Planning for retirement isn’t something that should wait until your final working years. One of the smartest steps you can take today “no matter your age” is estimating your future Social Security benefits. Understanding these numbers early helps you make more informed financial decisions, set realistic expectations, and build a roadmap toward a more secure retirement.

Why Estimating Your Benefits Early Matters

1. It Helps You Understand How Much You’ll Actually Need Many Americans overestimate how much Social Security will provide. By checking your personalized benefit estimate now, you can see whether your projected income will cover your essential expenses—and how much more you may need to save.

2. You Can Adjust Your Savings Strategy Ahead of Time If your estimated monthly benefit is lower than expected, learning this early gives you years—even decades—to increase your contributions to a 401(k), IRA, or other retirement vehicles.

3. It Highlights the Value of Working Longer Your Social Security payout is based on your highest 35 years of earnings. Seeing your estimate can motivate you to improve your earnings record or reduce low-income years, increasing your benefit when retirement finally comes.

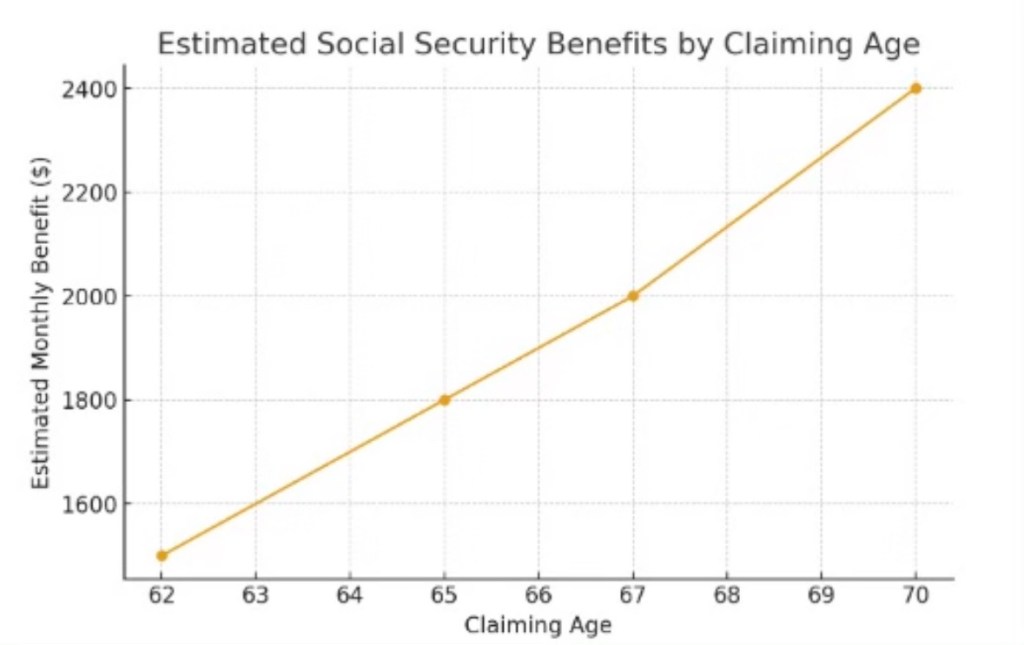

4. Claiming Age Makes a Huge Difference Whether you claim at 62, 67, or 70 dramatically changes your monthly income. Understanding this now helps you plan the right claiming strategy for your lifestyle and goals.

Estimated Social Security Benefits by Claiming Age

Below is a chart illustrating how estimated monthly benefits generally increase the longer you delay claiming:

How to Estimate Your Benefits Today

You can access your personalized estimate at any age by creating or logging into your mySocialSecurity account at SSA.gov. Once inside, you’ll see:

Your projected monthly benefit at age 62

Your full retirement age (typically 67)

Your estimated benefit at age 70

Your complete earnings record

Taking a few minutes to review this information now can help you avoid surprises later and give you the confidence to build a stronger retirement strategy.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As more Americans approach retirement, many are finding that the path to a secure and fulfilling post-work life is more complex than they expected. While saving money is an important first step, a successful retirement hinges on avoiding common pitfalls that can derail even the most carefully built plans. Here are some of the most frequent retirement traps—and smarter strategies to consider instead.

