Being a caregiver is often described as one of the most selfless roles a person can take on. Whether caring for an aging parent, a child with special needs, or a loved one facing illness, caregivers provide daily support, patience, and compassion that are nothing short of extraordinary. But while they devote themselves to others, many caregivers struggle to prioritize their own well-being.

According to recent studies, caregivers are more likely to experience stress, fatigue, and health challenges due to the demands of their responsibilities. Experts agree that while the focus is naturally on the person receiving care, it’s just as important to provide resources and relief for those who give it.

So where can caregivers turn when it’s time to think about their own needs? The answer lies in small but meaningful acts of support from the community. If you know a caregiver who may need a helping hand, here are some simple yet effective ways you can make a difference:

Offer Practical Help – Everyday tasks like grocery shopping, meal prep, or running errands can be a heavy burden. Volunteering your time for these chores can give caregivers much-needed breathing room.

Be a Listening Ear – Sometimes, what a caregiver needs most is someone to talk to. Offering compassion and a safe space to share can ease feelings of isolation.

Encourage Self-Care – Remind caregivers that their health matters, too. Encourage them to rest, exercise, or take short breaks without guilt.

Connect Them to Resources – Local support groups, respite care services, and online communities can provide additional help and understanding.

“Caregivers are the backbone of our communities, but they can’t pour from an empty cup,” said one local health advocate. “Showing kindness and offering support ensures that they, too, have the strength to continue their vital role.”

Being a caregiver is about love and responsibility—but it should never mean going it alone. By recognizing the challenges caregivers face and stepping in with support, friends, neighbors, and family members can play a key role in making their journey a little lighter.

Snowflake Inc. (NYSE: $SNOW) released its second quarter (fiscal 2026) results, reinforcing its role as a data and AI infrastructure play while navigating challenges in profitability and valuation. The reaction in markets suggests that investors are increasingly viewing Snowflake as more than just a cloud data warehousing provider — but as a core enabler of “AI Data Cloud” strategies. Here’s a breakdown of what’s happening, and the bull vs bear cases moving forward.

What the Numbers Say: Q2 & Recent Financials

Revenue, Margins & Growth

In Q2 FY2026, Snowflake reported product revenue of $1,090.5 million (i.e. from compute, storage, and data transfer). (Snowflake Investors)

The company continues to emphasize net revenue retention, which remains elevated (125%) as of July 31, 2025 — indicating that existing customers are expanding usage. (Snowflake Investors)

In its Q4 FY2025 results (ended January 31, 2025), Snowflake posted total revenue of $986.8 million, with product revenue of $943.3 million — up ~28% year-over-year. (Snowflake)

The Q4 gross profit margin (GAAP) was ~ 66%, and non-GAAP adjusted gross margin (excluding stock-based comp, amortization, etc.) was ~ 73%. (Snowflake)

Snowflake’s Q4 operating loss (GAAP) was about –$386.7 million, but on a non-GAAP basis it posted operating income of $92.8 million (≈ 9% margin). (Snowflake)

Its free cash flow in that quarter was ~$415.4 million (≈ 42% of revenue) and adjusted free cash flow ~$423.1 million. (Snowflake)

These numbers show both strength and tension: strong top-line growth and healthy non-GAAP profit conversions, but continued GAAP losses driven by sizable investments, stock compensation, and amortization.

