I am a very strong man who is also a proud parent (my son is my world) something that you do not find too often (sort of like those people lucky enough to earn a Doctoral Degree). I love competitive sports "March Madness," as I believe they help foster competition in the workplace. I am continually looking for new challenges and hold myself accountable for all my actions at home and in the workplace. I love to talk (who in sales doesn't), read & conduct research. Finally, through various work and educational experiences I hope someday to become an established & full-time writer.

When it comes to building wealth, most families focus on earning, saving, and investing. Yet one of the most overlooked parts of financial planning happens at the end of the journey: preparing the next generation to handle what’s left behind. Experts warn that simply passing down money—without communication or financial education—can lead to confusion, conflict, and costly mistakes.

A recent study by multiple wealth-management groups found that nearly 70% of inherited wealth is lost by the second generation, and 90% is gone by the third. The cause isn’t the financial markets—it’s a lack of preparation. When heirs are suddenly handed assets, properties, or cash with little context, they may mismanage the money, disagree with each other, or unintentionally make tax-heavy decisions.

Why Preparation Matters

Inheritance isn’t just about money—it’s about clarity and continuity. When families don’t talk about what’s being passed down, heirs often must make high-pressure decisions during periods of grief. Without a roadmap, even well-intentioned children or beneficiaries may disagree on how to handle a home, manage investments, or split proceeds.

And the stakes are rising. As Baby Boomers pass on an estimated $84 trillion over the next two decades, families who fail to prepare run the risk of watching generational wealth disappear.

Communication Is the First Step

Open dialogue ensures everyone understands what exists, where it is, who gets what, and—equally important—why. These conversations take the mystery out of money and help heirs feel responsible, not overwhelmed.

Good communication also reduces legal challenges, sibling tension, and last-minute surprises. Beneficiaries who know the plan ahead of time make smarter choices because they’re not operating in the dark.

Teach Financial Know-How Before It’s Needed

Even the best inheritance plan can fall apart if heirs don’t know how to manage money. Families should consider sharing basic financial skills: how taxes on inheritance work, the risks of cashing out investments too quickly, how to evaluate insurance needs, and how to make a long-term plan.

Working with a financial advisor, estate attorney, or tax professional can also give heirs a clear framework to manage their new responsibilities confidently.

Table: Smart Ways to Pass Down Inheritance

Method

What It Is

Best Use Case

Key Benefits

Potential Pitfalls

Will

Legal document stating who receives assets

Straightforward asset distribution

Simple, inexpensive, widely recognized

Can go through probate; may be challenged

Revocable Living Trust

A trust you control during your lifetime

Avoiding probate and ensuring smooth transfer

Faster distribution, more privacy, flexible

Requires proper funding; setup cost

Beneficiary Designations

Named beneficiaries on accounts (401k, life insurance, IRAs)

Retirement and insurance assets

Bypasses probate, easy to update

Conflicts with wills if not aligned

Gifting During Lifetime

Giving money or assets while alive

Reducing estate taxes; preparing heirs early

Lets heirs learn with guidance; tax advantages

Annual gift limits; may impact your retirement

Family Meetings

Regular discussions about assets and plans

Multi-heir families; complex estates

Reduces conflict, sets expectations

Requires openness; emotional topics

Financial Education for Heirs

Teaching heirs money skills before they inherit

Any family wanting generational wealth

Builds confidence and reduces mistakes

Time investment; requires ongoing support

Insurance Policies

Using life insurance to create liquidity

When heirs need cash to pay taxes or debts

Predictable payout; avoids asset liquidation

Premium costs; needs proper planning

Professional Advisors

Attorneys, financial planners, tax pros

Significant or complex estates

Expert guidance, reduced errors

Costs vary; choose reputable advisors

To Sum Up

In the end, passing down wealth isn’t just about assets—it’s about equipping the next generation to use those assets wisely. By communicating openly, planning thoughtfully, and preparing heirs with real financial understanding, families can protect their legacy and ensure their hard work continues to make a positive impact for years to come.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

In every great performance—whether it’s a championship-winning team, a thriving business, or a band in perfect harmony—there’s one thing in common: teamwork that works. But the secret isn’t just being on the same team. It’s about choosing to work as one.

The phrase “one band, one sound” captures this idea perfectly. Originating from the world of marching bands, it means every individual must give their best for the collective good. When one person falls out of sync, the entire performance suffers. But when everyone aligns with a shared goal, the results can be extraordinary.

The Power of Intentional Collaboration

True teamwork doesn’t happen by accident—it’s intentional. It requires trust, open communication, and a willingness to check egos at the door. Each member brings their own rhythm, but success comes from listening and adjusting to others. This is as true in the workplace as it is on the field or stage.

The Benefits of Working as One

When teamwork clicks, productivity soars. Studies show that teams built on mutual respect and collaboration are not only more innovative but also more resilient under pressure. Members feel valued, motivated, and supported, creating a positive feedback loop that lifts everyone higher.

