When it comes to homeowners insurance, most people focus on protecting their property from fire, theft, or storm damage. But one of the most overlooked—and most important—aspects of your policy is liability coverage. This protection kicks in when someone is injured on your property or if you accidentally cause damage to someone else’s property. And if you’re hiring contractors to work on your home, ensuring they’re properly insured could save you from financial disaster.

Understanding Liability Limits

Every homeowners insurance policy includes personal liability coverage, typically starting around $100,000 but often ranging up to $500,000 or more. This coverage helps pay for medical bills, legal fees, and settlements if you’re found responsible for an injury or property damage.

For example, if a guest slips on your icy driveway or a tree from your yard damages your neighbor’s fence, your liability coverage helps cover those costs. But here’s the catch—if damages exceed your policy limit, you’re personally responsible for the rest.

That’s why many insurance professionals recommend reviewing your limits regularly and considering an umbrella policy for extra protection. An umbrella policy can provide an additional $1 million or more in liability coverage for a relatively small cost each year.

The Hidden Risk of Uninsured Contractors

Home improvement projects often involve hiring outside help—roofers, electricians, painters, or landscapers. But before you hand over the keys or cut that first check, it’s critical to make sure any contractor working on your property carries their own liability and workers’ compensation insurance.

If a contractor is uninsured and one of their workers gets hurt on your property, you could be held liable for medical expenses, lost wages, or even lawsuits. Similarly, if they accidentally damage your home or a neighbor’s property, and they’re not covered, your own insurance might have to step in—potentially driving up your premiums or leaving you with out-of-pocket costs.

Protecting Yourself and Your Investment

Your homeowners insurance does more than protect your house—it protects your financial future. By maintaining sufficient liability limits and ensuring contractors are properly insured, you can avoid costly surprises if something goes wrong. A few minutes of due diligence today can save you thousands—and a lot of stress—tomorrow.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Quick take: Zeta Global, the AI-driven marketing cloud, has delivered a string of better-than-expected quarters, is guiding to another year of strong revenue growth, and just made a big acquisition to expand its loyalty and enterprise footprint. That combination accelerating revenue, improving profitability guidance, and strategic M&A is why some investors are re-rating the stock. Below: the facts, the catalyst, a compact risk view, and a chart/table that show the growth story.

Headlines and the data points you need

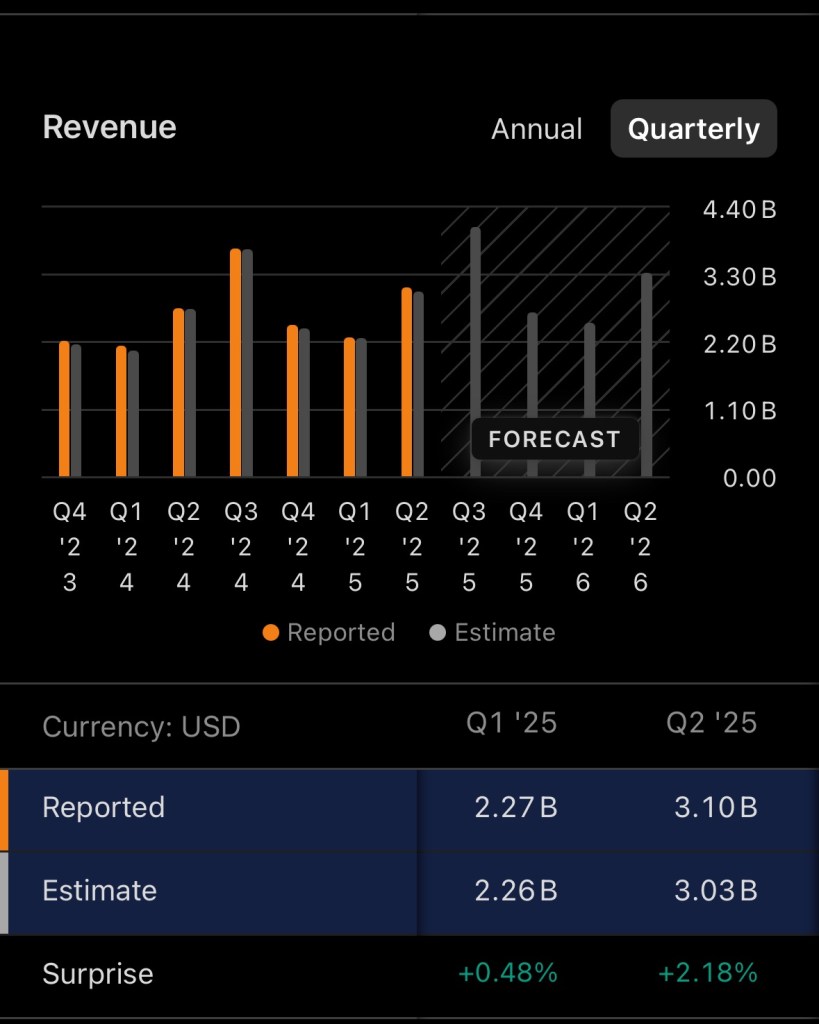

Zeta reported Q2 2025 revenue of $308.4 million, a ~35% year-over-year increase vs. the prior year quarter. (Nasdaq)

For full-year 2024 Zeta generated about $1.01 billion in revenue. (Zeta Global)

Management has repeatedly “beat and raise” most recently increasing full-year 2025 revenue guidance to $1,258–$1,268 million (midpoint ~$1.263B) and raising Adjusted-EBITDA and free-cash-flow ranges as well. Those revisions reflect faster growth and improving margins. (Zeta Global+1)

Zeta announced a large acquisition (Marigold’s enterprise business — including Cheetah Digital, Selligent, Sailthru and other assets) to strengthen loyalty and enterprise offerings, a move management says accelerates international reach and cross-sell opportunities. (Zeta Global+1)

Market snapshot (at time of writing): share price ≈ $20.37 and market cap in the mid-$4 billion range investors are paying for fast growth but also a path to profitability. (Yahoo Finance)

Why this could be an attractive investment (the bull case)

High single- to double-digit top-line growth that’s accelerating. Zeta’s recent quarters show consistent revenue acceleration (Q2 ’25 +35% YoY), a key signal for growth investors in the martech/adtech space. Management’s upward guidance for FY-2025 reinforces that it’s not just one quarter of outperformance. (Nasdaq+1)

Improving operating leverage and cash generation. The company has raised Adjusted-EBITDA and free-cash-flow guidance, pointing to margin expansion. That’s important: investors reward companies that can turn revenue growth into sustainable profits and cash. (Zeta Global)