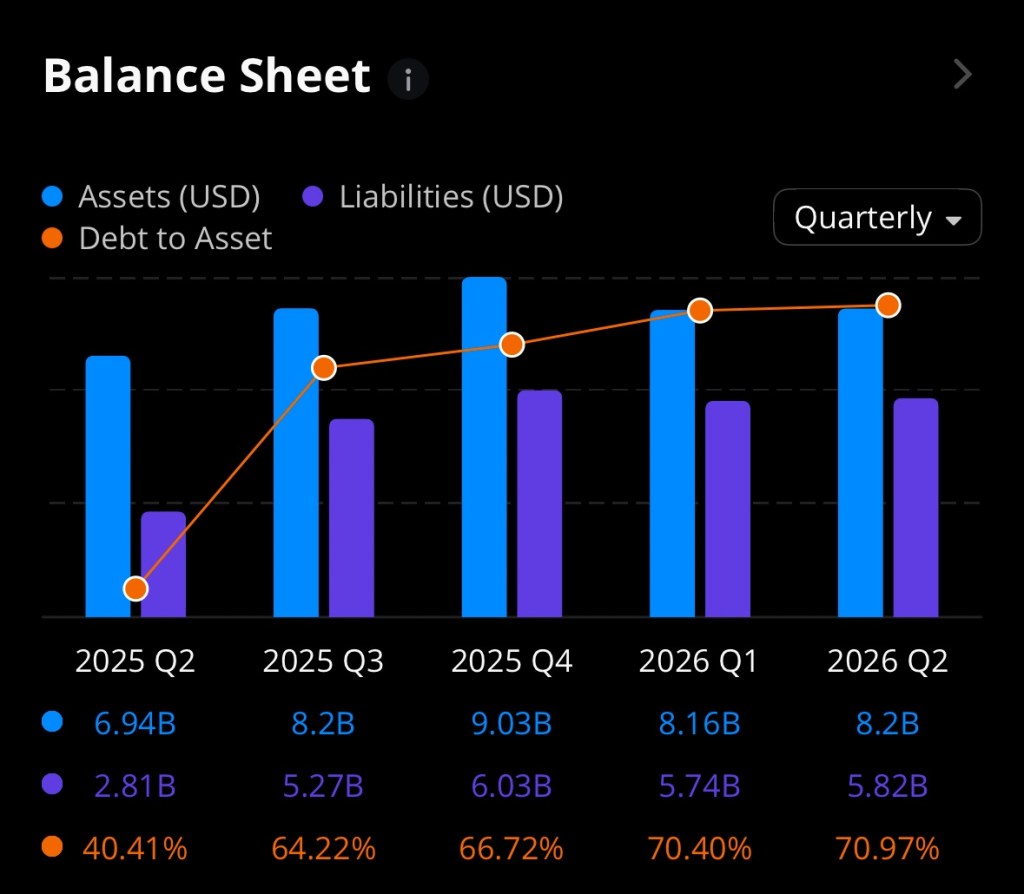

Balance Sheet & Liquidity

As of January 31, 2025, Snowflake held ~$2,698.7 million in cash, cash equivalents, and restricted cash. (Snowflake)

Total debt (short-term + long-term) is more modest — for example, in recent annual balance sheet summaries, SNOW’s short-term and current portion of long-term debt is listed in the range of ~ $36 million. (The Wall Street Journal)

On the assets side, total assets are in the realm of several billions (over $8B to $9B in some reports) with growth trends consistent among public disclosures. (Investing.com+1)

The company carries significant liabilities as well (deferred revenue, vendor payables, deferred costs), but its liquidity cushion offers some buffer against short-term shocks. (Investing.com)

Business & Strategic Metrics

Snowflake’s remaining performance obligations (RPO) — i.e., contracted but not-yet-recognized revenue — stood at $6.9 billion, growing ~33% year-over-year. (Snowflake)

The company serves 580 customers whose trailing 12-month product revenues exceed $1 million, and 745 Forbes Global 2000 customers as of Q4 FY2025. (Snowflake)

The 125% dollar-based net revenue retention underlines that Snowflake is often able to upsell or expand within its installed base. (Snowflake Investors)

More recently, Snowflake announced its acquisition of Crunchy Data (for ~ $250 million) to integrate Postgres capabilities into its ecosystem, enabling developers to more easily build AI agents and manage data workloads. (The Wall Street Journal+1)