Making It Work in Real Life

To build that “one band, one sound” culture, leaders and teammates alike must commit to:

Clear communication: Everyone knows their role and what success looks like.

Shared purpose: Each person understands how their contribution fits into the bigger picture.

Accountability: Individuals own their performance but remain loyal to the team’s mission.

Celebration of wins: Recognizing collective achievement strengthens unity and morale.

The Final Note

Teamwork really works—if you want it to. It’s not just about showing up; it’s about showing up for each other. When people align their goals, respect each other’s strengths, and perform with unity of purpose, the result is harmony in motion.

After all, in life as in music, the best sound comes when everyone plays their part—together.

Life is full of transitions—whether it’s buying your first home, changing careers, starting a family, or preparing for retirement. While these moments bring opportunity and excitement, they can also create uncertainty and stress. The good news: with proactive planning and professional guidance, individuals can navigate these turning points with greater confidence and clarity.

“Transitions can feel overwhelming because they often involve financial, emotional, and lifestyle changes all at once,” says certified financial planner Jenna Morales. “Having a plan and a professional partner to guide you helps you make informed decisions rather than emotional ones.”

The Power of Planning Ahead

Proactive planning means thinking ahead—mapping out potential outcomes and creating strategies that align with your long-term goals. It’s not about predicting the future but preparing for it. Whether you’re moving to a new city, managing an inheritance, or downsizing in retirement, foresight helps reduce risk and stress.

Professional advisors, from financial planners to insurance agents and career coaches, can offer valuable expertise to help identify blind spots and opportunities. They can also act as objective voices when emotions run high, ensuring you stay focused on your priorities.

Top Tips for Navigating Major Life Transitions

Start Early: Begin planning before the change happens. The earlier you prepare, the more control you’ll have over your options.

Clarify Your Goals: Define what success looks like for you—financially, emotionally, and personally.

Seek Professional Advice: Don’t go it alone. Certified experts can provide insights and structure your plan for maximum benefit.

Review Your Insurance and Finances: Major changes often affect your coverage needs and cash flow. Make sure your policies and budget reflect your new circumstances.

Build a Safety Net: Set aside emergency savings to cushion unexpected costs during transitions.

Stay Organized: Keep key documents—such as wills, policies, and financial records—accessible and updated.

Adjust as You Go: Life plans are not one-size-fits-all. Revisit and revise your strategy regularly as your needs evolve.

Focus on Mental Well-Being: Change can be stressful. Prioritize self-care and seek support when needed.

Moving Forward with Confidence

While no one can avoid life’s major transitions, being proactive and seeking professional guidance can transform uncertainty into opportunity. It’s about taking control of what you can—and having trusted experts help you navigate what you can’t.

“Confidence comes from preparation,” Morales adds. “When you plan ahead and surround yourself with knowledgeable support, you move forward not with fear—but with clarity.”

As we approach the end of 2025, the property insurance marketplace is navigating a mix of change, challenge and opportunity. Here’s a look at the key trends shaping the sector — and what they might mean for insurers, brokers and property owners alike.

1. Climate-Driven Losses Are Now the New Normal

The pace and severity of natural catastrophes continue to place major pressure on the property insurance market. The Swiss Re Institute estimates that global insured losses from natural catastrophes hit roughly US $80 billion in the first half of 2025, nearly double the 10-year average. (Reuters+2Insurance Journal+2) For insurers, that means heavier claims, tougher underwriting decisions and heightened scrutiny of exposures in high-risk zones.

What to watch:

Insurers will increasingly pull back or raise rates in high-catastrophe zones — e.g., coastal and wildfire-prone areas.

Property owners in those zones will receive stronger signals to invest in resilience (storm hardening, wildfire mitigation, flood defence).

Coverage gaps may grow where private insurers no longer provide adequate support, leading to more reliance on state/last-resort markets.

2. Pricing and Coverage Conditions Are Mixed — Softening in Some Segments, Hardening in Others

While recent years were characterised by sharp rate increases and tightening terms, there are signs that some parts of the market are stabilising or even softening. For example:

The Alera Group in its 2025 P&C update notes greater market stability, with disciplined underwriting, improving investment yields, and signs that premium growth may moderate. (Alera Group)

In commercial property, accounts with favourable loss history and limited catastrophe exposure may now see flat to single-digit rate increases, rather than the double-digit hikes of earlier years. (Dominion Risk+1)

On the flip side, in the homeowners/home-insurance space, average premiums remain elevated, and the insurers’ “combined ratio” suggests limited profitability in some segments. (Rate)

Key take-aways:

For well-performing risks, carriers are competing — more capacity, more flexible terms.

Brokers and agents who can help clients demonstrate strong mitigation/maintenance will be in demand.

