When most homeowners think about their insurance policies, they focus on the obvious: fire, theft, storms, and liability. But there’s a lesser-known protection that can make or break your financial recovery after a disaster—Law and Ordinance Coverage, sometimes referred to as “Building Code Coverage.”

And in 2025, with stricter building codes nationwide and rising construction costs, this coverage has never been more important.

What Is Law & Ordinance Coverage?

Law and Ordinance coverage is a component of your homeowners insurance that helps cover the additional costs required to rebuild or repair your home according to current building codes after a covered loss.

Many homes—especially those built 10, 20, or 50 years ago—no longer meet today’s safety and construction standards. If a fire, storm, or other covered event damages your home, local regulations may require you to upgrade wiring, plumbing, insulation, roofing systems, or structural components.

Without Law & Ordinance coverage, those upgrades come straight out of your pocket.

Three Key Parts of Law & Ordinance Coverage

Most policies break this coverage into three categories:

1. Coverage A: Loss to the Undamaged Portion of the Home

If 40% of your home is destroyed but local law requires the entire house to be rebuilt to meet current code, this coverage pays for the undamaged portion.

2. Coverage B: Demolition Costs

Bringing a damaged structure down safely isn’t cheap. Demolition, debris removal, and hauling away materials can be surprisingly costly.

3. Coverage C: Increased Cost of Construction

This covers the code-required upgrades—such as new electrical systems, energy-efficient windows, reinforced roofing, or accessibility requirements—that weren’t part of your original home.

Why It Matters in 2025

✔️ Building Codes Change Constantly

Many communities have tightened codes after severe weather events, wildfires, and structural failures. Even small repairs often trigger mandatory upgrades.

✔️ Construction Costs Continue Rising

The price of materials and skilled labor remains elevated. Code upgrades can add tens of thousands of dollars to a reconstruction project.

✔️ Older Homes Are Especially at Risk

Homes built before 2000 often lack modern safety requirements, meaning mandatory upgrades are more likely after a partial loss.

✔️ It Can Protect Your Savings and Prevent Delays

Without Law & Ordinance coverage, homeowners often face unexpected out-of-pocket expenses that can stall rebuilding and extend displacement.

Real-World Example

A kitchen fire damages 30% of a 1980s home. The city requires:

New electrical wiring throughout the entire house

Upgraded insulation

A modern HVAC system with energy efficiency standards

Only the portion of the home physically damaged by fire is covered by standard insurance. All code-required upgrades to undamaged areas are not — unless you have Law & Ordinance coverage.

The homeowner could face up to $40,000–$75,000 in uncovered expenses.

How Much Coverage Should You Carry?

Insurers typically offer Law & Ordinance limits as a percentage of the dwelling amount, commonly:

10%

25%

50%

100% (offered in some states)

For older homes or areas with aggressive code enforcement, higher limits may provide critical protection.

A Small Coverage That Makes a Big Difference

You can’t control when disaster strikes, but you can protect yourself from the financial shock that comes with rebuilding to today’s standards. Law and Ordinance coverage ensures your home can be rebuilt safely—and legally—without draining your savings or delaying your recovery.

If you haven’t reviewed your homeowners policy lately, now is the time to check your limits and make sure this essential coverage is in place.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

In a world that moves faster every year, 2025 has become a year of reflection. People are revisiting past decisions—career moves, relationships, financial choices, lifestyle habits—with a clearer lens and a deeper understanding of consequence. The old saying “everything happens for a reason” has resurfaced from a previous post of mine, not as a cliché, but as a guidepost for navigating uncertainty and reconciliation in our lives.

A Shift Toward Reflective Living

Across the country, more Americans are reporting that they feel more intentional than they did a decade ago. According to several national surveys, individuals in their 30s, 40s, and 50s say they now view pivotal moments—good and bad—as necessary steps that shaped their current stability. This movement toward reflective living has become especially prominent after years of global disruptions and economic volatility.

“For many, 2025 is the year of understanding,” says life coach and behavioral specialist Dana Reeves. “People look back and realize that even the setbacks taught them something that ultimately pushed them forward.”

Learning From Past Decisions

The theme of “If I knew then what I know now” has been revisited in countless workplaces, retirement discussions, and financial planning meetings. Individuals who once regretted switching careers, making certain investments, or delaying big decisions are beginning to see those choices differently.

Many professionals say that hardships in earlier years helped them build resilience, leading to promotions, stronger relationships, and greater financial responsibility today. Some even credit prior failures for their current success.

Turning Regret Into Growth

Mental-health experts note that regrets are being reframed in 2025 as tools for personal evolution, not anchors that weigh us down.

“Regret is a powerful teacher,” explains psychologist Dr. Liana Mercer. “If we’re willing to study our past with compassion, we unlock the intelligence needed to make better choices moving forward.”

This mindset shift has led to an uptick in personal development programs, career retraining, and financial literacy courses. People want to apply what they’ve learned, not dwell on what they’ve lost.