Trap 1: Relying Too Heavily on Social Security

Many retirees assume Social Security will replace most of their income, only to discover their benefits cover far less than expected. With the average monthly benefit hovering around modest levels, relying on Social Security alone can put retirees at risk of falling behind rising costs of living and healthcare expenses.

A smarter alternative: Build a layered income plan that includes Social Security, retirement accounts like 401(k)s or IRAs, pensions (if available), and supplemental income sources. Consider part-time work or consulting if feasible. The key is diversifying your income streams so one isn’t carrying the entire load.

Trap 2: Underestimating Healthcare Costs

Healthcare is one of the biggest retirement expenses, and Medicare doesn’t cover everything. Many retirees are shocked by premiums, deductibles, dental costs, and long-term care needs.

A smarter alternative: Plan early. Look into long-term care insurance or hybrid life-insurance policies with LTC riders. Create a dedicated healthcare fund within your retirement savings. And don’t overlook supplemental Medicare plans that can greatly reduce out-of-pocket expenses.

Trap 3: Cashing Out Retirement Accounts Too Early

Taking large withdrawals early in retirement—especially before age 59½—can trigger steep taxes and penalties, diminishing your long-term nest egg. Even after that age, withdrawing too aggressively can make savings run out sooner than expected.

A smarter alternative: Use a structured withdrawal plan, such as the 4% rule or dynamic withdrawal strategies that adjust based on market performance. Pair withdrawals with tax-efficient strategies like Roth conversions before RMD age to reduce future tax burdens.

Trap 4: Failing to Account for Inflation

Inflation has made a fierce comeback in recent years. Retirees with fixed incomes or overly conservative portfolios risk losing purchasing power over time.

A smarter alternative: Include growth investments—like diversified stock funds—even in retirement, to stay ahead of inflation. Treasury Inflation-Protected Securities (TIPS) and annuities that offer inflation adjustments can also provide peace of mind.

Trap 5: Overlooking Housing Costs

Many retirees assume their housing expenses will drop once the mortgage is gone, but property taxes, insurance, and maintenance continue—and often increase.

A smarter alternative: Evaluate your housing situation realistically. Downsizing, relocating to a lower-cost area, or exploring 55+ communities may reduce expenses. Some retirees also use a portion of home equity strategically through downsizing or a Home Equity Conversion Mortgage (HECM) as part of their financial plan.

Trap 6: Not Preparing Emotionally for Retirement

Retirement isn’t just a financial transition—it’s a lifestyle change. Without structure, purpose, or social engagement, many retirees face loneliness, boredom, or even depression.

A smarter alternative: Design your retirement life as intentionally as your financial strategy. Volunteer, join clubs, take classes, or explore part-time work in a field you enjoy. Staying mentally and socially active is essential for long-term well-being.

Smart Alternatives for Soon-to-Be and Current Retirees

Beyond avoiding traps, here are simple, proactive steps that make retirement more stable and satisfying:

Create a retirement income roadmap that outlines exactly where your money will come from and how long it should last.

Meet with a financial professional to stress-test your plan against inflation, market downturns, and health surprises.

Diversify income, including predictable sources like annuities, rental income, dividends, or guaranteed pension payouts.

Stay flexible—your retirement plan should evolve as life, health, and markets change.

Review your insurance coverage, including life, home, auto, and long-term care, to ensure you’re protected.

Stay active and engaged, both socially and physically, to support overall happiness and health.

Long and Short

Retirement doesn’t have to be uncertain. By steering clear of common traps and embracing a well-rounded financial and lifestyle strategy, retirees can build a future that’s not only secure—but rewarding. With thoughtful planning and the right support, this next chapter can be the best one yet.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Cohen & Steers Infrastructure Fund, Inc. (ticker: UTF) is a closed-end fund that invests primarily in listed infrastructure companies utilities, pipelines, toll roads, telecoms and similar businesses with an emphasis on income and total return. The fund targets at least 80% exposure to infrastructure securities and is permitted to hold preferreds and fixed-income as well. (Cohen & Steers+1)