3. Technology & Risk-Modelling Innovations Are Moving From “Nice to Have” to “Must-Have”

Insurers are rapidly expanding their use of technology — sensors, drones, satellite imagery, IoT monitoring, artificial intelligence — to refine risk assessments, improve underwriting and streamline claims. According to a recent legal-firm insight, insurers are deploying drones, satellite-imagery and IoT to track damage and property condition in real time. (Greenberg Traurig) Meanwhile, homeowners are seeing insurers push risk-mitigation incentives (smart-home sensors, leak detectors, fire-resistant construction) as a way to differentiate risk. (Rate)

What this means:

Risk-differentiation will widen: properties with upgraded resilience features may enjoy better terms/discounts.

Older or non-mitigated properties may face fewer options or harsher terms.

Agents and insurers who embrace these tools will have a competitive edge, especially in emerging hazard-zones.

4. Reinsurance and Capacity Pressures Remain Real

While direct insurance pricing may be moderating for some risks, the broader ecosystem — especially reinsurance — remains under strain. The costs of reinsurance for catastrophe risk continue to climb as global natural hazard exposures grow. (Greenberg Traurig) Also, some last-resort markets (state-backed, residual lines) are under pressure to raise rates or adjust eligibility, particularly in states with chronic exposure. (San Francisco Chronicle)

Implication: Insurers must manage their reinsurance treaties carefully, be selective about exposures they carry, and pass through appropriate pricing and terms to stay sustainable.

5. Market Size is Growing — With Geographic and Product Gaps Emerging

From a volume perspective, the property-insurance market remains on a growth path. For example, in North America the market for property insurance was projected to reach about US $365 billion in 2025, with a five-to-seven-year compound annual growth rate (CAGR) of nearly 7%. (Statista) Globally, a report projects the property-insurance market to be around US $364.75 billion in 2025, growing toward ~US$591 billion by 2034. (Business Research Insights)

Yet, growth is uneven:

Regions with escalating risk (wildfire, flood, storm) may struggle with supply and affordability.

Specialized products (wildfire-only, flood-only, resiliency add-ons) are gaining traction.

Bundled products (home + auto) and value-added services (risk-engineering, smart-home upgrades) are becoming differentiators.

6. Homeowners Face Increasing Burden — Affordability, Availability and Risk

For homeowners, especially in climate-exposed states (e.g., coastal Florida, wildfire-prone California), the challenges are mounting:

Rising premiums and deductibles: some reports show average home-insurance premiums nationally up ~20 % year-over-year in certain markets. (Rate+1)

Higher deductibles and more peril-specific deductibles (wind/hail, wildfire, flood) are becoming more common. (Matic Insurance)

Coverage availability is still strained in many high-risk ZIP codes; the E&S (Excess & Surplus) market is filling gaps. (Matic Insurance)

For agents and homeowners:

Risk mitigation (roof upgrades, fire-resistant landscaping, flood mitigation) is no longer optional—it can materially affect access and cost of coverage.

The choice of market (traditional carrier vs. surplus market) matters more than ever; early renewal/placement is advised.

For homeowners in highly exposed zones, budgeting for rising insurance costs (and potential policy non-renewals) is prudent.

7. Regulatory & Geographic Regulation Shifts

Regulators in states like Hawaii, Florida and California are responding to the stability challenges in property-insurance markets. For example, in Hawaii legislators pledged efforts to stabilise the market in the face of rising rates and insurers pulling out. (AP News) Rate filings and underwriting criteria adjustments are happening in several jurisdictions — meaning agents must stay abreast of local regulatory changes that could affect availability, coverage form, or premium.

Looking Ahead to Late 2025 and Early 2026

As we close out 2025, a few strategic themes for stakeholders:

For insurers and brokers: Market segmentation will deepen. Strong, well-mitigated risks will benefit from capacity and competition. Weakly mitigated risks will face greater terms and possibly coverage erosion.

For homeowners/property owners: Now is a contact point: review your property’s risk profile, invest in mitigation where possible, explore multiple carriers, and monitor renewal dates early.

For agents in your position (auto/property insurance): There’s an opportunity to advise clients on the “property side” in addition to auto — helping them understand risk exposures, mitigation, bundling opportunities, and market shifts. For example, bundling home + auto may give you more leverage.

For regulatory watchers: The interplay of climate risk, insurance affordability, and public policy will remain front-and-centre. Watch for state-level reforms, changes in last-resort insurers, and potential new coverage mandates or premium subsidies.

What Lies Ahead

The property-insurance market at the end of 2025 is in a state of transition. Big picture: demand is growing, but risk is mounting and not evenly distributed. Pricing and terms are moderating in some segments — yet for high-exposure zones the pressure remains acute. Technology, mitigation and geographic nuance will distinguish winners from laggards.