Embracing Purpose Through Adversity

Challenges—job losses, health scares, failed relationships—are being viewed through a new lens: as catalysts. Individuals who experienced major disruptions in the early 2020s often say those moments forced them to slow down, reassess their priorities, and rebuild in healthier ways.

As one community leader put it, “Sometimes life has to fall apart a little so it can fall into place later.”

Why 2025 Feels Different

Unlike articles and discussions from previous years, the 2025 perspective is grounded in lived experience and hindsight. People aren’t just repeating the phrase “everything happens for a reason”—they’re proving it through the stability, insight, and resilience they’ve cultivated.

Retirees are expressing gratitude that earlier financial struggles taught them discipline. Families are appreciating the detours that led them to stronger bonds. Career professionals are recognizing that their long roads were necessary to build confidence and competence.

The Takeaway

Looking back is no longer about regret—it’s about recognition. Every difficult chapter, every unexpected turn, every leap of faith has contributed to where people stand today.

As we continue through 2025, the message is clear: We can’t rewrite the past—but we can honor it. And often, we discover that the past knew exactly what it was doing.

As more Americans approach retirement, many are finding that the path to a secure and fulfilling post-work life is more complex than they expected. While saving money is an important first step, a successful retirement hinges on avoiding common pitfalls that can derail even the most carefully built plans. Here are some of the most frequent retirement traps—and smarter strategies to consider instead.

Trap 1: Relying Too Heavily on Social Security

Many retirees assume Social Security will replace most of their income, only to discover their benefits cover far less than expected. With the average monthly benefit hovering around modest levels, relying on Social Security alone can put retirees at risk of falling behind rising costs of living and healthcare expenses.

A smarter alternative: Build a layered income plan that includes Social Security, retirement accounts like 401(k)s or IRAs, pensions (if available), and supplemental income sources. Consider part-time work or consulting if feasible. The key is diversifying your income streams so one isn’t carrying the entire load.

Trap 2: Underestimating Healthcare Costs

Healthcare is one of the biggest retirement expenses, and Medicare doesn’t cover everything. Many retirees are shocked by premiums, deductibles, dental costs, and long-term care needs.

A smarter alternative: Plan early. Look into long-term care insurance or hybrid life-insurance policies with LTC riders. Create a dedicated healthcare fund within your retirement savings. And don’t overlook supplemental Medicare plans that can greatly reduce out-of-pocket expenses.

Trap 3: Cashing Out Retirement Accounts Too Early

Taking large withdrawals early in retirement—especially before age 59½—can trigger steep taxes and penalties, diminishing your long-term nest egg. Even after that age, withdrawing too aggressively can make savings run out sooner than expected.

A smarter alternative: Use a structured withdrawal plan, such as the 4% rule or dynamic withdrawal strategies that adjust based on market performance. Pair withdrawals with tax-efficient strategies like Roth conversions before RMD age to reduce future tax burdens.

Trap 4: Failing to Account for Inflation

Inflation has made a fierce comeback in recent years. Retirees with fixed incomes or overly conservative portfolios risk losing purchasing power over time.

A smarter alternative: Include growth investments—like diversified stock funds—even in retirement, to stay ahead of inflation. Treasury Inflation-Protected Securities (TIPS) and annuities that offer inflation adjustments can also provide peace of mind.

Trap 5: Overlooking Housing Costs

Many retirees assume their housing expenses will drop once the mortgage is gone, but property taxes, insurance, and maintenance continue—and often increase.

A smarter alternative: Evaluate your housing situation realistically. Downsizing, relocating to a lower-cost area, or exploring 55+ communities may reduce expenses. Some retirees also use a portion of home equity strategically through downsizing or a Home Equity Conversion Mortgage (HECM) as part of their financial plan.

Trap 6: Not Preparing Emotionally for Retirement

Retirement isn’t just a financial transition—it’s a lifestyle change. Without structure, purpose, or social engagement, many retirees face loneliness, boredom, or even depression.

A smarter alternative: Design your retirement life as intentionally as your financial strategy. Volunteer, join clubs, take classes, or explore part-time work in a field you enjoy. Staying mentally and socially active is essential for long-term well-being.

Smart Alternatives for Soon-to-Be and Current Retirees

Beyond avoiding traps, here are simple, proactive steps that make retirement more stable and satisfying:

Create a retirement income roadmap that outlines exactly where your money will come from and how long it should last.

Meet with a financial professional to stress-test your plan against inflation, market downturns, and health surprises.

Diversify income, including predictable sources like annuities, rental income, dividends, or guaranteed pension payouts.

Stay flexible—your retirement plan should evolve as life, health, and markets change.

Review your insurance coverage, including life, home, auto, and long-term care, to ensure you’re protected.

Stay active and engaged, both socially and physically, to support overall happiness and health.