Strategic M&A that fills capability gaps and expands addressable market. The Marigold enterprise business deal adds loyalty platforms and prominent enterprise customers (and EMEA coverage), enabling more cross-sell inside an existing customer base and a larger recurring revenue pool. If integration goes smoothly, this can boost both revenue and churn resilience. (Zeta Global+1)

Compelling unit economics at scale. Zeta reports improving ARPU (average revenue per scaled customer) and strong net revenue retention metrics, which suggest existing customers are spending more, a powerful multiplier for SaaS-like businesses. (Company disclosures highlight rising Scaled and Super-Scaled customer ARPU.) (Zeta Global+1)

Positive technical / market interest. Stock research outlets have recently upgraded technical scores (e.g., IBD RS rating rise), indicating renewed investor interest that can amplify returns if fundamentals keep improving.( Investors.com)

Visual: revenue comparison (Q2 vs prior year, FY 2024 vs FY 2025 guidance)

I created a compact chart and table comparing:

Q2 2024 (estimate) vs Q2 2025 actual, and

FY 2024 actual vs FY 2025 guidance midpoint.

(Chart and table were prepared from the company reporting and guidance figures cited above).

Sources for the plotted numbers: Q2 2025 revenue and YoY change, FY 2024 totals, and FY 2025 guidance. (Nasdaq+2Zeta Global+2)

Risks — what could go wrong

Execution risk on M&A and integration. The Marigold enterprise assets are substantial; integration issues, customer churn, or higher-than-expected costs could blunt the benefits. (Zeta Global)

Valuation vs. growth tradeoff. The stock price reflects future growth expectations. If revenue growth slows or margin expansion stalls, multiples can compress quickly. (Yahoo Finance)

Adtech / martech competition and cyclicality. The market is competitive (large incumbents and many specialists). Ad/spend cyclicality could affect revenue. Company performance depends on continued client spend and retention. (Zeta Global)

Profitability not yet fully GAAP positive. Zeta has narrowed losses but still reports GAAP net losses; investors should watch sustained EBITDA and free-cash-flow conversion. (Zeta Global)

Bottom line (concise)

Zeta Global presents a classic high-growth martech investment case: accelerating revenue, improving profitability guidance, and strategic M&A that extends its product footprint and international reach. That combination can create durable revenue expansion and margin improvement — the ingredients growth investors pay for. But the stock still carries execution and integration risk and depends on preserving high retention and ARPU. If you like fast growth with a clear path to margin expansion and accept the M&A/integration risk, Zeta is a name to research further; if you are risk-averse or need immediate GAAP profitability, it may not fit.

Disclosure:

I do not own any stock or have any financial interest in Zeta Global Holdings (NYSE: $ZETA). This article is for informational purposes only and should not be considered financial or investment advice. Investing in stocks carries risks, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

References

Zeta Global Holdings Corp. (2025, August 8). Zeta reports second quarter 2025 financial results; raises full-year 2025 guidance. Zeta Global Investor Relations. Retrieved from https://investors.zetaglobal.com/

Zeta Global Holdings Corp. (2024, February 28). Zeta reports fourth quarter and full-year 2024 results. Zeta Global Investor Relations. Retrieved from https://investors.zetaglobal.com/

Investor’s Business Daily. (2025, September). Zeta Global stock analysis and relative strength update. Investor’s Business Daily. Retrieved from https://www.investors.com/

Reuters. (2025, September). Zeta Global Holdings Corp. company profile and financial summary (ZETA.O). Reuters Markets. Retrieved from https://www.reuters.com/

MarketWatch. (2025, October). Zeta Global Holdings Corp. stock quote & financials (ZETA). MarketWatch. Retrieved from https://www.marketwatch.com/

Business Wire. (2025, July 31). Zeta Global announces acquisition of Marigold’s enterprise business to expand loyalty and EMEA presence. Business Wire. Retrieved from https://www.businesswire.com/

Yahoo Finance. (2025, October 9). Zeta Global Holdings Corp. (ZETA) stock price and market cap data. Yahoo Finance. Retrieved from https://finance.yahoo.com/

Snowflake Inc. (NYSE: $SNOW) released its second quarter (fiscal 2026) results, reinforcing its role as a data and AI infrastructure play while navigating challenges in profitability and valuation. The reaction in markets suggests that investors are increasingly viewing Snowflake as more than just a cloud data warehousing provider but as a core enabler of “AI Data Cloud” strategies. Here’s a breakdown of what’s happening, and the bull vs bear cases moving forward.

What the Numbers Say: Q2 & Recent Financials

Revenue, Margins & Growth

In Q2 FY2026, Snowflake reported product revenue of $1,090.5 million (i.e. from compute, storage, and data transfer). (Snowflake Investors)

The company continues to emphasize net revenue retention, which remains elevated (125%) as of July 31, 2025 — indicating that existing customers are expanding usage. (Snowflake Investors)

In its Q4 FY2025 results (ended January 31, 2025), Snowflake posted total revenue of $986.8 million, with product revenue of $943.3 million — up ~28% year-over-year. (Snowflake)

The Q4 gross profit margin (GAAP) was ~ 66%, and non-GAAP adjusted gross margin (excluding stock-based comp, amortization, etc.) was ~ 73%. (Snowflake)

Snowflake’s Q4 operating loss (GAAP) was about –$386.7 million, but on a non-GAAP basis it posted operating income of $92.8 million (≈ 9% margin). (Snowflake)

Its free cash flow in that quarter was ~$415.4 million (≈ 42% of revenue) and adjusted free cash flow ~$423.1 million. (Snowflake)

These numbers show both strength and tension: strong top-line growth and healthy non-GAAP profit conversions, but continued GAAP losses driven by sizable investments, stock compensation, and amortization.