For you (and your clients) this means: be proactive. Know the risks. Position properties (or clients’ homes) for reward (through mitigation) rather than punishment. And stay flexible — the “next renewal” is likely to look quite different from the last.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

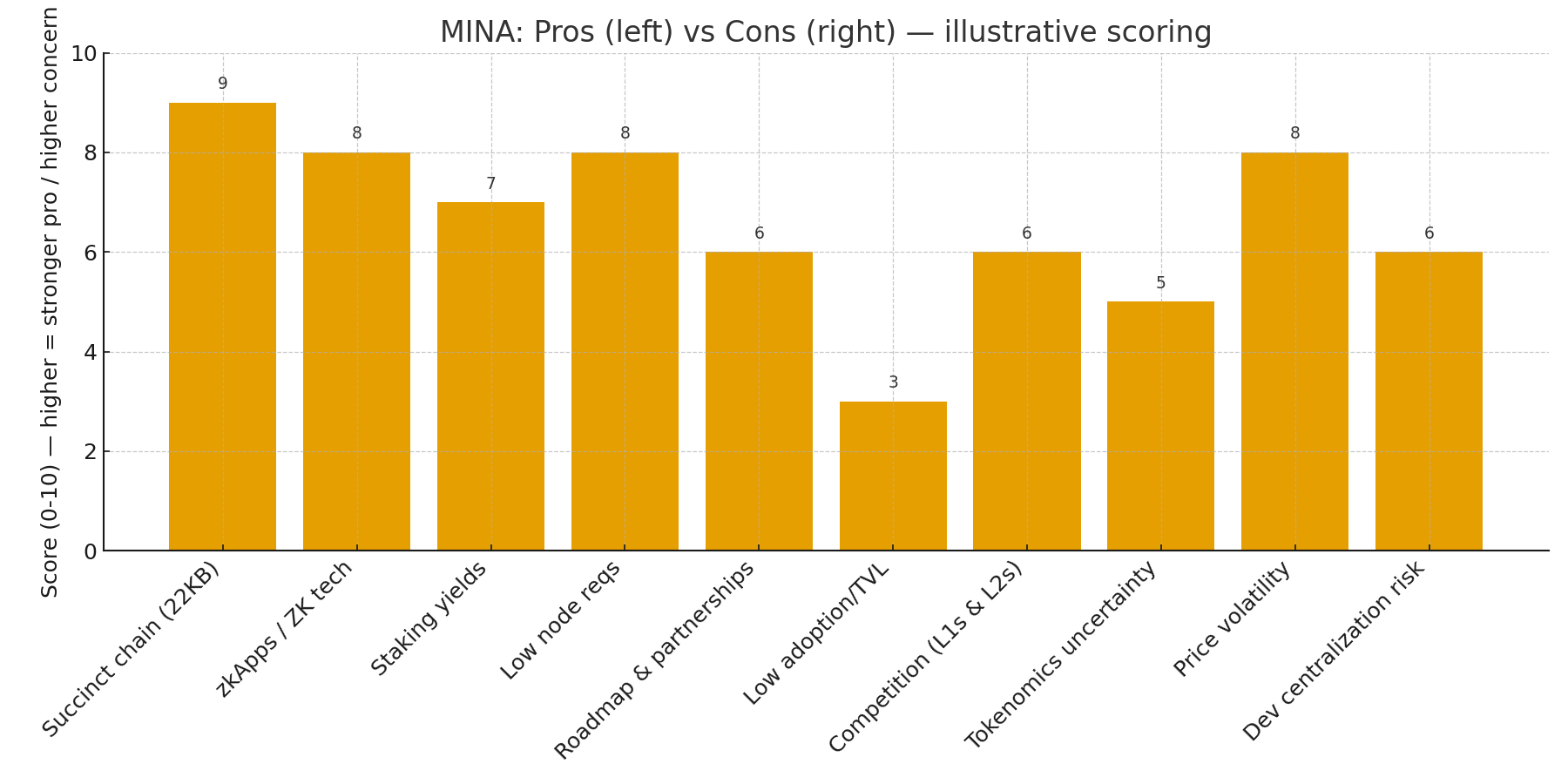

Mina Protocol markets itself as the “lightest blockchain” — a layer-1 that stays tiny by using recursive zero-knowledge proofs (zk-SNARKs) so the entire chain remains a succinct ~22KB snapshot instead of a growing ledger. That design promises a blockchain any device can verify, lowering node requirements and enabling on-device privacy-aware dApps (zkApps). Those technical foundations are Mina’s headline differentiator and the core reason some investors treat MINA as a long-term hold. (Mina Protocol+1)

Where MINA stands right now

As of early November 2025, MINA trades in the low-to-mid $0.17–$0.19 range with a market cap in the low hundreds of millions of dollars and roughly 1.26 billion MINA circulating. Price and ranking vary by source and exchange, but major market trackers show MINA as a mid-to-low market-cap altcoin. (CoinMarketCap+1)

Why investors like MINA — the bullish case

Truly lightweight chain: Mina’s constant-sized blockchain (~22KB) lowers the hardware and bandwidth needed to run a full node, which could help decentralize participation and boost mobile/edge use cases. This is fundamental to Mina’s pitch as a “blockchain for everyone.” (Nansen Research+1)

Zero-knowledge programmability (zkApps): Mina’s zkApp framework enables privacy-preserving smart contracts and verifiable off-chain computation. If ZK tech becomes central to mainstream Web3 privacy and scaling, Mina could capture unique developer interest. (Mina Protocol)