Long and Short

Retirement doesn’t have to be uncertain. By steering clear of common traps and embracing a well-rounded financial and lifestyle strategy, retirees can build a future that’s not only secure—but rewarding. With thoughtful planning and the right support, this next chapter can be the best one yet.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Cohen & Steers Infrastructure Fund, Inc. (ticker: UTF) is a closed-end fund that invests primarily in listed infrastructure companies utilities, pipelines, toll roads, telecoms and similar businesses with an emphasis on income and total return. The fund targets at least 80% exposure to infrastructure securities and is permitted to hold preferreds and fixed-income as well. (Cohen & Steers+1)

The case for UTF in a downturn

High and steady monthly distribution. UTF pays a monthly cash distribution (recently about $0.155 per share) that translates to a forward annualized dividend around the high-single to mid-single digits (roughly a 7–8% yield at current market prices). That regular payout can make UTF attractive to income-seeking investors during equity market weakness. (Cohen & Steers Resources+1)

Defensive underlying exposure. Infrastructure companies often provide essential services (power, water, roads, telecom) with relatively stable cash flows and regulatory protections that can soften downside in economic contractions compared with cyclical sectors. UTF’s strategy explicitly focuses on these companies and includes income-oriented holdings (common equity plus a portion in preferreds/fixed income). (SEC+1)

Closed-end structure can add opportunity. As a closed-end fund, UTF can trade at a premium or discount to net asset value (NAV) and use leverage or share repurchases to enhance returns. In downturns, discounts can widen and create potential buying opportunities for investors seeking yield and income—though discounts can also persist. Recent fund documents show management tools (repurchase programs, rights offerings) are in use when needed. (Cohen & Steers+1)

Relative price stability historically. While all market securities fall in tough selloffs, UTF’s share price history shows less extreme volatility than many small-cap or tech names because of its income focus and infrastructure holdings. (See sources below for historical price and distribution history.) (Yahoo Finance+1)

Total-return potential from dividends + capital. In a downturn the regular dividend cushions total returns. If the portfolio’s underlying cash flows remain intact, the dividend can provide an attractive yield while capital recoveries occur — particularly for buy-and-hold income investors.

Risks you must weigh

Discount/premium risk: CEFs can trade at large, persistent discounts to NAV; the market price might not reflect NAV recovery quickly. (CEF Connect)

Leverage and interest-rate sensitivity: Some closed-end funds use leverage that can magnify losses when markets fall and can increase sensitivity to rising rates. UTF’s prospectus and factsheet discuss leverage and fixed-income exposure. (Cohen & Steers Resources+1)

Concentration risk: Heavy exposure to infrastructure and related subsectors means sector-specific shocks (regulatory, energy shocks, etc.) can hit performance. (SEC)

Analysts don’t always publish a single consensus price target for closed-end funds like UTF; where a consensus target isn’t available, a scenario approach is often more informative. Below I created three plausible projected price scenarios for the next 12 months — Bear (–15% y), Baseline (+4% y) and Bull (+25% y) — starting from the recent market close (~$24.20). These are illustrative projections (not predictions or investment advice), intended to show how price paths and total return dynamics might look under different macro/backdrop outcomes.

Key assumptions used for the chart: start price $24.20, monthly compounding equivalent to the annual scenario rates listed above. These scenarios do not include dividends — they show market-price outcomes only (adding dividends would materially improve total returns, especially at a ~7–8% yield).

Quick takeaways

UTF’s monthly dividend and exposure to essential infrastructure make it a reasonable consideration for income-focused investors during market downturns; the dividend can provide cashflow support while equity markets recover. (Cohen & Steers Resources+1)

However, because UTF is a closed-end fund, price movements can diverge from underlying NAV and be influenced by fund-specific factors (discounts, leverage, corporate actions). That tradeoff (high yield vs. structural CEF risks) is central to whether UTF is appropriate for any individual portfolio. (Cohen & Steers+1)

Disclosure

I currently hold a position in the Cohen & Steers Infrastructure Fund (UTF). This information is provided for educational and informational purposes only and should not be considered financial advice. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

DividendMax. (n.d.). Cohen & Steers Infrastructure Fund dividend information. Retrieved from https://www.dividendmax.com/

SEC. (n.d.). Cohen & Steers Infrastructure Fund, Inc. (UTF) — Prospectus & filings. U.S. Securities and Exchange Commission. Retrieved from https://www.sec.gov/

StockAnalysis.com. (n.d.). UTF: Cohen & Steers Infrastructure Fund stock dividend & history. Retrieved from https://stockanalysis.com/

Yahoo Finance. (n.d.). UTF — Cohen & Steers Infrastructure Fund price & chart data. Retrieved from https://finance.yahoo.com/

When it comes to building wealth, most families focus on earning, saving, and investing. Yet one of the most overlooked parts of financial planning happens at the end of the journey: preparing the next generation to handle what’s left behind. Experts warn that simply passing down money—without communication or financial education—can lead to confusion, conflict, and costly mistakes.