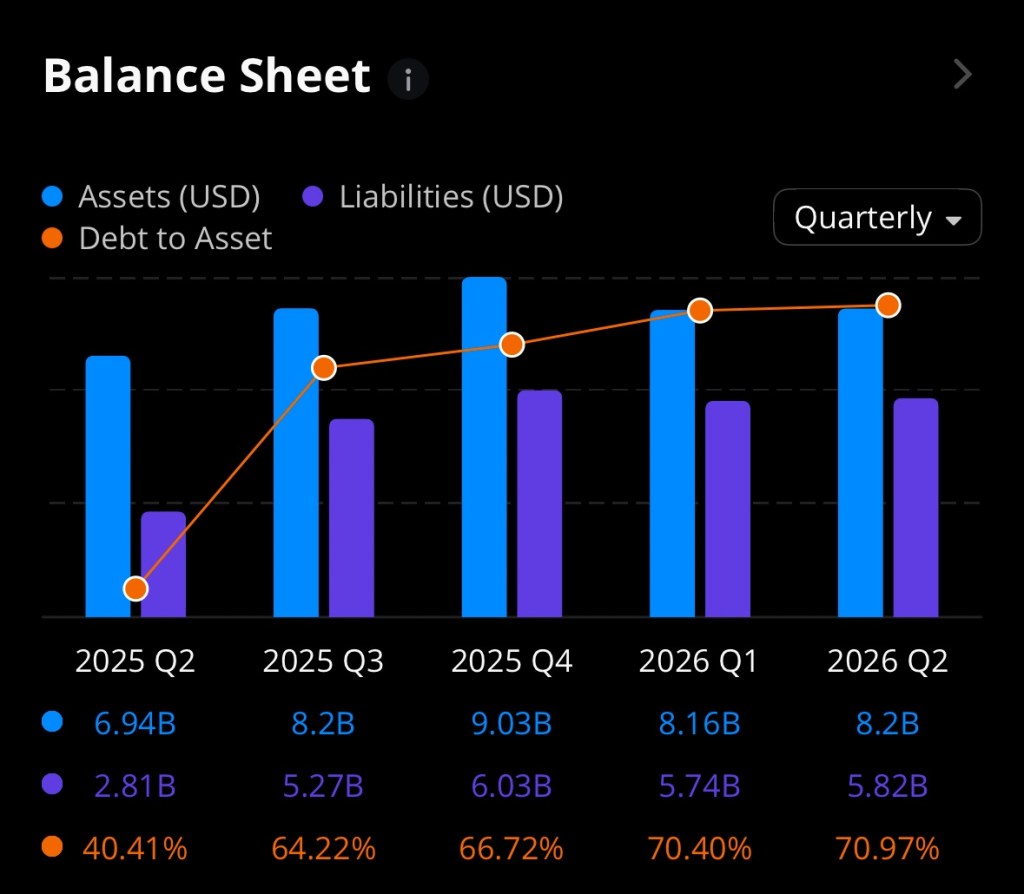

Balance Sheet & Liquidity

As of January 31, 2025, Snowflake held ~$2,698.7 million in cash, cash equivalents, and restricted cash. (Snowflake)

Total debt (short-term + long-term) is more modest for example, in recent annual balance sheet summaries, SNOW’s short-term and current portion of long-term debt is listed in the range of ~ $36 million. (The Wall Street Journal)

On the assets side, total assets are in the realm of several billions (over $8B to $9B in some reports) with growth trends consistent among public disclosures. (Investing.com+1)

The company carries significant liabilities as well (deferred revenue, vendor payables, deferred costs), but its liquidity cushion offers some buffer against short-term shocks. (Investing.com)

Business & Strategic Metrics

Snowflake’s remaining performance obligations (RPO) i.e., contracted but not-yet-recognized revenue stood at $6.9 billion, growing ~33% year-over-year. (Snowflake)

The company serves 580 customers whose trailing 12-month product revenues exceed $1 million, and 745 Forbes Global 2000 customers as of Q4 FY2025. (Snowflake)

The 125% dollar-based net revenue retention underlines that Snowflake is often able to upsell or expand within its installed base. (Snowflake Investors)

More recently, Snowflake announced its acquisition of Crunchy Data (for ~ $250 million) to integrate Postgres capabilities into its ecosystem, enabling developers to more easily build AI agents and manage data workloads. (The Wall Street Journal+1)

The company is also partnering or aligning more closely with AI/LLM providers (e.g., Anthropic), seeking to embed language model capabilities into its platform. (Reuters+2markets.businessinsider.com+2)

What’s Driving the Recent Move & Market Sentiment

In response to its Q4 FY2025 earnings (released earlier in 2025), Snowflake’s stock jumped ~10.9% after hours, as the company beat on earnings (30 cents per share vs ~18 cents expected) and revenue (nearly $987 million vs $957 million consensus). Barron’s It also raised its forecast for product revenue and delivered upbeat guidance for FY2026, projecting ~24% growth to ~$4.28 billion. (MarketWatch+2Barron’s+2)

Investors have taken notice of Snowflake’s push into AI, including more sophisticated integrations with large language models, and its efforts to position itself not just as a data platform but an “AI data cloud” enabler. (markets.businessinsider.com+2Reuters+2)

That said, concerns still linger over valuation multiples (Snowflake trades at high forward multiples), GAAP losses, and macro risk to enterprise IT spending.

Why Some Investors Might Find SNOW Attractive (and Its Risks)

Bull Case

Exposure to Secular Trends in Data + AI As enterprises shift toward AI, data modeling, real-time analytics, and agent-based applications, Snowflake sits at a nexus: you need scalable, secure data infrastructure. Its existing customer base, product maturity, and retention metrics lend credibility to that positioning.

Upsell & Expansion Potential Snowflake’s high net revenue retention and expanding average spend per customer suggest that a lot of value lies in selling more compute/storage or ancillary AI features to its installed base.

Strategic Acquisitions & Technology Stack Expansion The Crunchy Data deal, combined with its AI platform integrations, may help lock in more workloads (especially developer, data app, and AI agent workloads) and reduce friction for adoption.

Cash Generative Capacity (Non-GAAP / FCF) Despite GAAP losses, Snowflake has shown strong adjusted free cash flow generation, which gives it flexibility to invest, defend, or expand without complete reliance on external financing.

Backlog / Contracted Revenue Visibility The RPO metric provides a view into future revenue, giving some predictability to growth expectations and lessening the reliance purely on new deals.

Risks & Challenges

Profitability & Cost Pressure Snowflake still runs GAAP losses. Its heavy investment in R&D, sales & marketing, and stock-based compensation make margins sensitive. If growth slows, the pressure on margins will intensify.

Valuation Overhang At high multiples, the stock’s valuation leaves little room for mistakes. A small slip in guidance or macro softness in enterprise IT spending could cause multiple compression.

Competition & Execution Risk The competitive landscape is fierce (e.g. Databricks, AWS, Google, Microsoft) and execution (product development, scaling, integrating acquisitions) will matter enormously.

Dependence on Cloud Providers Snowflake relies on underlying public clouds (AWS, Azure, GCP) for infrastructure. Any changes in pricing, caps, or ecosystem dynamics could affect its cost structure or competitiveness. (Wikipedia+1)

Macro / IT Spend Weakness In a downturn or with tightening enterprise budgets, large IT and data platform spends may get deferred, impacting growth.

Integration and Engineering Complexity Adding deeper database, AI, and application layers increases complexity — integrating acquisitions and maintaining stability and performance across features will be demanding.

Outlook & Near-Term Catalysts

Snowflake’s guidance for Q1 FY2026 product revenue is in the range $955 million to $960 million. (Snowflake)

For full-year FY2026, the company expects ~ 24% product revenue growth to ~$4.28 billion, with non-GAAP product gross margins reaching ~75%. (Snowflake)

The success of its Crunchy Data acquisition (Postgres integration), traction of AI integrations (e.g., embedding LLMs for analytics), and customer growth in large enterprises will be closely watched.

If Snowflake can continue delivering above expectations on product revenue, manage its cost base, and ensure that its AI/data additions translate into incremental revenue without diluting execution, it may justify its premium valuation post its recent run.

Verdict & Investor Fit

Snowflake is not a “safe” stock in the sense of predictable earnings or low volatility, but it is a compelling pick for investors with conviction in the data + AI transition and a willingness to ride through lumps. For those looking for asymmetric upside exposure to the AI/data infrastructure stack, SNOW has a profile worth watching especially if bought during periods of market softness.

Disclosure:

I do not own any stock or have any financial interest in Snowflake Inc. (NYSE: $SNOW). This article is for informational purposes only and should not be considered financial or investment advice. Investing in stocks carries risks, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

When renewing your registration or handling certain vehicle-related matters at the Department of Motor Vehicles (DMV), you may be asked to provide an FS-1. For many drivers, the request sparks confusion—but the form is a crucial part of verifying compliance with state insurance laws.

What Is an FS-1? An FS-1, sometimes called a “Certificate of Insurance,” is an official document issued by your auto insurance company. It confirms that you currently carry liability insurance that meets or exceeds the minimum coverage required by your state. Unlike a regular insurance ID card, the FS-1 is not something you automatically receive when you buy a policy; it’s generated only when the DMV requests it.

Why the DMV Requests an FS-1 The DMV may request an FS-1 for several reasons, including:

Registration Renewals: To confirm your vehicle has active coverage before issuing new tags.

New Vehicle Registration: When adding a car to the road for the first time, proof of proper insurance is mandatory.

Insurance Verification Programs: States often run audits to catch lapsed or fraudulent insurance, and an FS-1 is one way to confirm coverage directly from your insurer.

After Accidents or Violations: If you’ve been cited for driving uninsured or been involved in a crash, the DMV may require the FS-1 to prove you now carry valid insurance.

What the FS-1 Does The FS-1 serves as an official communication between your insurance company and the DMV. Unlike simply showing your insurance card, the FS-1 provides legal assurance that your coverage is valid, active, and issued by a licensed carrier. It protects the state and other drivers on the road by helping ensure that every registered vehicle is financially responsible in case of an accident.

The Bottom Line If the DMV asks you for an FS-1, don’t panic. It doesn’t necessarily mean you’re in trouble—it simply means they need official verification of your insurance. Contact your insurance agent or company right away, and they can file the FS-1 directly with the DMV on your behalf.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Conduent Incorporated, the business-process-services company spun out from Xerox, reported mixed results through early 2025 as it works to convert cost cuts and restructuring into sustainable profit. The shares trade at a low single-digit price level, making the company a high-beta, speculative play for investors who believe management can consistently deliver margin improvement and free cash flow growth. (Conduent Investor)

Key headlines (what just happened)

Conduent reported second-quarter 2025 results in early August with revenue of roughly $754 million and GAAP net loss on a standalone basis (but continued improvements in adjusted metrics were highlighted by management). (Conduent Investor)

The company’s market capitalization sits in the hundreds of millions (Yahoo Finance shows market cap in the ~$440–460M range around current quotes), while enterprise value is notably higher because of net debt on the balance sheet. The stock price is trading near $2.80–$3.00 per share as of this writing. (Yahoo Finance)

Balance-sheet and financial-position analysis

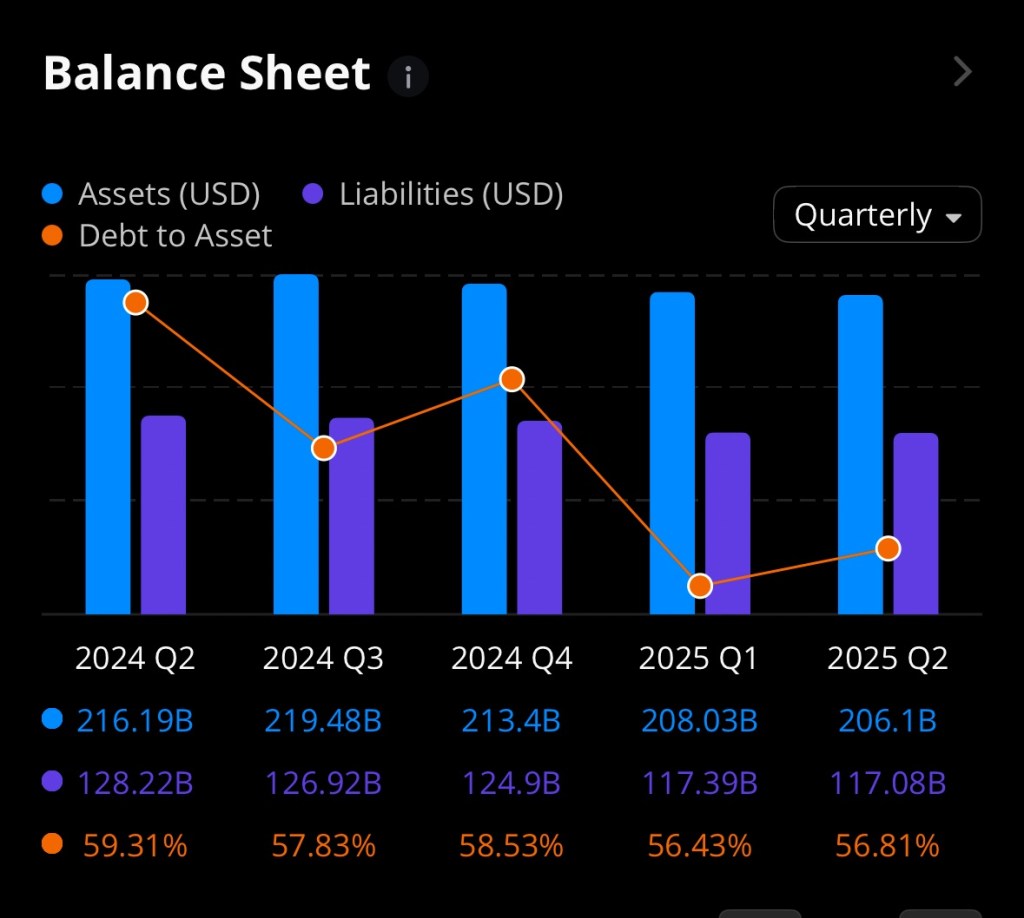

Using the company filings and aggregated financial data, the balance-sheet picture for Conduent in the most recent filings shows several important characteristics:

Total assets / liabilities: Conduent’s total assets in recent annual/quarterly filings have been in the low-to-mid billions (annual totals around $2.6B–$3.2B), with total liabilities making up a substantial portion of that base. That translates to relatively thin shareholder equity compared with larger peers. (Yahoo Finance+1)

Leverage / net debt: Total long-term debt has historically been material — recent snapshots put total debt roughly in the high hundreds of millions to over $1B (enterprise value and total debt differ by source and date) — and net cash/(debt) has been negative (i.e., net debt). StockAnalysis and other aggregators show net debt in the several-hundred-million range. That means Conduent’s EV is meaningfully larger than its market cap. (StockAnalysis+1)

Liquidity: Management has emphasized cash on hand and the revolving credit facility as sources of near-term liquidity in SEC filings and the latest 10-Q/earnings commentary; operating cash flow is a key metric to watch as the company seeks to deleverage. The company stated it believes its cash, projected operating cash flow and its revolving credit line support near-term needs. (Conduent Investor+1)

Interpretation: Conduent is a balance-sheet–constrained turnaround: not insolvent, but carrying leverage that raises the bar for operational execution. If revenue growth stalls or free cash flow fails to materialize, debt servicing and refinancing risk become real constraints.

Income-statement & cash-flow highlights

Revenue trend: Revenues have been in the ~$3.3B range on an annual basis (2023–2024 levels per public filings and financial aggregators), with sequential quarter fluctuations due to contract timing and divestitures. Recent quarters in 2025 showed revenue in the mid-$700M range per quarter. (Yahoo Finance+1)

Profitability: GAAP results have cycled between losses and small profits in recent years; management prefers adjusted EBITDA/adjusted metrics that show margin improvement after restructuring. For investors, the question is whether adjusted profit improvement converts to consistent GAAP profitability and positive operating cash flow. (Conduent Investor+1)

Cash flow: Free-cash-flow generation has been variable. The company highlights projected cash flow from operations as a pillar of its liquidity, but historical net debt and working-capital swings mean investors should track quarterly cash-flow statements, not just headline operating results. (Conduent Investor+1)

Valuation and risks

Valuation: On a trailing basis Conduent’s P/E (when positive) and EV multiples are compressed versus stable peers because of the elevated leverage and inconsistent earnings. Market cap (sub-$500M range) compared with enterprise value near ~$1B indicates investors price in significant debt and execution risk. (Yahoo Finance+1)

Catalysts for upside: sustained adjusted-EBITDA growth, consistent GAAP profitability, meaningful free cash flow, and visible debt reduction would be strong upside catalysts. Contract wins or higher-margin mix (e.g., digital-services expansion) could improve investor sentiment. (Conduent Investor)

Downside risks: failure to convert adjusted metrics to real cash, large contract losses, macro pressure on customers (public-sector budgets, transportation spending shifts), or refinancing stress on debt.

Recommendation (straight answer)

For conservative investors: Conduent is not suitable. The balance sheet shows leverage and earnings volatility; until management demonstrably converts adjusted profits into recurring GAAP profits and consistent positive free cash flow, the stock is a speculative holding at best. (StockAnalysis+1)

For risk-tolerant investors / traders seeking gains: Conduent’s low absolute market cap and depressed share price create asymmetric upside if execution improves. That makes it a potential high-risk, event-driven trade — buy only a small allocation, be prepared for high volatility, and plan an exit strategy tied to specific milestones (e.g., two to three consecutive quarters of positive operating cash flow or a material debt-reduction announcement). Use strict position sizing and stop rules. (Conduent Investor)

What to watch next (actionable checklist)

Quarterly cash-flow from operations (is it consistently positive?). (Conduent Investor)

Net debt trend — any sustained debt paydown or refinancing on better terms. (StockAnalysis)

Revenue mix — growth in higher-margin digital services vs. legacy BPO work. (Conduent Investor)

This article relied on Conduent’s investor relations releases and SEC filings, plus market data aggregators (Yahoo Finance, StockAnalysis, Macrotrends, Nasdaq) for pricing, market cap and historical financial statements. Key sources: Conduent investor releases and 10-Q/10-K filings, Yahoo Finance price & key statistics, and StockAnalysis balance-sheet pages. (StockAnalysis+3Conduent Investor+3Conduent Investor+3)

Bottom line: Conduent is a turnaround story with a leveraged balance sheet. If you believe management will convert improved adjusted margins into recurring cash and pay down debt, the stock offers speculative upside from a depressed base. If you require capital preservation and predictable returns, this is better left alone. Keep position sizing small, watch cash flow and net-debt trends, and tie any buy decision to concrete operational milestones. (Conduent Investor+1)

References

Conduent Incorporated. (2025, August 6). Conduent reports second quarter 2025 results [Press release]. Conduent Investor Relations. https://investor.conduent.com

Conduent Incorporated. (2025). Form 10-Q for the quarterly period ended June 30, 2025. U.S. Securities and Exchange Commission. https://www.sec.gov

Pfizer Inc. ($PFE), one of the world’s largest pharmaceutical companies, continues to make a strong case for long-term investors seeking both stability and income. While the stock has faced recent volatility due to a decline in COVID-19 vaccine sales, its solid fundamentals, diversified pipeline, and consistent dividend payouts remain key reasons why investors may want to hold shares for the long haul.

Pfizer currently offers an attractive dividend yield—well above the S&P 500 average—making it a compelling choice for income-focused portfolios. The company has a long track record of reliable dividend payments and has shown commitment to rewarding shareholders even during periods of industry and market uncertainty. With a payout ratio supported by its robust cash flow, Pfizer’s dividend looks sustainable in the years ahead.

Beyond dividends, Pfizer’s pipeline of treatments in oncology, immunology, and rare diseases provides investors with growth opportunities outside of its COVID-19 products. Recent strategic acquisitions, such as the purchase of Seagen to bolster its oncology portfolio, reinforce the company’s long-term vision. These moves are designed to balance near-term headwinds with future revenue expansion.

Financial Snapshot: Strengths and Weaknesses

Strengths

Dividend Yield & Stability: Pfizer’s dividend yield is significantly higher than the S&P 500 average, appealing to income-focused investors.

Strong Balance Sheet: Despite recent revenue declines, Pfizer maintains healthy cash reserves and strong operating cash flow, supporting its dividend and acquisition strategy.

Attractive Valuation: Shares are trading at a discount compared to peers in the pharmaceutical sector, offering a margin of safety for value investors.

Diversified Revenue Base: Expansion in oncology, vaccines, and rare diseases provides multiple future growth drivers beyond COVID-19.

Weaknesses

COVID-19 Dependency Hangover: A sharp decline in vaccine and antiviral demand has pressured revenue, highlighting reliance on pandemic-era products.

R&D Risk: Heavy investment in research and development may not always lead to successful approvals, leaving earnings vulnerable.

Debt from Acquisitions: The Seagen deal adds to Pfizer’s debt load, which, while manageable, could strain resources if integration challenges arise.

Patent Expirations: Like many pharmaceutical giants, Pfizer faces long-term risks from patent cliffs that could erode future revenue streams.

Stock Price Outlook: 1 to 5 Years

Pfizer’s current share price reflects market concerns over post-COVID revenue declines, but its fundamentals suggest room for recovery.

12-Month View (2025–2026): Analysts see potential for modest gains, with shares trading in the $32–$38 range as the market digests lower vaccine revenues but begins to price in oncology and pipeline growth. The dividend will continue to anchor returns even if share price growth is muted.

3-Year View (2027): As new oncology therapies, rare-disease drugs, and vaccine innovations mature, Pfizer could see revenue stabilize and return to growth. A reasonable target range could be $40–$48 per share, supported by mid-single-digit revenue growth and steady dividends.

5-Year View (2029–2030): If Pfizer successfully integrates Seagen, brings key drugs to market, and manages upcoming patent expirations, long-term investors could see shares trading in the $50–$60 range. Dividend reinvestment along the way would enhance total returns, making Pfizer a solid long-term hold for income plus growth.

While uncertainty remains in the short term, Pfizer’s combination of a reliable dividend, undervaluation relative to peers, and a promising pipeline suggests patient investors may be rewarded over a 5-year horizon.

Disclosure: I currently hold a position in Pifzer (NASDAQ: $PFE). This article reflects my personal opinions and analysis, and is not intended as financial advice. Please conduct your own research or consult a financial advisor before making any investment decisions.

Some quantitative models project a steep upward trajectory. One forecasting service estimates an average December 2025 price of $34.67, with a low of $32.18 and a high of $35.72—implying over 100% upside from current levels (StockScan). If investor sentiment catches up with this model, the stock could indeed flirt with $40 before year-end.

2. Financing Strength and Cash Position

As of March 31, 2025, Oscar Health reported a fortified balance sheet: $4.86 billion in cash, equivalents, and investments, up from $3.97 billion at the end of 2024. Total assets rose 21% YoY, while operating cash flow increased 38% (Michael Burry’s Insights). This cash cushion gives Oscar flexibility to invest in growth, navigate regulatory headwinds, and drive further value.

3. Strategic Expansion Through New Partnerships

Oscar’s deal with Hy-Vee to launch “Hy-Vee Health with Oscar” in Des Moines, covering about 400,000 employees in the individual marketplace starting Jan 1, 2026, signals a bold move into employer-backed coverage. The ICHRA model aims to save businesses 20–30% and deliver substantial cost-savings to employees-this could create significant scale and margin tailwinds (Benzinga).

4. Accelerating Revenue Growth

While Q2 revenue of $2.86 billion fell slightly short of the $2.91 billion estimate, it still marked a 29% increase YoY. The company reaffirmed its full-year 2025 revenue guidance at $12–12.2 billion (versus Wall Street’s $11.32 billion estimate), underscoring underlying growth momentum (BenzingaYahoo FinanceStockAnalysis).

5. Valuation Appears Undervalued for Growth Potential

Oscar trades at over 101x forward EV/EBITDA, a lofty multiple—but some analysts argue this valuation is justified by its “quality characteristics” and disruptive business model (StockStory). Others see it as deeply undervalued despite near-term uncertainty tied to ACA policy risks (Seeking Alpha+1).

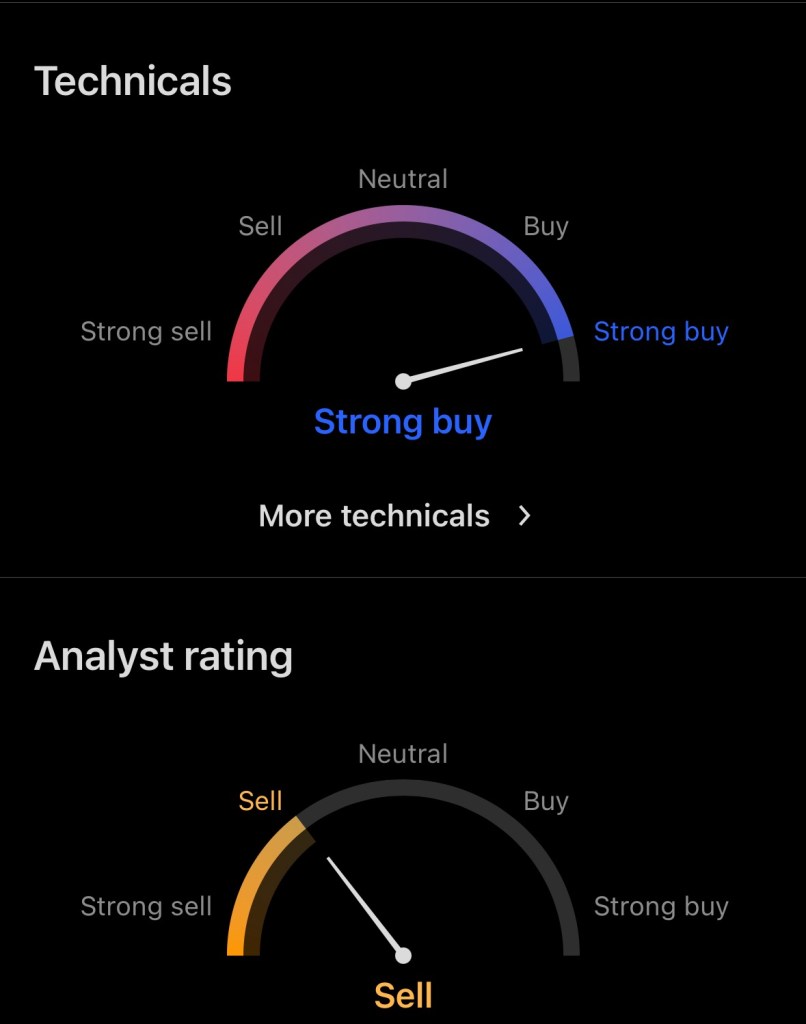

Skeptical Market Sentiment: Many brokerages hold “Sell,” “Hold,” or “Neutral” ratings. Notably, Piper Sandler cut its target from $14 to $13, citing uncertainties around risk adjustments and path to profitability (Benzinga). MarketBeat’s consensus is “Strong Sell,” and TipRanks flags a “Downside potential” of ~30% (MarketBeat).