The case for UTF in a downturn

High and steady monthly distribution. UTF pays a monthly cash distribution (recently about $0.155 per share) that translates to a forward annualized dividend around the high-single to mid-single digits (roughly a 7–8% yield at current market prices). That regular payout can make UTF attractive to income-seeking investors during equity market weakness. (Cohen & Steers Resources+1)

Defensive underlying exposure. Infrastructure companies often provide essential services (power, water, roads, telecom) with relatively stable cash flows and regulatory protections that can soften downside in economic contractions compared with cyclical sectors. UTF’s strategy explicitly focuses on these companies and includes income-oriented holdings (common equity plus a portion in preferreds/fixed income). (SEC+1)

Closed-end structure can add opportunity. As a closed-end fund, UTF can trade at a premium or discount to net asset value (NAV) and use leverage or share repurchases to enhance returns. In downturns, discounts can widen and create potential buying opportunities for investors seeking yield and income—though discounts can also persist. Recent fund documents show management tools (repurchase programs, rights offerings) are in use when needed. (Cohen & Steers+1)

Relative price stability historically. While all market securities fall in tough selloffs, UTF’s share price history shows less extreme volatility than many small-cap or tech names because of its income focus and infrastructure holdings. (See sources below for historical price and distribution history.) (Yahoo Finance+1)

Total-return potential from dividends + capital. In a downturn the regular dividend cushions total returns. If the portfolio’s underlying cash flows remain intact, the dividend can provide an attractive yield while capital recoveries occur — particularly for buy-and-hold income investors.

Risks you must weigh

Discount/premium risk: CEFs can trade at large, persistent discounts to NAV; the market price might not reflect NAV recovery quickly. (CEF Connect)

Leverage and interest-rate sensitivity: Some closed-end funds use leverage that can magnify losses when markets fall and can increase sensitivity to rising rates. UTF’s prospectus and factsheet discuss leverage and fixed-income exposure. (Cohen & Steers Resources+1)

Concentration risk: Heavy exposure to infrastructure and related subsectors means sector-specific shocks (regulatory, energy shocks, etc.) can hit performance. (SEC)

Analysts don’t always publish a single consensus price target for closed-end funds like UTF; where a consensus target isn’t available, a scenario approach is often more informative. Below I created three plausible projected price scenarios for the next 12 months — Bear (–15% y), Baseline (+4% y) and Bull (+25% y) — starting from the recent market close (~$24.20). These are illustrative projections (not predictions or investment advice), intended to show how price paths and total return dynamics might look under different macro/backdrop outcomes.

Key assumptions used for the chart: start price $24.20, monthly compounding equivalent to the annual scenario rates listed above. These scenarios do not include dividends — they show market-price outcomes only (adding dividends would materially improve total returns, especially at a ~7–8% yield).

Quick takeaways

UTF’s monthly dividend and exposure to essential infrastructure make it a reasonable consideration for income-focused investors during market downturns; the dividend can provide cashflow support while equity markets recover. (Cohen & Steers Resources+1)

However, because UTF is a closed-end fund, price movements can diverge from underlying NAV and be influenced by fund-specific factors (discounts, leverage, corporate actions). That tradeoff (high yield vs. structural CEF risks) is central to whether UTF is appropriate for any individual portfolio. (Cohen & Steers+1)

Disclosure

I currently hold a position in the Cohen & Steers Infrastructure Fund (UTF). This information is provided for educational and informational purposes only and should not be considered financial advice. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

DividendMax. (n.d.). Cohen & Steers Infrastructure Fund dividend information. Retrieved from https://www.dividendmax.com/

SEC. (n.d.). Cohen & Steers Infrastructure Fund, Inc. (UTF) — Prospectus & filings. U.S. Securities and Exchange Commission. Retrieved from https://www.sec.gov/

StockAnalysis.com. (n.d.). UTF: Cohen & Steers Infrastructure Fund stock dividend & history. Retrieved from https://stockanalysis.com/

Yahoo Finance. (n.d.). UTF — Cohen & Steers Infrastructure Fund price & chart data. Retrieved from https://finance.yahoo.com/

When it comes to building wealth, most families focus on earning, saving, and investing. Yet one of the most overlooked parts of financial planning happens at the end of the journey: preparing the next generation to handle what’s left behind. Experts warn that simply passing down money—without communication or financial education—can lead to confusion, conflict, and costly mistakes.