A recent study by multiple wealth-management groups found that nearly 70% of inherited wealth is lost by the second generation, and 90% is gone by the third. The cause isn’t the financial markets—it’s a lack of preparation. When heirs are suddenly handed assets, properties, or cash with little context, they may mismanage the money, disagree with each other, or unintentionally make tax-heavy decisions.

Why Preparation Matters

Inheritance isn’t just about money—it’s about clarity and continuity. When families don’t talk about what’s being passed down, heirs often must make high-pressure decisions during periods of grief. Without a roadmap, even well-intentioned children or beneficiaries may disagree on how to handle a home, manage investments, or split proceeds.

And the stakes are rising. As Baby Boomers pass on an estimated $84 trillion over the next two decades, families who fail to prepare run the risk of watching generational wealth disappear.

Communication Is the First Step

Open dialogue ensures everyone understands what exists, where it is, who gets what, and—equally important—why. These conversations take the mystery out of money and help heirs feel responsible, not overwhelmed.

Good communication also reduces legal challenges, sibling tension, and last-minute surprises. Beneficiaries who know the plan ahead of time make smarter choices because they’re not operating in the dark.

Teach Financial Know-How Before It’s Needed

Even the best inheritance plan can fall apart if heirs don’t know how to manage money. Families should consider sharing basic financial skills: how taxes on inheritance work, the risks of cashing out investments too quickly, how to evaluate insurance needs, and how to make a long-term plan.

Working with a financial advisor, estate attorney, or tax professional can also give heirs a clear framework to manage their new responsibilities confidently.

Table: Smart Ways to Pass Down Inheritance

Method

What It Is

Best Use Case

Key Benefits

Potential Pitfalls

Will

Legal document stating who receives assets

Straightforward asset distribution

Simple, inexpensive, widely recognized

Can go through probate; may be challenged

Revocable Living Trust

A trust you control during your lifetime

Avoiding probate and ensuring smooth transfer

Faster distribution, more privacy, flexible

Requires proper funding; setup cost

Beneficiary Designations

Named beneficiaries on accounts (401k, life insurance, IRAs)

Retirement and insurance assets

Bypasses probate, easy to update

Conflicts with wills if not aligned

Gifting During Lifetime

Giving money or assets while alive

Reducing estate taxes; preparing heirs early

Lets heirs learn with guidance; tax advantages

Annual gift limits; may impact your retirement

Family Meetings

Regular discussions about assets and plans

Multi-heir families; complex estates

Reduces conflict, sets expectations

Requires openness; emotional topics

Financial Education for Heirs

Teaching heirs money skills before they inherit

Any family wanting generational wealth

Builds confidence and reduces mistakes

Time investment; requires ongoing support

Insurance Policies

Using life insurance to create liquidity

When heirs need cash to pay taxes or debts

Predictable payout; avoids asset liquidation

Premium costs; needs proper planning

Professional Advisors

Attorneys, financial planners, tax pros

Significant or complex estates

Expert guidance, reduced errors

Costs vary; choose reputable advisors

To Sum Up

In the end, passing down wealth isn’t just about assets—it’s about equipping the next generation to use those assets wisely. By communicating openly, planning thoughtfully, and preparing heirs with real financial understanding, families can protect their legacy and ensure their hard work continues to make a positive impact for years to come.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

In every great performance—whether it’s a championship-winning team, a thriving business, or a band in perfect harmony—there’s one thing in common: teamwork that works. But the secret isn’t just being on the same team. It’s about choosing to work as one.

The phrase “one band, one sound” captures this idea perfectly. Originating from the world of marching bands, it means every individual must give their best for the collective good. When one person falls out of sync, the entire performance suffers. But when everyone aligns with a shared goal, the results can be extraordinary.

The Power of Intentional Collaboration

True teamwork doesn’t happen by accident—it’s intentional. It requires trust, open communication, and a willingness to check egos at the door. Each member brings their own rhythm, but success comes from listening and adjusting to others. This is as true in the workplace as it is on the field or stage.

The Benefits of Working as One

When teamwork clicks, productivity soars. Studies show that teams built on mutual respect and collaboration are not only more innovative but also more resilient under pressure. Members feel valued, motivated, and supported, creating a positive feedback loop that lifts everyone higher.

Making It Work in Real Life

To build that “one band, one sound” culture, leaders and teammates alike must commit to:

Clear communication: Everyone knows their role and what success looks like.

Shared purpose: Each person understands how their contribution fits into the bigger picture.

Accountability: Individuals own their performance but remain loyal to the team’s mission.

Celebration of wins: Recognizing collective achievement strengthens unity and morale.

The Final Note

Teamwork really works—if you want it to. It’s not just about showing up; it’s about showing up for each other. When people align their goals, respect each other’s strengths, and perform with unity of purpose, the result is harmony in motion.

After all, in life as in music, the best sound comes when everyone plays their part—together.

Life is full of transitions—whether it’s buying your first home, changing careers, starting a family, or preparing for retirement. While these moments bring opportunity and excitement, they can also create uncertainty and stress. The good news: with proactive planning and professional guidance, individuals can navigate these turning points with greater confidence and clarity.