Staking yields / network rewards: MINA supports staking and many exchanges and platforms offer competitive staking APRs (examples reporting 6–12% or higher on various platforms), which attracts yield-seeking holders who prefer passive income while they wait for price appreciation. (Kraken+1)

Active roadmap and ecosystem work: Core development groups and community initiatives continue evolving Mina (roadmaps and upgrades in 2024–25 aim at tooling, zk developer onboarding, and greater interoperability). Continued protocol development can improve utility and adoption. (Mina Protocol+1)

Relatively small market cap = upside if narrative wins: Compared with top L1s, Mina’s market cap is modest, so positive adoption or a crypto risk-on rotation could produce outsized percentage gains (classic “small-cap upside” dynamic).

Risks and why caution is warranted

Adoption & TVL remain low vs major L1s: For MINA to move materially higher, it needs more apps, users, and locked value. Today it’s still a niche stack versus giants like Ethereum, Solana, or new ZK-focused rivals. Low TVL limits organic utility demand for the token. (CoinGecko+1)

Strong competition: Other projects are pursuing ZK tech, rollups, and lightweight verification. If larger ecosystems integrate similar ZK capabilities (or if Ethereum rollups dominate the ZK narrative), Mina’s unique edge could shrink. (o1Labs)

Tokenomics & supply dynamics: A large circulating supply (~1.26B MINA) and ongoing issuance/staking rewards can dilute price upside unless demand grows to absorb supply. Coin trackers list circulating supply but no fixed “max” supply, so inflation mechanics matter to holders. (CoinMarketCap)

Price volatility & market risk: As a mid/low-cap crypto, MINA is susceptible to broad market moves, liquidity shocks, and volatility — factors that can erase gains quickly. Historical price charts show sharp swings that should caution risk-sensitive investors. (Yahoo Finance)

Technology / centralization risk: While Mina’s research teams (o1 Labs, Mina Foundation, community contributors) are active, concentrated development or coordination risks exist — and any delays or setbacks to roadmap items could temper market enthusiasm. (o1Labs)

Potential upside in an “altcoin season”

Altcoin seasons reward narratives — smaller caps with clear, differentiated value propositions often run hardest. Mina’s narrative (real ZK programmability + tiny chain size) fits a neat theme: privacy, edge verification, and on-device dApps. If the ZK narrative accelerates — through developer tool improvements, interoperability wins (projects like Aligned working on ZK verification integrations), or a wave of zkApps adoption — MINA could outpace larger, less nimble chains. Several mid-2024–25 developments and roadmap items indicate the team remains focused on ZK tooling and ecosystem funding, which would be the necessary fuel for such a move. (o1Labs+1)

How an investor might position (not financial advice)

Long-term speculative hold: If you believe ZK tech and ultra-light clients matter, a small allocation to MINA (size depending on risk tolerance) could be reasonable — especially if you stake to capture yield while waiting for adoption. (Kraken)

Event-driven trade: Watch roadmap milestones, zkApp launches, partnerships (e.g., Aligned/Ecosystem announcements), and listings/staking product rollouts. Positive, repeated dev activity and growing on-chain usage are bullish triggers. (Mina Protocol+1)

Risk management: Given volatility and competition, position sizing, stop levels, and a clear thesis (what adoption metric would make you add more vs cut losses) are essential.

End Result

Mina’s technology is interesting and differentiated: a truly succinct chain with ZK programmability that theoretically lowers barriers to running full nodes and enables privacy-preserving dApps. That technical moat gives MINA a plausible role in a future Web3 where ZK proofs are central. However, adoption, TVL, competition, tokenomics, and market volatility remain the main hurdles. For investors, MINA looks like a classic higher-risk, higher-optional-upside altcoin: attractive to those who believe in ZK-native dApps and willing to stomach swings; less attractive to conservative crypto investors who prefer larger, more established L1 ecosystems. (Mina Protocol+2CoinMarketCap+2)

Disclaimer

I currently hold a position in MINA. The views and opinions expressed in this article are my own and are provided for informational purposes only. This content should not be construed as financial, investment, or trading advice. Always conduct your own research or consult with a licensed financial advisor before making investment decisions.

As daylight fades and drivers take to the roads after sunset, the risks rise dramatically. According to the National Safety Council, the fatal crash rate at night is about three times higher than during the day. Despite making up only a small portion of total driving time, nighttime driving accounts for nearly 50% of all traffic deaths in the United States each year.

Experts point to one primary reason: reduced visibility. Even with streetlights and modern vehicle technology, the human eye struggles in low-light conditions. But what many drivers don’t realize is how much their own vehicle’s headlights can contribute to the danger.

Over time, headlight lenses become cloudy or yellowed from oxidation, cutting light output by as much as 50%. Bulbs can also dim gradually, often without the driver noticing, and misaligned headlights may shine too low or too high, limiting visibility or blinding oncoming traffic.

“Headlights are your first line of defense at night,” says a local automotive safety technician. “Keeping them clean, bright, and properly aimed can make the difference between spotting a hazard in time or not at all.”

Regular maintenance—such as cleaning lenses, checking bulb brightness, and ensuring correct alignment—can dramatically improve safety. Replacing bulbs in pairs and restoring headlight covers can also restore lost visibility and reduce glare for others.

Drivers should also be mindful of when they’re on the road. Statistics show that the hours after midnight are the most dangerous, as fatigue, alcohol impairment, and reduced alertness peak. For the safest travel, experts recommend getting home before midnight whenever possible.

In short, maintaining your headlights isn’t just about looks—it’s about safety. As nights grow longer, take a few minutes to check your car’s lights. It could be one of the simplest ways to protect yourself and everyone else on the road.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

When it comes to homeowners insurance, accuracy is everything. One of the most critical tools used to protect your biggest investment is the Replacement Cost Estimator (RCE)—a system that helps determine how much it would actually cost to rebuild your home from the ground up after a covered loss. Unfortunately, many homeowners underestimate their home’s true value, leading to painful surprises when disaster strikes.

The RCE takes into account today’s construction costs, materials, labor, and local building codes to calculate an accurate rebuilding cost—not the market price of your home. With inflation in construction and fluctuating material prices, relying on outdated or ballpark figures can leave you dangerously underinsured. If your policy doesn’t reflect your home’s current replacement cost, you could end up paying tens—or even hundreds—of thousands—out of pocket after a total loss.

It’s not just the structure that matters. Personal property coverage—the protection for your belongings like furniture, electronics, and clothing—should also reflect their true replacement value. Too often, people underestimate what it would take to replace everything they own. And don’t overlook loss of use coverage, which helps pay for temporary housing and living expenses if your home becomes uninhabitable. Skimping on this area could make a tough situation even harder if you’re displaced for months during repairs.

The bottom line: an accurate RCE ensures your dwelling, personal property, and loss of use coverages keep pace with reality. Take time to review your policy annually, ask your agent to update your RCE, and avoid the false comfort of being “covered” for less than what you’d actually need. When life’s unexpected moments happen, being properly insured is what helps you rebuild—not just your home, but your peace of mind.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As the vibrant colors of fall begin to fade and the crisp chill of winter settles in, we prepare for one of the most noticeable transitions of the year—the end of Daylight Saving Time. On Sunday, November 2nd, clocks “fall back” one hour, marking the shift to standard time. While the extra hour of sleep sounds like a treat, the darker evenings and shorter days can affect more than just our schedules—they can influence our mood, energy, and overall well-being.

The Emotional Shift of Seasonal Change

Many people notice a change in their mood this time of year. With less sunlight and longer nights, it’s common to feel more sluggish, irritable, or even down. This phenomenon, often referred to as the “winter blues,” can stem from disruptions in our body’s internal clock and reduced exposure to natural light. Some individuals experience a more serious form called Seasonal Affective Disorder (SAD), which can bring on symptoms similar to depression.

Experts note that our brains rely on sunlight to regulate serotonin (the “feel-good” hormone) and melatonin (which controls sleep). When daylight hours shrink, so does our natural boost in mood and energy. But with a little preparation and self-care, you can ease the transition and keep your spirits high.

7 Simple Ways to Feel Better During the Time Change

Set Your Clocks Back — Remember to turn your clocks back one hour before bed on Saturday night. It’s a small step that helps keep your schedule on track.

Get Morning Sunlight — Spend at least 15–30 minutes outdoors in the morning light. It helps reset your body clock and improves alertness.

Keep a Consistent Sleep Schedule — Go to bed and wake up at the same time each day, even on weekends. Consistency helps regulate your energy.

Stay Active — Physical activity boosts mood and helps combat sluggishness. Try indoor workouts, yoga, or brisk walks during daylight hours.

Eat Well — Foods rich in vitamin D, omega-3s, and whole grains can help stabilize mood and energy levels.

Use Light Therapy — Consider a light therapy lamp to mimic natural sunlight if you spend most of your time indoors.

Stay Social — Don’t hibernate! Stay connected with friends and family to keep your spirits up.

As we “fall back” into standard time, it’s a perfect opportunity to slow down, reflect, and adjust your routines for the months ahead. Embrace the cozy side of the season—warm drinks, soft blankets, and quiet evenings—and take care of both your body and your mind.

Because while we can’t control the darkness of winter, we can always create our own light. ☕🍂🕰️

Opendoor Technologies (NASDAQ: $OPEN), the best-known public “iBuyer” that buys, renovates and resells homes, has gone from near-obscurity to the center of a retail-investor frenzy — and to a renewed debate among analysts about whether the company is finally turning a corner or simply a high-risk turnaround story.