A recent study by multiple wealth-management groups found that nearly 70% of inherited wealth is lost by the second generation, and 90% is gone by the third. The cause isn’t the financial markets—it’s a lack of preparation. When heirs are suddenly handed assets, properties, or cash with little context, they may mismanage the money, disagree with each other, or unintentionally make tax-heavy decisions.

Why Preparation Matters

Inheritance isn’t just about money—it’s about clarity and continuity. When families don’t talk about what’s being passed down, heirs often must make high-pressure decisions during periods of grief. Without a roadmap, even well-intentioned children or beneficiaries may disagree on how to handle a home, manage investments, or split proceeds.

And the stakes are rising. As Baby Boomers pass on an estimated $84 trillion over the next two decades, families who fail to prepare run the risk of watching generational wealth disappear.

Communication Is the First Step

Open dialogue ensures everyone understands what exists, where it is, who gets what, and—equally important—why. These conversations take the mystery out of money and help heirs feel responsible, not overwhelmed.

Good communication also reduces legal challenges, sibling tension, and last-minute surprises. Beneficiaries who know the plan ahead of time make smarter choices because they’re not operating in the dark.

Teach Financial Know-How Before It’s Needed

Even the best inheritance plan can fall apart if heirs don’t know how to manage money. Families should consider sharing basic financial skills: how taxes on inheritance work, the risks of cashing out investments too quickly, how to evaluate insurance needs, and how to make a long-term plan.

Working with a financial advisor, estate attorney, or tax professional can also give heirs a clear framework to manage their new responsibilities confidently.

Table: Smart Ways to Pass Down Inheritance

Method

What It Is

Best Use Case

Key Benefits

Potential Pitfalls

Will

Legal document stating who receives assets

Straightforward asset distribution

Simple, inexpensive, widely recognized

Can go through probate; may be challenged

Revocable Living Trust

A trust you control during your lifetime

Avoiding probate and ensuring smooth transfer

Faster distribution, more privacy, flexible

Requires proper funding; setup cost

Beneficiary Designations

Named beneficiaries on accounts (401k, life insurance, IRAs)

Retirement and insurance assets

Bypasses probate, easy to update

Conflicts with wills if not aligned

Gifting During Lifetime

Giving money or assets while alive

Reducing estate taxes; preparing heirs early

Lets heirs learn with guidance; tax advantages

Annual gift limits; may impact your retirement

Family Meetings

Regular discussions about assets and plans

Multi-heir families; complex estates

Reduces conflict, sets expectations

Requires openness; emotional topics

Financial Education for Heirs

Teaching heirs money skills before they inherit

Any family wanting generational wealth

Builds confidence and reduces mistakes

Time investment; requires ongoing support

Insurance Policies

Using life insurance to create liquidity

When heirs need cash to pay taxes or debts

Predictable payout; avoids asset liquidation

Premium costs; needs proper planning

Professional Advisors

Attorneys, financial planners, tax pros

Significant or complex estates

Expert guidance, reduced errors

Costs vary; choose reputable advisors

To Sum Up

In the end, passing down wealth isn’t just about assets—it’s about equipping the next generation to use those assets wisely. By communicating openly, planning thoughtfully, and preparing heirs with real financial understanding, families can protect their legacy and ensure their hard work continues to make a positive impact for years to come.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Life is full of transitions—whether it’s buying your first home, changing careers, starting a family, or preparing for retirement. While these moments bring opportunity and excitement, they can also create uncertainty and stress. The good news: with proactive planning and professional guidance, individuals can navigate these turning points with greater confidence and clarity.

“Transitions can feel overwhelming because they often involve financial, emotional, and lifestyle changes all at once,” says certified financial planner Jenna Morales. “Having a plan and a professional partner to guide you helps you make informed decisions rather than emotional ones.”

The Power of Planning Ahead

Proactive planning means thinking ahead—mapping out potential outcomes and creating strategies that align with your long-term goals. It’s not about predicting the future but preparing for it. Whether you’re moving to a new city, managing an inheritance, or downsizing in retirement, foresight helps reduce risk and stress.