“Transitions can feel overwhelming because they often involve financial, emotional, and lifestyle changes all at once,” says certified financial planner Jenna Morales. “Having a plan and a professional partner to guide you helps you make informed decisions rather than emotional ones.”

The Power of Planning Ahead

Proactive planning means thinking ahead—mapping out potential outcomes and creating strategies that align with your long-term goals. It’s not about predicting the future but preparing for it. Whether you’re moving to a new city, managing an inheritance, or downsizing in retirement, foresight helps reduce risk and stress.

Professional advisors, from financial planners to insurance agents and career coaches, can offer valuable expertise to help identify blind spots and opportunities. They can also act as objective voices when emotions run high, ensuring you stay focused on your priorities.

Top Tips for Navigating Major Life Transitions

Start Early: Begin planning before the change happens. The earlier you prepare, the more control you’ll have over your options.

Clarify Your Goals: Define what success looks like for you—financially, emotionally, and personally.

Seek Professional Advice: Don’t go it alone. Certified experts can provide insights and structure your plan for maximum benefit.

Review Your Insurance and Finances: Major changes often affect your coverage needs and cash flow. Make sure your policies and budget reflect your new circumstances.

Build a Safety Net: Set aside emergency savings to cushion unexpected costs during transitions.

Stay Organized: Keep key documents—such as wills, policies, and financial records—accessible and updated.

Adjust as You Go: Life plans are not one-size-fits-all. Revisit and revise your strategy regularly as your needs evolve.

Focus on Mental Well-Being: Change can be stressful. Prioritize self-care and seek support when needed.

Moving Forward with Confidence

While no one can avoid life’s major transitions, being proactive and seeking professional guidance can transform uncertainty into opportunity. It’s about taking control of what you can—and having trusted experts help you navigate what you can’t.

“Confidence comes from preparation,” Morales adds. “When you plan ahead and surround yourself with knowledgeable support, you move forward not with fear—but with clarity.”

As we approach the end of 2025, the property insurance marketplace is navigating a mix of change, challenge and opportunity. Here’s a look at the key trends shaping the sector — and what they might mean for insurers, brokers and property owners alike.

1. Climate-Driven Losses Are Now the New Normal

The pace and severity of natural catastrophes continue to place major pressure on the property insurance market. The Swiss Re Institute estimates that global insured losses from natural catastrophes hit roughly US $80 billion in the first half of 2025, nearly double the 10-year average. (Reuters+2Insurance Journal+2) For insurers, that means heavier claims, tougher underwriting decisions and heightened scrutiny of exposures in high-risk zones.

What to watch:

Insurers will increasingly pull back or raise rates in high-catastrophe zones — e.g., coastal and wildfire-prone areas.

Property owners in those zones will receive stronger signals to invest in resilience (storm hardening, wildfire mitigation, flood defence).

Coverage gaps may grow where private insurers no longer provide adequate support, leading to more reliance on state/last-resort markets.

2. Pricing and Coverage Conditions Are Mixed — Softening in Some Segments, Hardening in Others

While recent years were characterised by sharp rate increases and tightening terms, there are signs that some parts of the market are stabilising or even softening. For example:

The Alera Group in its 2025 P&C update notes greater market stability, with disciplined underwriting, improving investment yields, and signs that premium growth may moderate. (Alera Group)

In commercial property, accounts with favourable loss history and limited catastrophe exposure may now see flat to single-digit rate increases, rather than the double-digit hikes of earlier years. (Dominion Risk+1)

On the flip side, in the homeowners/home-insurance space, average premiums remain elevated, and the insurers’ “combined ratio” suggests limited profitability in some segments. (Rate)

Key take-aways:

For well-performing risks, carriers are competing — more capacity, more flexible terms.

Brokers and agents who can help clients demonstrate strong mitigation/maintenance will be in demand.

3. Technology & Risk-Modelling Innovations Are Moving From “Nice to Have” to “Must-Have”

Insurers are rapidly expanding their use of technology — sensors, drones, satellite imagery, IoT monitoring, artificial intelligence — to refine risk assessments, improve underwriting and streamline claims. According to a recent legal-firm insight, insurers are deploying drones, satellite-imagery and IoT to track damage and property condition in real time. (Greenberg Traurig) Meanwhile, homeowners are seeing insurers push risk-mitigation incentives (smart-home sensors, leak detectors, fire-resistant construction) as a way to differentiate risk. (Rate)

What this means:

Risk-differentiation will widen: properties with upgraded resilience features may enjoy better terms/discounts.

Older or non-mitigated properties may face fewer options or harsher terms.

Agents and insurers who embrace these tools will have a competitive edge, especially in emerging hazard-zones.