The company is also partnering or aligning more closely with AI/LLM providers (e.g., Anthropic), seeking to embed language model capabilities into its platform. (Reuters+2markets.businessinsider.com+2)

What’s Driving the Recent Move & Market Sentiment

In response to its Q4 FY2025 earnings (released earlier in 2025), Snowflake’s stock jumped ~10.9% after hours, as the company beat on earnings (30 cents per share vs ~18 cents expected) and revenue (nearly $987 million vs $957 million consensus). Barron’s It also raised its forecast for product revenue and delivered upbeat guidance for FY2026, projecting ~24% growth to ~$4.28 billion. (MarketWatch+2Barron’s+2)

Investors have taken notice of Snowflake’s push into AI, including more sophisticated integrations with large language models, and its efforts to position itself not just as a data platform but an “AI data cloud” enabler. (markets.businessinsider.com+2Reuters+2)

That said, concerns still linger over valuation multiples (Snowflake trades at high forward multiples), GAAP losses, and macro risk to enterprise IT spending.

Why Some Investors Might Find SNOW Attractive (and Its Risks)

Bull Case

Exposure to Secular Trends in Data + AI As enterprises shift toward AI, data modeling, real-time analytics, and agent-based applications, Snowflake sits at a nexus: you need scalable, secure data infrastructure. Its existing customer base, product maturity, and retention metrics lend credibility to that positioning.

Upsell & Expansion Potential Snowflake’s high net revenue retention and expanding average spend per customer suggest that a lot of value lies in selling more compute/storage or ancillary AI features to its installed base.

Strategic Acquisitions & Technology Stack Expansion The Crunchy Data deal, combined with its AI platform integrations, may help lock in more workloads (especially developer, data app, and AI agent workloads) and reduce friction for adoption.

Cash Generative Capacity (Non-GAAP / FCF) Despite GAAP losses, Snowflake has shown strong adjusted free cash flow generation, which gives it flexibility to invest, defend, or expand without complete reliance on external financing.

Backlog / Contracted Revenue Visibility The RPO metric provides a view into future revenue, giving some predictability to growth expectations and lessening the reliance purely on new deals.

Risks & Challenges

Profitability & Cost Pressure Snowflake still runs GAAP losses. Its heavy investment in R&D, sales & marketing, and stock-based compensation make margins sensitive. If growth slows, the pressure on margins will intensify.

Valuation Overhang At high multiples, the stock’s valuation leaves little room for mistakes. A small slip in guidance or macro softness in enterprise IT spending could cause multiple compression.

Competition & Execution Risk The competitive landscape is fierce (e.g. Databricks, AWS, Google, Microsoft) and execution (product development, scaling, integrating acquisitions) will matter enormously.

Dependence on Cloud Providers Snowflake relies on underlying public clouds (AWS, Azure, GCP) for infrastructure. Any changes in pricing, caps, or ecosystem dynamics could affect its cost structure or competitiveness. (Wikipedia+1)

Macro / IT Spend Weakness In a downturn or with tightening enterprise budgets, large IT and data platform spends may get deferred, impacting growth.

Integration and Engineering Complexity Adding deeper database, AI, and application layers increases complexity — integrating acquisitions and maintaining stability and performance across features will be demanding.

Outlook & Near-Term Catalysts

Snowflake’s guidance for Q1 FY2026 product revenue is in the range $955 million to $960 million. (Snowflake)

For full-year FY2026, the company expects ~ 24% product revenue growth to ~$4.28 billion, with non-GAAP product gross margins reaching ~75%. (Snowflake)

The success of its Crunchy Data acquisition (Postgres integration), traction of AI integrations (e.g., embedding LLMs for analytics), and customer growth in large enterprises will be closely watched.

If Snowflake can continue delivering above expectations on product revenue, manage its cost base, and ensure that its AI/data additions translate into incremental revenue without diluting execution, it may justify its premium valuation post its recent run.