Profitability Still Out of Reach in 2025: OSCR is expected to operate at a loss—losses projected around $200–300 million for the year (Yahoo Finance). Its Q2 GAAP loss was $0.89/share, and medical loss ratio (MLR) swelled from 79% in 2024 to 91.1% in Q2 2025 (BenzingaStockAnalysis). These factors dampen bullish expectations.

Headlines-Style Article: “Oscar Health: Can It Make the Leap to $40 by Christmas 2025?”

New York, August 23, 2025 – Oscar Health Inc. (NYSE: OSCR) currently trades near $16.98, buoyed by stellar revenue growth, robust liquidity, and a landmark new partnership but Wall Street’s confidence remains tepid.

Why $40 isn’t implausible:

Long-term algorithmic forecasts place December 2025 prices in the low-$30s, including a possible high of $35.72 (StockScan).

Strengthened cash position of $4.86 billion, coupled with rising operating cash flows, enhances the company’s financial flexibility (Michael Burry’s Insights).

Innovative ventures like the Hy-Vee collaboration, targeting 400,000 employees, position Oscar to disrupt cost structures and tap new revenue streams (Benzinga).

A confirmed revenue guidance of $12–12.2 billion highlights strong underlying demand despite macro-healthcare headwinds (Yahoo FinanceStockAnalysis).

Profitability is still elusive: projected operational losses of up to $300 million in 2025, and increased medical loss ratios (MLR) eroding margins (BenzingaYahoo FinanceStockAnalysis).

Sentiment skews negative, with ratings from “Hold” to “Strong Sell” prevailing, reflecting elevated policy-related and insurance-market risks (MarketBeat).

Final Thoughts: While consensus targets place Oscar Health under $15, a confluence of strong cash reserves, growth initiatives, and bullish long-term models could propel the stock into the low $30s by Christmas-though doing so would require sustained execution and favorable market sentiment in the face of continued near-term challenges.

Disclaimer: The author holds a position in $OSCR Oscar Healthcare and this article should not be considered financial advice. Always conduct your own research before making any investment decisions.

Airbnb delivered $11.1 billion in revenue for 2024, marking a 12% year-over-year increase, driven by higher booking volume and sustained average daily rates. Gross booking value surged to $81.8 billion (+10.6% YoY), while free cash flow hit $458 million in Q4 (18% margin) (AInvest).

Moreover, Airbnb’s global market share in short-term rentals climbed to 44% in 2024, up from 28% in 2019—far ahead of Booking.com (18%) and Expedia/Vrbo (9%) (AInvest).

2. Efficient Asset-Light Business Model

Airbnb’s strategy avoids owning properties, enabling high-margin operations. Their gross margin soared to approximately 83% in early 2024 (The Motley Fool), and their asset utilization metrics demonstrate tightening efficiency. Notably, the net fixed-asset turnover leaped from 12.5 in 2020 to 75.5 in 2024, reflecting strong revenue delivery with minimal asset base (Stock Analysis on Net).

3. Strategic Diversification into Services & Experiences

In recent quarters, Airbnb has repositioned itself beyond homestays into an integrated travel ecosystem-offering localized experiences, services like spa treatments, personal training, and lodging alternatives-all within its revamped app ecosystem (AInvestMarketWatch).

This diversification is not trivial: management projects that the “Services & Experiences” vertical could generate $1 billion in annual revenue within 3–5 years, backed by a $200–250 million investment earmarked for 2025 (AInvestMarketWatch).

4. Recent Strong Earnings Momentum

Airbnb outperformed expectations in Q2 2025:

Earnings per share: $1.03 (+99% YoY vs. $0.94 expected)

Revenue: $3.1 billion (+13% YoY)

Gross bookings: $23.5 billion (+11% YoY)

Despite these strong results, caution around margin trajectory and investment pace weighed on sentiment, causing a ~7% dip in premarket trading Investors.

Simultaneously, long-term confidence remains steady-Akre Capital boosted its Airbnb allocation by 10%, signaling belief in the company’s growth trajectory (AInvest).

5. Favorable Industry Trends

In the broader travel space, analysts remain positive. A recent Barron’s feature highlights secular travel growth outpacing GDP and the rising demand for experiences. Although other travel players like hotels and airlines benefit, OTAs and platforms like Airbnb must adapt and diversify to stay competitive-something Airbnb is actively doing (Barron’s).

Industry Positioning: How Airbnb Compares

Here’s a snapshot comparing Airbnb to its main competitors in the travel lodging and experiences sector:

Company

Market Share (2024)

Business Model

Key Differentiator

Airbnb

44%

Asset-light platform

Large host network, high margins, diversified services

Booking.com

18%

Hybrid (hotels + rentals)

Strong hotel partnerships, AI integration

Expedia/Vrbo

9%

Hybrid OTA

Bundle offerings, traditional OTA presence

Airbnb leads clearly in short-term rental share and continues to build stronger differentiation through vertical integration and digital enhancements (AInvest+1MarketWatchBarron’s).

Points of Caution

Valuation: Forward P/E sits above 30x (e.g., ~34.5x), relatively high compared to peers like Expedia (~10x) or Booking (~18x) (The Motley FooleToro).

Regulatory Headwinds: Local restrictions (e.g., New York City) and evolving laws could curtail growth in certain markets (eToroMarketWatch).

Execution Risk: Scaling new offerings and achieving the $1 billion services target will take time—short-term margins may remain under pressure (AInvestInvestorsMarketWatch).

Final Take

Airbnb demonstrates the hallmarks of a high-upside, long-term growth stock:

Strong financials, efficient operations, and leading share in a growing market.

Expanding revenue streams beyond traditional listings.

Strategic execution evidenced by earnings beats and fund manager conviction.