4. Reinsurance and Capacity Pressures Remain Real

While direct insurance pricing may be moderating for some risks, the broader ecosystem — especially reinsurance — remains under strain. The costs of reinsurance for catastrophe risk continue to climb as global natural hazard exposures grow. (Greenberg Traurig) Also, some last-resort markets (state-backed, residual lines) are under pressure to raise rates or adjust eligibility, particularly in states with chronic exposure. (San Francisco Chronicle)

Implication: Insurers must manage their reinsurance treaties carefully, be selective about exposures they carry, and pass through appropriate pricing and terms to stay sustainable.

5. Market Size is Growing — With Geographic and Product Gaps Emerging

From a volume perspective, the property-insurance market remains on a growth path. For example, in North America the market for property insurance was projected to reach about US $365 billion in 2025, with a five-to-seven-year compound annual growth rate (CAGR) of nearly 7%. (Statista) Globally, a report projects the property-insurance market to be around US $364.75 billion in 2025, growing toward ~US$591 billion by 2034. (Business Research Insights)

Yet, growth is uneven:

Regions with escalating risk (wildfire, flood, storm) may struggle with supply and affordability.

Specialized products (wildfire-only, flood-only, resiliency add-ons) are gaining traction.

Bundled products (home + auto) and value-added services (risk-engineering, smart-home upgrades) are becoming differentiators.

6. Homeowners Face Increasing Burden — Affordability, Availability and Risk

For homeowners, especially in climate-exposed states (e.g., coastal Florida, wildfire-prone California), the challenges are mounting:

Rising premiums and deductibles: some reports show average home-insurance premiums nationally up ~20 % year-over-year in certain markets. (Rate+1)

Higher deductibles and more peril-specific deductibles (wind/hail, wildfire, flood) are becoming more common. (Matic Insurance)

Coverage availability is still strained in many high-risk ZIP codes; the E&S (Excess & Surplus) market is filling gaps. (Matic Insurance)

For agents and homeowners:

Risk mitigation (roof upgrades, fire-resistant landscaping, flood mitigation) is no longer optional—it can materially affect access and cost of coverage.

The choice of market (traditional carrier vs. surplus market) matters more than ever; early renewal/placement is advised.

For homeowners in highly exposed zones, budgeting for rising insurance costs (and potential policy non-renewals) is prudent.

7. Regulatory & Geographic Regulation Shifts

Regulators in states like Hawaii, Florida and California are responding to the stability challenges in property-insurance markets. For example, in Hawaii legislators pledged efforts to stabilise the market in the face of rising rates and insurers pulling out. (AP News) Rate filings and underwriting criteria adjustments are happening in several jurisdictions — meaning agents must stay abreast of local regulatory changes that could affect availability, coverage form, or premium.

Looking Ahead to Late 2025 and Early 2026

As we close out 2025, a few strategic themes for stakeholders:

For insurers and brokers: Market segmentation will deepen. Strong, well-mitigated risks will benefit from capacity and competition. Weakly mitigated risks will face greater terms and possibly coverage erosion.

For homeowners/property owners: Now is a contact point: review your property’s risk profile, invest in mitigation where possible, explore multiple carriers, and monitor renewal dates early.

For agents in your position (auto/property insurance): There’s an opportunity to advise clients on the “property side” in addition to auto — helping them understand risk exposures, mitigation, bundling opportunities, and market shifts. For example, bundling home + auto may give you more leverage.

For regulatory watchers: The interplay of climate risk, insurance affordability, and public policy will remain front-and-centre. Watch for state-level reforms, changes in last-resort insurers, and potential new coverage mandates or premium subsidies.

What Lies Ahead

The property-insurance market at the end of 2025 is in a state of transition. Big picture: demand is growing, but risk is mounting and not evenly distributed. Pricing and terms are moderating in some segments — yet for high-exposure zones the pressure remains acute. Technology, mitigation and geographic nuance will distinguish winners from laggards.

For you (and your clients) this means: be proactive. Know the risks. Position properties (or clients’ homes) for reward (through mitigation) rather than punishment. And stay flexible — the “next renewal” is likely to look quite different from the last.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

