adding the right insurance ensures that your good times don’t come with unnecessary risks. Before the next ride, round of golf, or day on the water, check your coverage and make sure your adventures are backed by protection as strong as your passion.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

When you hand over your car keys to a friend or family member, you might not think twice. But in the world of auto insurance, that moment is about more than just trust-it’s about something called permissive use.

What Is Permissive Use?

Permissive use simply means you’ve allowed someone else to drive your vehicle with your permission. That permission can be:

Express – You clearly told them they could drive your car.

Implied – It’s understood based on your relationship or past behavior (e.g., your spouse or roommate regularly uses your car without asking each time).

In most standard auto insurance policies, permissive users are covered under the vehicle owner’s liability coverage. That means if the driver gets into an accident while using your car with your consent, your policy can help pay for damages or injuries to others.

Why Understanding Permissive Use Matters

You Could Be Financially Responsible Even if you weren’t behind the wheel, your insurance may still be the first to pay if a permissive user causes an accident. If damages exceed your policy limits, you could be responsible for the difference.

Coverage Isn’t Always Unlimited Some insurance companies provide reduced coverage limits for permissive drivers-especially if they’re not listed on your policy. Others might exclude certain drivers altogether.

Not All Situations Are Covered If the person using your car is engaging in excluded activities-like delivering food for a rideshare app, racing, or using the vehicle without permission—your insurance might not apply.

Claims Can Affect Your Record An accident caused by a permissive user can still appear on your insurance history and may impact your premiums.

How to Protect Yourself When Sharing Your Vehicle

Know Your Policy – Check your policy documents or talk to your agent to understand how your insurer handles permissive use.

Be Selective – Only allow responsible, licensed drivers to use your vehicle.

Clarify Restrictions – If you don’t want someone driving for certain purposes (like work deliveries), make that clear.

List Regular Drivers – If someone uses your car often, consider adding them to your policy to avoid coverage gaps.

Key Takeaway for Drivers

Permissive use may feel like a small favor, but it carries big insurance implications. By knowing the rules, choosing drivers wisely, and keeping your policy updated, you can avoid unpleasant surprises and keep both your car and your finances protected.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.