Professional advisors, from financial planners to insurance agents and career coaches, can offer valuable expertise to help identify blind spots and opportunities. They can also act as objective voices when emotions run high, ensuring you stay focused on your priorities.

Top Tips for Navigating Major Life Transitions

Start Early: Begin planning before the change happens. The earlier you prepare, the more control you’ll have over your options.

Clarify Your Goals: Define what success looks like for you—financially, emotionally, and personally.

Seek Professional Advice: Don’t go it alone. Certified experts can provide insights and structure your plan for maximum benefit.

Review Your Insurance and Finances: Major changes often affect your coverage needs and cash flow. Make sure your policies and budget reflect your new circumstances.

Build a Safety Net: Set aside emergency savings to cushion unexpected costs during transitions.

Stay Organized: Keep key documents—such as wills, policies, and financial records—accessible and updated.

Adjust as You Go: Life plans are not one-size-fits-all. Revisit and revise your strategy regularly as your needs evolve.

Focus on Mental Well-Being: Change can be stressful. Prioritize self-care and seek support when needed.

Moving Forward with Confidence

While no one can avoid life’s major transitions, being proactive and seeking professional guidance can transform uncertainty into opportunity. It’s about taking control of what you can—and having trusted experts help you navigate what you can’t.

“Confidence comes from preparation,” Morales adds. “When you plan ahead and surround yourself with knowledgeable support, you move forward not with fear—but with clarity.”

When it comes to homeowners insurance, accuracy is everything. One of the most critical tools used to protect your biggest investment is the Replacement Cost Estimator (RCE)—a system that helps determine how much it would actually cost to rebuild your home from the ground up after a covered loss. Unfortunately, many homeowners underestimate their home’s true value, leading to painful surprises when disaster strikes.

The RCE takes into account today’s construction costs, materials, labor, and local building codes to calculate an accurate rebuilding cost—not the market price of your home. With inflation in construction and fluctuating material prices, relying on outdated or ballpark figures can leave you dangerously underinsured. If your policy doesn’t reflect your home’s current replacement cost, you could end up paying tens—or even hundreds—of thousands—out of pocket after a total loss.

It’s not just the structure that matters. Personal property coverage—the protection for your belongings like furniture, electronics, and clothing—should also reflect their true replacement value. Too often, people underestimate what it would take to replace everything they own. And don’t overlook loss of use coverage, which helps pay for temporary housing and living expenses if your home becomes uninhabitable. Skimping on this area could make a tough situation even harder if you’re displaced for months during repairs.

The bottom line: an accurate RCE ensures your dwelling, personal property, and loss of use coverages keep pace with reality. Take time to review your policy annually, ask your agent to update your RCE, and avoid the false comfort of being “covered” for less than what you’d actually need. When life’s unexpected moments happen, being properly insured is what helps you rebuild—not just your home, but your peace of mind.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As retirement approaches, one of the biggest financial questions homeowners face is whether to pay off their mortgage early or hold on to the cash for flexibility and investments. Both paths have strong arguments, and the right choice often depends on your personal goals, financial stability, and tolerance for risk.

🔹 The Case for Paying Off Your Mortgage

1. Peace of Mind and Lower Expenses Eliminating your mortgage before retirement means you’ll enter your golden years without one of your biggest monthly bills. This can bring enormous peace of mind—especially for retirees living on a fixed income. Without a mortgage, your monthly expenses drop dramatically, making it easier to stretch your retirement savings further.

2. Guaranteed Return on Investment Paying off your mortgage is like earning a “risk-free” return equal to your interest rate. For example, if your mortgage rate is 6%, you’re effectively earning a guaranteed 6% return by eliminating that debt—a tough benchmark for low-risk investments to match.

3. Emotional and Financial Freedom Many homeowners simply like the feeling of owning their home outright. It provides a sense of security knowing that, no matter what happens to the market or the economy, you have a paid-off place to live.

🔸 The Case for Keeping the Mortgage and Saving the Cash

1. Liquidity and Flexibility Once you pay off your mortgage, that cash is locked into your home’s equity. While you can access it through a home equity line or reverse mortgage, those options can be costly or hard to qualify for in retirement. Keeping cash in savings or investments gives you flexibility for emergencies, healthcare costs, or opportunities.

2. