Across the country, homeowners are facing rising insurance premiums as insurance companies respond to increasing claims, inflation, severe weather events, and aging housing stock. While many homeowners focus on shopping for lower rates, one of the most overlooked factors affecting premiums is the condition of the home itself.

Insurance companies are paying closer attention than ever to property maintenance. Advances in aerial imagery, satellite technology, drones, and property inspection software allow insurers to identify potential hazards without ever stepping inside a home.

The result? A roof nearing the end of its life, deteriorating plumbing, outdated electrical systems, or neglected exterior maintenance can lead to premium increases, non-renewal notices, or even cancellation of coverage.

Why Maintenance Matters

Insurance is based on risk. The greater the likelihood that a claim will occur, the higher the premium charged to insure that risk.

For example:

- An aging roof is more likely to leak or sustain storm damage.

- Old plumbing systems increase the risk of water damage claims.

- Outdated electrical systems increase fire risk.

- Dead trees and damaged siding create additional exposure during severe weather events.

From an insurer’s perspective, a well-maintained home represents a lower probability of costly claims.

The Hidden Cost of Deferred Maintenance

Many homeowners postpone repairs to save money. Unfortunately, the long-term costs can be much greater.

Consider a roof that should have been replaced five years ago. Not only may the homeowner face higher premiums, but a future claim could be limited or denied if the damage is determined to result from wear and tear rather than a sudden covered event.

Similarly, a small plumbing leak left unaddressed can eventually lead to thousands of dollars in water damage and mold remediation expenses.

Estimated Repair Costs and Potential Insurance Benefits

The following estimates represent typical costs in today’s market. Actual costs vary based on location, home size, and materials used.

| Home Improvement | Estimated Cost | Potential Insurance Impact |

|---|---|---|

| New Roof | $12,000 – $30,000 | Lower premiums and improved eligibility for coverage |

| Electrical Panel Upgrade | $2,000 – $6,000 | Reduced fire risk may qualify for credits |

| Whole Home Re-Plumbing | $4,000 – $15,000 | Reduced water damage exposure |

| Hurricane Impact Windows | $10,000 – $30,000 | Significant wind mitigation discounts in many states |

| HVAC Replacement | $5,000 – $12,000 | Reduced risk of system-related losses |

| Water Leak Detection System | $500 – $2,500 | Discounts offered by some insurers |

| Garage Door Wind Upgrade | $1,500 – $5,000 | Windstorm mitigation credits |

| Exterior Painting and Siding Repair | $3,000 – $15,000 | Improves insurability and property condition scores |

| Tree Removal Near Structure | $500 – $5,000 | Reduces storm-related claim risk |

| Security System Installation | $300 – $2,000 | Potential theft and fire protection discounts |

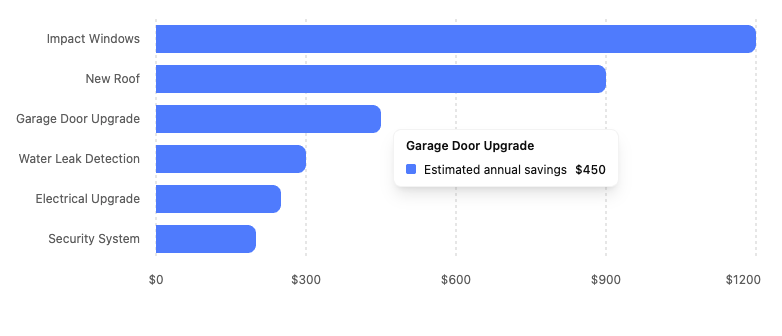

Estimated Annual Premium Savings

While every insurer is different, homeowners may see reductions ranging from modest to substantial depending on the improvement completed.

Potential annual homeowners insurance savings

Illustrative annual savings after major home improvements. Actual savings vary by insurer, location, and home characteristics.

Florida Homeowners Face Unique Challenges

Homeowners in Florida have experienced some of the nation’s largest insurance premium increases in recent years. Windstorm exposure, hurricane losses, litigation costs, and reinsurance expenses have dramatically impacted the market.

For Florida homeowners, improvements such as:

- New roofs

- Impact-resistant windows

- Reinforced garage doors

- Updated roof-to-wall connections

can often produce meaningful insurance savings through wind mitigation programs while simultaneously strengthening the home against future storms.

The Takeaway

Your home is likely your largest financial asset. Maintaining it properly not only protects its value but can also help keep insurance costs under control.

Before renewing your homeowners insurance policy, consider reviewing the age and condition of major systems throughout your home. A repair that seems expensive today may ultimately save thousands of dollars in future claims, prevent coverage issues, and reduce annual insurance premiums for years to come.

Disclosure: This article is intended for educational purposes only and should not be considered insurance, legal, or financial advice. Insurance eligibility, discounts, and premiums vary by carrier, location, and individual underwriting guidelines.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.