That said, elevated valuation and near-term execution risks suggest that patient investors may benefit from disciplined entry points or staged allocation.

Disclaimer: The author holds a position in $ABNB AIR BNB and this article should not be considered financial advice. Always conduct your own research before making any investment decisions.

Apple remains a compelling long-term investment, thanks to its robust ecosystem, accelerating AI strategy, and disciplined capital returns.

🏛️ Reliable Business Model & Ecosystem Moat

Apple now supports over 2.3 billion active devices, forming one of the most durable customer ecosystems in tech. This massive footprint reinforces high switching costs and recurring revenue streams via services like the App Store, Apple Pay, and suite of subscriptions (now over 38% of gross profit) (Forbes). Its strategy of integrating hardware, software, and services creates a differentiation moat that’s hard to replicate.

🚀 Catalysts Behind Future Growth

▪ Apple Intelligence: A Privacy-First AI Pivot

At WWDC 2025, Apple unveiled its “Apple Intelligence” initiative—20+ AI-powered features like real-time translation and email summarization designed for on-device performance and privacy. A major upgrade to Siri is expected in 2026. While it’s lagging peers in sheer AI spend, Apple is now investing aggressively and open to strategic M&A, having acquired at least seven AI startups in 2025..

▪ iPhone Refresh Cycles & Hardware Upside

Morgan Stanley projects a 12% rebound in iPhone shipments by fiscal 2026 as AI features boost upgrade demand. The favorable reception to new iPhone 16 models ahead of the holiday season supports this optimistic view (marketwatch.com).

🌍 Strategic Resilience Amid Geopolitical Risks

Apple’s architecture strategy includes over $500 billion in U.S. investment over four years—from expanding chip-making capacity to creating manufacturing academies and AI server production facilities to help offset tariff risks. At the same time, it has shifted much iPhone production for U.S. markets to India, diversifying supply chain risk away from China.

💰 Financial Strength & Shareholder Returns

Apple posted $94 billion in Q3 2025 revenue—a 10% year-over-year gain—and services revenue reached a record $27.4 billion. EPS came in above expectations, and despite $800 million+ in tariff impacts, Apple demonstrated operational resilience.

It continues to return capital aggressively, with $15.2 billion paid in dividends in 2025 and a long-term track record of dividend increases and share repurchases. Analysts expect this capital discipline to endure, offering downside protection and steady income (The Motley FoolForbes).

📉 Valuation: Discount with Upside Potential

Despite its strengths, Apple is currently down roughly 20% year-to-date, underperforming other major tech names amid tariff fears, AI lags, and macro uncertainty (Business Insider). Its forward P/E sits at around 33.6×, above the S&P 500 average (~23×), making valuation relative to its growth prospects a mixed story (Forbes). Still, analysts at BofA, Goldman Sachs, Wedbush, and others issue “Buy” ratings with 12–18 month targets of $235–300, implying double-digit upside from today’s ~$200 price levels.

🧭 Risks to Watch

While Apple’s fundamentals remain solid, investors should monitor:

Delays or execution risk in AI deployment or acquisitions

Regulatory scrutiny around antitrust, App Store rules, and global expansion

U.S.–China relations and implications for supply chain resilience

📈 Final Verdict: Long-Term Buy, Tactical Caution

Apple’s dominant ecosystem, balanced growth from hardware and high-margin services, disciplined capital returns, and accelerated AI pivot position it as a long-term winner. While near-term volatility and tariff uncertainty add caution, the current valuation discount provides an attractive entry point for investors with a multiyear horizon.

Disclosure:

I do not own any stock or have any financial interest in Apple Inc. (NYSE: AAPL). This article is for informational purposes only and should not be considered financial or investment advice. Investing in stocks carries risks, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

The boundaries between work and personal life have become increasingly blurred. Smartphones, laptops, and collaboration tools make it easier than ever to stay connected to work—sometimes too connected. While this digital connectivity has its advantages, it also presents new challenges to maintaining a healthy work-life balance.

The Double-Edged Sword of Connectivity Technology has transformed the modern workplace, enabling remote work, flexible schedules, and real-time collaboration across time zones. For many, this has opened up opportunities to balance personal responsibilities with professional demands more effectively. However, the same tools that provide freedom also tether employees to their jobs around the clock.

The expectation to be constantly available can lead to burnout, stress, and reduced productivity. Emails after dinner, Slack messages on weekends, and Zoom calls outside of regular hours can erode the boundary that once clearly separated work from life.

Understanding the Importance of Work-Life Balance Work-life balance isn’t just a trendy phrase; it’s a vital component of mental and physical health. Research shows that employees who maintain a healthy balance are more engaged, creative, and resilient. They also tend to have better relationships, sleep quality, and overall well-being.

Without balance, overworking can lead to anxiety, depression, and even serious health problems like cardiovascular disease. For employers, an imbalanced workforce can result in higher turnover rates, lower morale, and decreased performance.

Strategies for Achieving Balance

Set Clear Boundaries Create a defined start and end to your workday. Turn off work notifications during personal time and use tools like calendar blocking to separate work tasks from personal obligations.

Embrace Flexibility—Wisely Flexibility is a benefit, but it should serve you, not control you. Use flexible schedules to accommodate your life, but be cautious not to let work bleed into every free moment.

Prioritize and Delegate Focus on high-impact tasks and delegate where possible. Not every task needs your immediate attention or direct involvement. Learn to say “no” or “not right now” to non-essential demands.

Take Regular Breaks Stepping away from your screen helps reset your brain. Incorporate short breaks during the day and make time for longer stretches away from work, such as weekend unplugging or vacations.

Communicate Openly Whether you’re an employee or a leader, talk openly about work-life balance. Set realistic expectations and encourage a culture where taking personal time is respected.

Use Technology Intentionally Use digital tools to enhance, not hinder, balance. Apps that promote mindfulness, track screen time, or automate tasks can be powerful allies in managing digital overload.

The Role of Employers Employers have a crucial role in promoting work-life balance. Forward-thinking companies offer wellness programs, flexible work arrangements, and support systems for mental health. Encouraging regular time off, discouraging after-hours communications, and recognizing efforts to maintain balance can create a healthier work culture.

Balance Is a Moving Target In the digital age, achieving work-life balance isn’t about perfect symmetry—it’s about creating harmony between work and personal priorities. It requires intention, discipline, and adaptability. As technology continues to evolve, so too must our strategies for staying grounded. By being mindful of how we engage with digital tools and setting healthy boundaries, we can reclaim balance and build more fulfilling lives—both at work and at home.