Over the last few months OpenDoor’s shares have swung dramatically: the stock traded around $7.70–$8.00 at the end of October 2025 and the company’s market capitalization sits in the $5–6 billion range, after a year of volatile trading that included a multi-hundred-percent YTD gain. (Yahoo Finance+1)

What changed recently

Several headline events have driven sentiment:

Leadership and board moves: Opendoor brought in Kaz Nejatian (former Shopify COO) as CEO and welcomed co-founders (including Keith Rabois) back into senior board roles; those governance shifts have been cheered by retail investors and credited with a share-price pop. (Barron’s)

Institutional attention and retail momentum: a disclosed stake by trading firm Jane Street and visible retail groups (“Open Army”) helped amplify demand and liquidity in the stock, intensifying swings. (Investopedia+1)

Changing operating results: Opendoor reported stronger operating metrics in 2025 quarters, including a notable adjusted-EBITDA improvement (the company posted roughly $23M adjusted EBITDA in Q2 2025), and guidance that signaled more predictable contribution profit heading into Q3 — although management warned of macro and inventory risks. (investor.opendoor.com+1)

Those items explain the run-up in price and the renewed investor conversation — but they do not answer whether the stock is a good investment for a given investor. Below we lay out the primary reasons for and against considering Opendoor as a buy, and then present a compact comparison table against a few direct/adjacent competitors.

Investment case — the arguments for buying

Path to a more capital-light business mix. Management has publicly emphasized diversifying away from pure house flipping and toward capital-light revenue (listings, agent referrals and platform services). If executed, that could reduce inventory/interest-rate exposure and lift margins. (Nasdaq)

Operational improvement indicators. Opendoor reported improved contribution margins/adjusted EBITDA in 2025 quarters, indicating they can be profitable on a run-rate basis under current housing conditions when volumes and pricing cooperate. That shows the business has levers to control costs and marketing spend. (investor.opendoor.com+1)

Retail + selective institutional support can sustain valuation re-rating. The combination of vocal retail investors and large trading desks taking stakes can produce favorable secondary-market momentum and liquidity — often important for smaller, restructuring names. Recent stake disclosures and active retail communities materially contributed to price appreciation. (Investopedia+1)

Investment case — the arguments against buying

Still fundamentally exposed to housing and rates. iBuying profitability depends on narrow purchase/resale spreads. High mortgage rates, slower transaction volumes and inventory carrying costs can quickly turn contribution profit negative; management itself has warned of those macro risks. (AInvest)

Historical unprofitability and scale risk. Despite pockets of positive adjusted EBITDA, Opendoor remains a company that has reported large GAAP losses in recent years and must prove sustained, repeatable profitability at scale. Analysts and some sell-side desks still view the firm skeptically. (Investopedia+1)

Valuation and momentum risk (meme-stock dynamics). Part of the recent price action appears driven by retail fervor and narrative (founder/board changes, social campaigns). If sentiment cools or short interest/unfavorable headlines resume, the stock can be highly volatile. Institutional disclosures (e.g., Jane Street) can be neutral in economic intent — they don’t guarantee long-term fundamental support. (Investopedia+1)

Quick facts & signals investors should check before deciding

Recent price / market cap: ~$7.7–$7.8 per share, market cap roughly $5–6B (end of October 2025). (Yahoo Finance+1)

Recent operating cue: Q2 2025 reported ~$1.6B revenue and $23M adjusted EBITDA (management said this was their first quarter of positive adjusted EBITDA in the recent cycle). Management gave guidance for Q3 2025 but flagged inventory & macro risks. (investor.opendoor.com+1)

Sentiment shocks: Return of co-founders/board changes + Jane Street stake disclosure drove major intraday moves and an extended retail buying wave in mid-to-late 2025. (Barron’s+1)

Table shows representative market snapshots and price-movement indicators as reported publicly in late Oct 2025. Percent figures are illustrative based on publicly reported YTD or 1-year performance where available; use the cited links to verify live numbers before trading.

Company (ticker)

Business focus

Representative price (late Oct 2025)

Market cap (approx.)

Notable recent move / comment

Opendoor (OPEN)

iBuyer / online home marketplace

~$7.7 (Oct 31, 2025). 52-wk range: $0.51–$10.87.

$5–6B.

Big YTD rally driven by board changes, CEO hire & retail interest; Q2’25 adjusted EBITDA improvement. (Yahoo Finance+2StockAnalysis+2)

How a pragmatic investor might think about sizing a position

Risk-aware, small allocation: If you believe management can execute and you want exposure to an asymmetric upside (turnaround + retail momentum), consider a modest, portfolio-hedged allocation (small percent of liquid equities), with strict stop or re-evaluation triggers tied to subsequent earnings and inventory metrics.

Event-driven play: Some traders view Opendoor as an event trade (earnings, board/management updates). That strategy requires active monitoring and is not suitable for buy-and-hold retirement capital.

Avoid if you need steady income/low volatility: Opendoor is not a conservative equity — it’s a high-volatility name with housing and interest-rate sensitivity.

What to watch next (near-term catalysts)

Q3 2025 earnings / management commentary (Nov 6, 2025): updated revenue, contribution profit, inventory levels and margin guidance will matter. Opendoor plans a novel “Financial Open House” investor presentation that could influence retail interest. (investor.opendoor.com+1)

Inventory and financing costs: how much inventory they hold and the cost to finance that inventory as mortgage rates move. (AInvest)

Any further institutional filings: large 13F/13D/13G filings or insider transactions (adding/removing high-profile board members) can swing sentiment quickly. (Investopedia+1)

Long and Short

Opendoor sits at the intersection of a real operational story (improving contribution metrics, attempts to move into capital-light revenue) and a high-sensation market story (retail fervor, activist board moves, and short-squeeze/meme dynamics). That combination creates both upside and downside:

If you believe management can repeat profitable quarters, diversify revenue and steadily shrink inventory risk, Opendoor could be a high-reward turnaround play.

If you believe that housing-cycle risk, rate sensitivity, and structurally low flipping spreads will persist, then the stock remains a speculative, momentum-driven bet that could reverse sharply.

Before making any trade, check the latest quarter results, read management’s Q&A from the upcoming November presentation, and confirm up-to-the-minute prices/position filings — the environment around Opendoor is unusually fast-moving and sentiment-sensitive. (investor.opendoor.com+2Quiver Quantitative+2)

Disclaimer

I currently hold a personal position in Opendoor Technologies Inc. (NASDAQ: OPEN). This article is provided for informational and educational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any securities. Investors should conduct their own research or consult a licensed financial advisor before making investment decisions.

References

Barron’s. (2025, October 31). Opendoor Technologies Inc. (OPEN) stock price, quote, and news. Retrieved from https://www.barrons.com

Business Insider. (2025, October 31). Opendoor Technologies Inc. (OPEN) stock performance and financial data. Retrieved from https://markets.businessinsider.com

CNBC. (2025, October 25). Opendoor shares surge after leadership shake-up and board changes. Retrieved from https://www.cnbc.com

MarketWatch. (2025, October 31). Opendoor Technologies Inc. stock overview and financial results. Retrieved from https://www.marketwatch.com

Nasdaq. (2025, October 30). Opendoor Technologies Inc. (OPEN) company profile and financials. Retrieved from https://www.nasdaq.com

Opendoor Technologies Inc. (2025). Q2 2025 shareholder letter and financial results. Retrieved from https://investor.opendoor.com

Reuters. (2025, October 27). Opendoor Technologies sees EBITDA improvement, guidance for Q3 2025. Retrieved from https://www.reuters.com

Seeking Alpha. (2025, October 28). Opendoor Technologies Q2 earnings report analysis. Retrieved from https://seekingalpha.com

Yahoo Finance. (2025, October 31). Opendoor Technologies Inc. (OPEN) stock price, history, and market cap. Retrieved from https://finance.yahoo.com

Zillow Group Inc. (2025, October 30). Company financials and stock price. Retrieved from https://www.zillowgroup.com

Offerpad Solutions Inc. (2025, October 30). Company profile and stock chart. Retrieved from https://www.offerpad.com

Redfin Corporation. (2025, October 29). Rocket Companies announces acquisition of Redfin at $12.50 per share. Retrieved from https://www.redfin.com/news

Halloween has always been more than just costumes and candy to me—it’s a celebration of creativity, community, and connection. Every October 31st, the air fills with excitement and the scent of autumn leaves, as neighborhoods come alive with laughter, decorations, and the unmistakable crunch of candy wrappers.

For me, Halloween is about sharing the fun. It’s the night when families come together, friends roam the streets in costume, and everyone—young or old—gets to feel like a kid again. Whether it’s carving pumpkins with family, trading candy with friends, or just admiring the creativity of neighborhood displays, Halloween brings people closer in ways few other holidays can.

The candy, of course, is part of the magic. I still get a nostalgic thrill seeing a bowl filled with mini chocolate bars and colorful wrappers. But even more than the treats, it’s the shared experiences that make the night unforgettable—the laughter, the spooky stories, and the small acts of kindness between neighbors.

As much fun as Halloween is, it’s also important to stay safe while celebrating. Here are a few simple reminders to keep the night full of treats and free of tricks:

🕯️ Halloween Safety Tips

Stay visible. Wear reflective tape or carry glow sticks to make sure drivers can see you.

Check costumes for safety. Avoid masks that block vision and make sure shoes fit properly to prevent tripping.

Stick with a group. Trick-or-treating is always safer—and more fun—with friends or family.

Watch for traffic. Use sidewalks and crosswalks, and never assume drivers can see you.

Inspect your candy. Check all treats before eating—especially anything unwrapped or homemade from strangers.

Keep pets inside. Halloween can be stressful for animals; make sure they’re safe and comfortable.

Be mindful of decorations. Open flames, cords, and fog machines can be hazards—keep pathways clear.

Respect others’ property. Stay on paths and avoid trampling lawns or decorations.

This Halloween, I’ll be out enjoying the fall air, greeting neighbors, and sharing laughs with the people who make the night so special. Because in the end, Halloween isn’t just about the candy—it’s about the memories we make along the way. 👻🍬