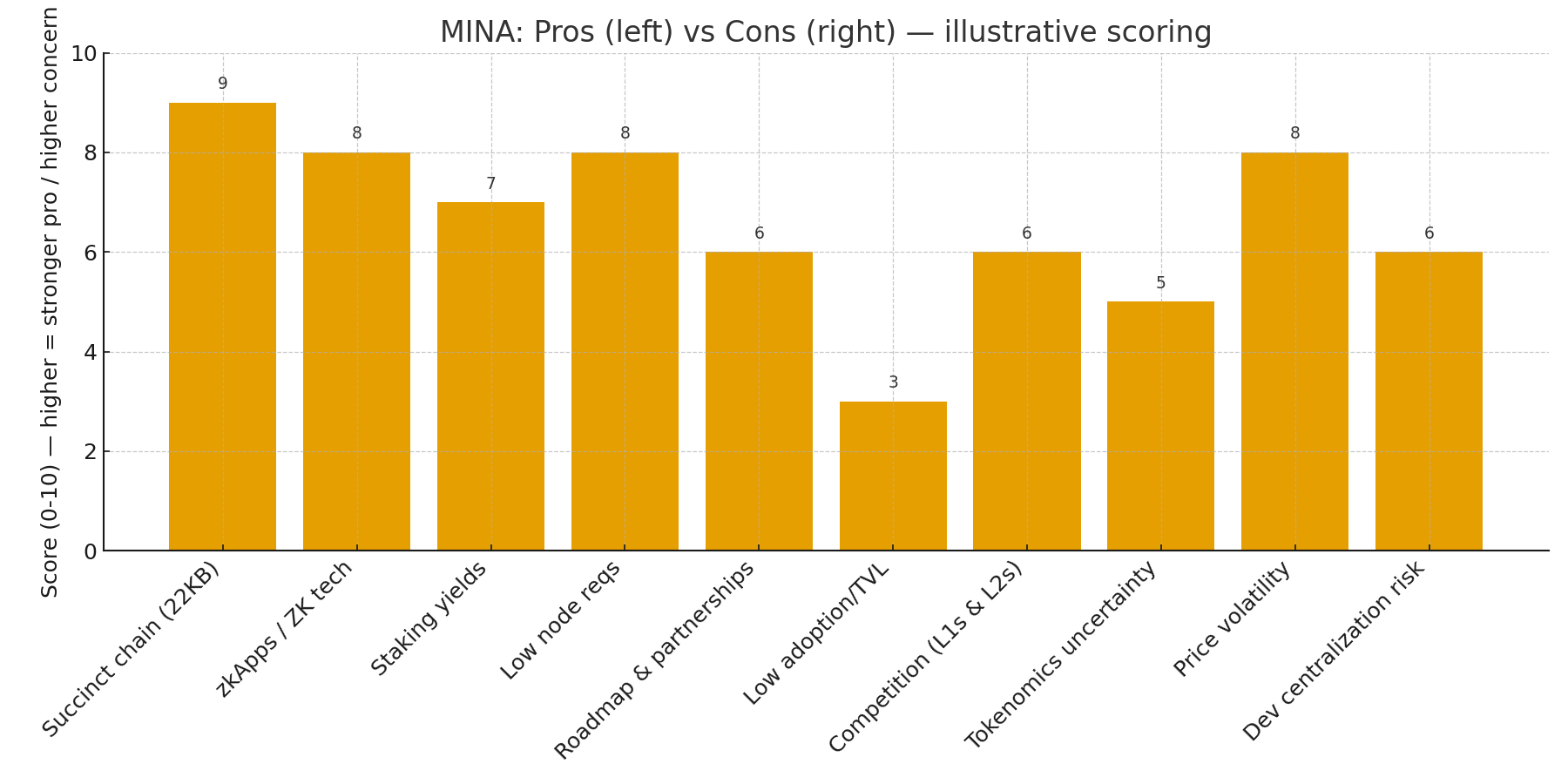

Mina Protocol markets itself as the “lightest blockchain” — a layer-1 that stays tiny by using recursive zero-knowledge proofs (zk-SNARKs) so the entire chain remains a succinct ~22KB snapshot instead of a growing ledger. That design promises a blockchain any device can verify, lowering node requirements and enabling on-device privacy-aware dApps (zkApps). Those technical foundations are Mina’s headline differentiator and the core reason some investors treat MINA as a long-term hold. (Mina Protocol+1)

Where MINA stands right now

As of early November 2025, MINA trades in the low-to-mid $0.17–$0.19 range with a market cap in the low hundreds of millions of dollars and roughly 1.26 billion MINA circulating. Price and ranking vary by source and exchange, but major market trackers show MINA as a mid-to-low market-cap altcoin. (CoinMarketCap+1)

Why investors like MINA — the bullish case

Truly lightweight chain: Mina’s constant-sized blockchain (~22KB) lowers the hardware and bandwidth needed to run a full node, which could help decentralize participation and boost mobile/edge use cases. This is fundamental to Mina’s pitch as a “blockchain for everyone.” (Nansen Research+1)

Zero-knowledge programmability (zkApps): Mina’s zkApp framework enables privacy-preserving smart contracts and verifiable off-chain computation. If ZK tech becomes central to mainstream Web3 privacy and scaling, Mina could capture unique developer interest. (Mina Protocol)

Staking yields / network rewards: MINA supports staking and many exchanges and platforms offer competitive staking APRs (examples reporting 6–12% or higher on various platforms), which attracts yield-seeking holders who prefer passive income while they wait for price appreciation. (Kraken+1)

Active roadmap and ecosystem work: Core development groups and community initiatives continue evolving Mina (roadmaps and upgrades in 2024–25 aim at tooling, zk developer onboarding, and greater interoperability). Continued protocol development can improve utility and adoption. (Mina Protocol+1)

Relatively small market cap = upside if narrative wins: Compared with top L1s, Mina’s market cap is modest, so positive adoption or a crypto risk-on rotation could produce outsized percentage gains (classic “small-cap upside” dynamic).