Verdict & Investor Fit

Snowflake is not a “safe” stock in the sense of predictable earnings or low volatility, but it is a compelling pick for investors with conviction in the data + AI transition and a willingness to ride through lumps. For those looking for asymmetric upside exposure to the AI/data infrastructure stack, SNOW has a profile worth watching — especially if bought during periods of market softness.

Disclosure:

I do not own any stock or have any financial interest in Snowflake Inc. (NYSE: $SNOW). This article is for informational purposes only and should not be considered financial or investment advice. Investing in stocks carries risks, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

High Dividend Yield & Track Record Target currently pays $4.56 annually ($1.14 per quarter), translating into a robust ~4.9% yield on today’s ~$93 share price (StockAnalysisTipRanks). The company has increased its dividend for 54 consecutive years, a hallmark Dividend King that inspires investor confidence (NasdaqStockAnalysis). Its most recent raise (1.8%) was declared in June 2025, effective with the $1.14 quarterly payment on Sept 1, 2025 (ex-div Aug 13) (Target Corporation).

Payout Coverage & Sustainability Target retains a payout ratio of roughly 52%—meaning it distributes just over half of earnings as dividends, leaving room to reinvest and buffer downturns (KoyfinStockAnalysis). It also generated ~$2.9 B in free cash flow over the past 12 months, comfortably above its roughly $2 B annual dividend obligation (Nasdaq).

Valuation Lean vs Peers At a P/E near 11×, Target trades well below peers like Walmart (~37×), suggesting the market has priced in current headwinds—offering potential upside if operational trends normalize over time (Nasdaq).

🧾 Balance Sheet Overview (as of latest trailing 12 mo / August 2025)

Target maintains a healthy asset base, anchored by substantial property, inventory, and cash buffers. Long‐term debt is sizable but manageable given recurring cash flow. Equity has grown steadily (~$14.7 B in FY 2024 to ~$15.4 B TTM), with tangible book value per share near $34—over one-third of share price (StockAnalysis).

🔍 Business Momentum & Outlook

Recent performance (Q2 FY 2025): Net sales declined ~0.9% YoY and comp sales fell ~1.9%, though digital sales rose ~4.3%. Operating income slipped ~19% to $1.3 B. Full-year EPS guidance remains at $8.00–$10.00 GAAP (adjusted ~$7–$9) (Target Corporation).

Strategic tailwinds: Investments in same-day fulfillment via Shipt, modernization of logistics, and omnichannel integration are expected to drive margin recovery (expected to improve toward ~6% by FY 2028) (University of Iowa).

💡 Investment Case: Why Consider TGT

Reliable, high income: ~4.9–5.0% yield, backed by decades of increases.

Dividend sustainability: Strong cash flow vs payout; modest payout ratio.

Undemanding valuation: Trading at low P/E, offering value if business stabilizes.

Long-term turnaround potential: Operational improvements could bolster margins and share price over time.

Risks include macro-sensitive retail environment, margin pressures, inventory mismanagement, and stiff competition. However, the dividend acts as a buffer while strategic moves take root.

📌 Bottom Line

For income-focused investors looking to pair dividend yield with capital appreciation potential, Target (TGT) stands out as a compelling blended opportunity. Its long-standing dividend credibility, backed by solid free cash flow and a durable balance sheet, makes it a defensive anchor in a portfolio. Coupled with low valuation and a clear path to operational recovery, TGT offers both yield today and upside tomorrow.

Disclosure: I currently hold a position in Target Corporation (NASDAQ: $TGT). This article reflects my personal opinions and analysis, and is not intended as financial advice. Please conduct your own research or consult a financial advisor before making any investment decisions.

Success is often measured in numbers—bank accounts, investments, or even social media followers—the deeper meaning of being both healthy and wealthy can sometimes get lost. For me, the phrase isn’t about chasing material excess, but about balance, fulfillment, and sustainability in both body and mind.