Risks and why caution is warranted

Adoption & TVL remain low vs major L1s: For MINA to move materially higher, it needs more apps, users, and locked value. Today it’s still a niche stack versus giants like Ethereum, Solana, or new ZK-focused rivals. Low TVL limits organic utility demand for the token. (CoinGecko+1)

Strong competition: Other projects are pursuing ZK tech, rollups, and lightweight verification. If larger ecosystems integrate similar ZK capabilities (or if Ethereum rollups dominate the ZK narrative), Mina’s unique edge could shrink. (o1Labs)

Tokenomics & supply dynamics: A large circulating supply (~1.26B MINA) and ongoing issuance/staking rewards can dilute price upside unless demand grows to absorb supply. Coin trackers list circulating supply but no fixed “max” supply, so inflation mechanics matter to holders. (CoinMarketCap)

Price volatility & market risk: As a mid/low-cap crypto, MINA is susceptible to broad market moves, liquidity shocks, and volatility — factors that can erase gains quickly. Historical price charts show sharp swings that should caution risk-sensitive investors. (Yahoo Finance)

Technology / centralization risk: While Mina’s research teams (o1 Labs, Mina Foundation, community contributors) are active, concentrated development or coordination risks exist — and any delays or setbacks to roadmap items could temper market enthusiasm. (o1Labs)

Potential upside in an “altcoin season”

Altcoin seasons reward narratives — smaller caps with clear, differentiated value propositions often run hardest. Mina’s narrative (real ZK programmability + tiny chain size) fits a neat theme: privacy, edge verification, and on-device dApps. If the ZK narrative accelerates — through developer tool improvements, interoperability wins (projects like Aligned working on ZK verification integrations), or a wave of zkApps adoption — MINA could outpace larger, less nimble chains. Several mid-2024–25 developments and roadmap items indicate the team remains focused on ZK tooling and ecosystem funding, which would be the necessary fuel for such a move. (o1Labs+1)

How an investor might position (not financial advice)

Long-term speculative hold: If you believe ZK tech and ultra-light clients matter, a small allocation to MINA (size depending on risk tolerance) could be reasonable — especially if you stake to capture yield while waiting for adoption. (Kraken)

Event-driven trade: Watch roadmap milestones, zkApp launches, partnerships (e.g., Aligned/Ecosystem announcements), and listings/staking product rollouts. Positive, repeated dev activity and growing on-chain usage are bullish triggers. (Mina Protocol+1)

Risk management: Given volatility and competition, position sizing, stop levels, and a clear thesis (what adoption metric would make you add more vs cut losses) are essential.

End Result

Mina’s technology is interesting and differentiated: a truly succinct chain with ZK programmability that theoretically lowers barriers to running full nodes and enables privacy-preserving dApps. That technical moat gives MINA a plausible role in a future Web3 where ZK proofs are central. However, adoption, TVL, competition, tokenomics, and market volatility remain the main hurdles. For investors, MINA looks like a classic higher-risk, higher-optional-upside altcoin: attractive to those who believe in ZK-native dApps and willing to stomach swings; less attractive to conservative crypto investors who prefer larger, more established L1 ecosystems. (Mina Protocol+2CoinMarketCap+2)

Disclaimer

I currently hold a position in MINA. The views and opinions expressed in this article are my own and are provided for informational purposes only. This content should not be construed as financial, investment, or trading advice. Always conduct your own research or consult with a licensed financial advisor before making investment decisions.

As daylight fades and drivers take to the roads after sunset, the risks rise dramatically. According to the National Safety Council, the fatal crash rate at night is about three times higher than during the day. Despite making up only a small portion of total driving time, nighttime driving accounts for nearly 50% of all traffic deaths in the United States each year.

Experts point to one primary reason: reduced visibility. Even with streetlights and modern vehicle technology, the human eye struggles in low-light conditions. But what many drivers don’t realize is how much their own vehicle’s headlights can contribute to the danger.

Over time, headlight lenses become cloudy or yellowed from oxidation, cutting light output by as much as 50%. Bulbs can also dim gradually, often without the driver noticing, and misaligned headlights may shine too low or too high, limiting visibility or blinding oncoming traffic.

“Headlights are your first line of defense at night,” says a local automotive safety technician. “Keeping them clean, bright, and properly aimed can make the difference between spotting a hazard in time or not at all.”

Regular maintenance—such as cleaning lenses, checking bulb brightness, and ensuring correct alignment—can dramatically improve safety. Replacing bulbs in pairs and restoring headlight covers can also restore lost visibility and reduce glare for others.

Drivers should also be mindful of when they’re on the road. Statistics show that the hours after midnight are the most dangerous, as fatigue, alcohol impairment, and reduced alertness peak. For the safest travel, experts recommend getting home before midnight whenever possible.

In short, maintaining your headlights isn’t just about looks—it’s about safety. As nights grow longer, take a few minutes to check your car’s lights. It could be one of the simplest ways to protect yourself and everyone else on the road.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.