Health as the Foundation Health is more than the absence of illness; it’s the daily practice of treating your body and mind with respect. For me, that includes maintaining energy to do the things I love, fueling my body with good food, and taking time to reduce stress. Without health, even the greatest fortune feels empty. Wealth is meaningless if you don’t have the strength or clarity to enjoy it.

Wealth Beyond Money When I think of being “wealthy,” I don’t immediately picture luxury cars or sprawling mansions. Instead, I see freedom—the freedom to spend time with loved ones, pursue passions, and give back to the community. True wealth, to me, includes financial security, but also peace of mind, strong relationships, and opportunities to grow.

Healthy and Wealthy Together The two go hand in hand. Being healthy allows me to work toward financial stability with focus and determination. Being financially stable allows me to invest in my health—whether that’s quality healthcare, nutritious food, or the ability to take time off when I need it. Together, they create a cycle that builds not just a lifestyle, but a legacy.

A Personal Vision Ultimately, “healthy and wealthy” means living in a way that supports long-term happiness. It’s about waking up each day with energy, knowing I have the resources to handle life’s challenges, and feeling grateful for both the small and big wins. To me, that’s real success—being rich in health, rich in love, and rich in purpose.

When it comes to protecting wealth and passing it on to loved ones, many families are discovering that a simple will may not be enough. Increasingly, individuals are turning to trusts as a more effective way to manage their assets and provide security for beneficiaries. While wills remain common, trusts offer unique advantages that make them an essential tool in modern estate planning.

A trust is a legal arrangement in which a trustee manages assets on behalf of beneficiaries. Unlike a will, which becomes public during probate, a trust can keep family financial matters private while ensuring assets are distributed according to the grantor’s wishes.

Avoiding Probate Delays and Costs One of the main reasons individuals choose a trust is to avoid probate—the court-supervised process of distributing an estate after death. Probate can take months or even years, and legal fees can significantly reduce what heirs actually receive. With a trust, assets are transferred more quickly and with fewer administrative costs.

Tax Efficiency and Asset Protection Certain types of trusts can also provide tax advantages. For high-net-worth individuals, this can mean minimizing estate taxes, while others use trusts to shield assets from creditors or lawsuits. Parents of minor children often create trusts to ensure their children’s financial needs are met in the event of an untimely death.

Control Over Distribution Unlike a will, which typically results in a lump-sum transfer of assets, a trust allows for customized distribution. For example, beneficiaries can receive funds at certain ages, in installments, or for specific purposes such as education or healthcare. This level of control provides peace of mind for those worried about heirs’ financial responsibility.

Peace of Mind for Families “Trusts aren’t just for the wealthy,” says estate planning attorney Sarah Mitchell. “They’re tools that provide structure, protection, and clarity—things every family can benefit from. For many clients, it’s about peace of mind knowing their loved ones are taken care of.”

As life expectancy increases and wealth is passed down through generations, experts predict that more families will explore trusts as part of their financial planning. Whether it’s avoiding probate, protecting assets, or ensuring responsible inheritance, trusts are becoming a cornerstone of modern estate planning.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Apple remains a compelling long-term investment, thanks to its robust ecosystem, accelerating AI strategy, and disciplined capital returns.

🏛️ Reliable Business Model & Ecosystem Moat

Apple now supports over 2.3 billion active devices, forming one of the most durable customer ecosystems in tech. This massive footprint reinforces high switching costs and recurring revenue streams via services like the App Store, Apple Pay, and suite of subscriptions (now over 38% of gross profit) (Forbes). Its strategy of integrating hardware, software, and services creates a differentiation moat that’s hard to replicate.

🚀 Catalysts Behind Future Growth

▪ Apple Intelligence: A Privacy-First AI Pivot

At WWDC 2025, Apple unveiled its “Apple Intelligence” initiative—20+ AI-powered features like real-time translation and email summarization designed for on-device performance and privacy. A major upgrade to Siri is expected in 2026. While it’s lagging peers in sheer AI spend, Apple is now investing aggressively and open to strategic M&A, having acquired at least seven AI startups in 2025..

▪ iPhone Refresh Cycles & Hardware Upside

Morgan Stanley projects a 12% rebound in iPhone shipments by fiscal 2026 as AI features boost upgrade demand. The favorable reception to new iPhone 16 models ahead of the holiday season supports this optimistic view (marketwatch.com).

🌍 Strategic Resilience Amid Geopolitical Risks

Apple’s architecture strategy includes over $500 billion in U.S. investment over four years—from expanding chip-making capacity to creating manufacturing academies and AI server production facilities to help offset tariff risks. At the same time, it has shifted much iPhone production for U.S. markets to India, diversifying supply chain risk away from China.

💰 Financial Strength & Shareholder Returns

Apple posted $94 billion in Q3 2025 revenue—a 10% year-over-year gain—and services revenue reached a record $27.4 billion. EPS came in above expectations, and despite $800 million+ in tariff impacts, Apple demonstrated operational resilience.

It continues to return capital aggressively, with $15.2 billion paid in dividends in 2025 and a long-term track record of dividend increases and share repurchases. Analysts expect this capital discipline to endure, offering downside protection and steady income (The Motley FoolForbes).

📉 Valuation: Discount with Upside Potential

Despite its strengths, Apple is currently down roughly 20% year-to-date, underperforming other major tech names amid tariff fears, AI lags, and macro uncertainty (Business Insider). Its forward P/E sits at around 33.6×, above the S&P 500 average (~23×), making valuation relative to its growth prospects a mixed story (Forbes). Still, analysts at BofA, Goldman Sachs, Wedbush, and others issue “Buy” ratings with 12–18 month targets of $235–300, implying double-digit upside from today’s ~$200 price levels.

🧭 Risks to Watch

While Apple’s fundamentals remain solid, investors should monitor:

Delays or execution risk in AI deployment or acquisitions

Regulatory scrutiny around antitrust, App Store rules, and global expansion

U.S.–China relations and implications for supply chain resilience

📈 Final Verdict: Long-Term Buy, Tactical Caution

Apple’s dominant ecosystem, balanced growth from hardware and high-margin services, disciplined capital returns, and accelerated AI pivot position it as a long-term winner. While near-term volatility and tariff uncertainty add caution, the current valuation discount provides an attractive entry point for investors with a multiyear horizon.

Disclosure:

I do not own any stock or have any financial interest in Apple Inc. (NYSE: AAPL). This article is for informational purposes only and should not be considered financial or investment advice. Investing in stocks carries risks, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

Finding balance between work and family has been one of the biggest challenges- and greatest lessons- of my life. For a long time, I thought I could achieve some magical state where everything stayed perfectly organized and everyone’s needs were met without any hiccups. I quickly learned that life doesn’t work that way. What I’ve discovered instead is that balance is a daily choice, a constant practice, and a mindset that helps me stay grounded when life gets messy.

It starts with being honest about my priorities. I know there will always be more emails to answer, calls to return, and projects to complete. But my family only gets one version of me-and I want that version to be fully present. That’s why I carve out dedicated time on my calendar for family dinners, school events, and quiet evenings at home. I block those moments off the same way I would for an important meeting with a client because, to me, they’re just as important.

Another thing that helps is clear and open communication. I talk to my family about my work schedule, and I keep my team at work updated on my family commitments. When everyone’s on the same page, it’s easier to manage expectations and avoid unnecessary stress. I’ve learned that it’s okay to ask for help or to say “no” when my plate is too full. It doesn’t make me any less dedicated-it just makes me human.

I also try to protect small moments for myself. These pockets of time-like enjoying my morning coffee before anyone else is awake, squeezing in a quick workout, or reading a few pages of a book before bed-give me the energy to show up for both work and family. I’ve found that when I neglect my own needs, it catches up with me fast. Self-care isn’t selfish; it’s essential.

Flexibility is another big piece of the puzzle. Some days, work will demand more of my time. Other days, family emergencies or milestones take priority. Instead of getting frustrated when plans change, I remind myself that balance isn’t about splitting my time evenly every day-it’s about adjusting as life unfolds. I try to be kind to myself when things don’t go perfectly.

Finding balance will always be a moving target for me, but over time, I’ve gotten better at recognizing what works and what doesn’t. I’ve stopped trying to do it all at once. Instead, I focus on being fully present wherever I am-whether I’m leading a meeting, helping with homework, or just laughing around the dinner table.

In the end, my biggest takeaway is that balance doesn’t come from rigid rules-it comes from giving myself grace, staying flexible, and remembering what matters most. And as long as I keep showing up for both my work and my family with intention and love, I know I’m doing something right.

As temperatures rise and backyard grills fire up, summer is often synonymous with indulgent foods from ice cream cones and cheeseburgers to sugary cocktails and deep-fried fair treats. But this year, health-conscious eaters are proving that you don’t have to sacrifice flavor to stay on track with your wellness goals.

Nutritionists and chefs alike are championing simple food swaps that cut down on calories and saturated fat, boost nutrients, and still deliver the mouthwatering taste people crave during the sunny season.

Frozen Yogurt Over Ice Cream Swap out sugar-laden ice cream for creamy Greek frozen yogurt. It satisfies that sweet tooth while packing in protein and probiotics that aid digestion — a win-win after a heavy BBQ meal.

Grilled Veggies Instead of Chips Potato chips are a picnic staple, but grilled veggies like zucchini, bell peppers, and eggplant are quickly taking over summer spreads. Tossed with olive oil and herbs, they’re crisp, colorful, and bursting with flavor — minus the trans fats and sodium overload.

Turkey or Veggie Burgers in Place of Beef Summer cookouts and burgers go hand in hand, but swapping a fatty beef patty for a lean turkey or plant-based burger reduces saturated fat without skimping on the smoky taste. Pile it high with fresh greens and tomatoes for added crunch and nutrients.

Infused Water Beats Soda Sugary sodas and sweet teas can derail a healthy summer day fast. Instead, stay hydrated with naturally flavored water. Add fresh berries, cucumber slices, or mint to your pitcher — it’s refreshing, festive, and free of empty calories.

Nice Cream for Dessert Banana “nice cream” is trending for good reason: blend frozen bananas with a splash of almond milk, and you’ve got a creamy, dairy-free dessert that rivals traditional soft serve — without the sugar crash.

Fresh Fruit Kabobs Instead of Candy Summer means peak season for juicy fruits like watermelon, pineapple, and strawberries. Thread them onto skewers for colorful, fun-to-eat kabobs that beat processed sweets and satisfy a sugar craving naturally.

Whole-Wheat Buns and Wraps For those summer sandwiches and hot dogs, opt for whole-wheat buns or lettuce wraps. You’ll up your fiber intake and avoid the blood sugar spikes that come with refined white bread.

These swaps aren’t about deprivation they’re about finding creative ways to celebrate the season’s best flavors while giving your body what it needs to feel its best.

So, whether you’re hosting a backyard barbecue or packing a picnic for the beach, try one (or all) of these healthy swaps and taste how satisfying smart choices can be.

What’s your favorite healthy summer swap? Let us know in the comments!

As Americans continue to grapple with economic uncertainty, rising living costs, and increasing life expectancy, the importance of retirement planning has never been more pressing. One of the biggest debates among financial experts and everyday workers alike is this: Is it better to start saving early, or can a late start still lead to a secure retirement?

The Power of Starting Early Financial advisors almost universally agree—when it comes to retirement, time is your greatest asset. Starting in your 20s or early 30s allows compound interest to work its magic.

Take, for example, a 25-year-old who invests $300 a month in a retirement account with an average annual return of 7%. By the time they turn 65, they could accumulate nearly $725,000. On the other hand, someone who begins investing the same amount at age 40 would end up with just over $225,000 at retirement.

“Starting early doesn’t just mean you’ll have more saved—it also means you can afford to take less risk, contribute less monthly, and still enjoy financial freedom later,” says Michelle Harris, a certified financial planner in Chicago.

Early starters also have the advantage of weathering market volatility. They have decades to recover from downturns, allowing for a more aggressive, growth-oriented investment approach early on.

The Challenges—and Hope—of Starting Late Still, not everyone has the means or knowledge to begin saving in their 20s. Life events such as student debt, low-paying jobs, or unexpected medical expenses can push retirement planning to the back burner.

“If you’re starting in your 40s or even 50s, the hill is steeper, but it’s not insurmountable,” says Tony Kim, a retirement strategist based in San Diego. “The key is discipline, increased contributions, and possibly working a bit longer.”

Late starters are often advised to max out retirement accounts like 401(k)s and IRAs, take advantage of catch-up contributions (available to those 50 and older), and consider delaying Social Security benefits to increase monthly payouts.

Financial experts also emphasize the importance of budgeting, eliminating debt, and making intentional lifestyle choices to accelerate savings.

A Matter of Mindset Whether you start at 25 or 55, the most important step is simply to start. Procrastination is often the biggest enemy of retirement planning.

“Too many people think they have time or that it’s too late,” says Harris. “Both beliefs are harmful. The sooner you face your financial future, the better your options will be.”

Retirement planning is not a one-size-fits-all journey. Starting early gives investors more flexibility and freedom, but starting late doesn’t mean the game is over. With the right strategy, discipline, and mindset, it’s possible to secure a comfortable retirement at any age.

About the Author:

David Dandaneau is a insurance agent that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

The cryptocurrency market continues to evolve, with new projects constantly emerging that aim to redefine finance. One such project making waves is ONDO Finance. This innovative platform bridges traditional finance with decentralized finance (DeFi), providing investors with unique opportunities to gain exposure to real-world assets on the blockchain.

What is ONDO Finance? ONDO Finance is a decentralized finance protocol that focuses on tokenizing traditional financial assets, such as bonds, treasury securities, and other stable investments. By leveraging blockchain technology, ONDO Finance offers transparency, security, and ease of access to investors seeking diversified income streams.

The ONDO token is the platform’s utility and governance token, allowing holders to participate in decision-making processes, earn rewards, and access exclusive investment opportunities.

Why is ONDO Finance Gaining Attention?

Real-World Asset Integration: ONDO Finance bridges traditional finance with crypto by tokenizing real-world assets. This unique model offers stability and predictable returns, attracting risk-averse investors seeking consistent yields.

Transparency and Security: Blockchain technology ensures that all transactions are recorded and verifiable, reducing fraud risk and enhancing trust among investors.

Yield Opportunities: ONDO Finance offers structured investment products designed to maximize returns, making it an attractive platform for both retail and institutional investors.

Institutional Partnerships: The project has forged partnerships with major financial institutions, reinforcing its credibility and growth potential.

DeFi Growth Potential: As DeFi continues to expand, platforms like ONDO Finance that focus on real-world asset integration are poised for strong growth.

Investment Considerations While ONDO Finance presents an exciting opportunity, potential investors should be mindful of the risks inherent to the crypto market. Market volatility, regulatory changes, and platform-specific risks should be carefully considered. Conducting thorough research and diversifying investments is crucial.

ONDO Finance is emerging as a significant player in the crypto landscape by combining traditional finance stability with blockchain innovation. For investors seeking exposure to real-world assets with the added benefits of DeFi, ONDO Finance may offer a promising avenue for growth. However, as with any investment, due diligence is key to making informed decisions.

Disclaimer: The author holds a position in ONDO Finance and this article should not be considered financial advice. Always conduct your own research before making any investment decisions.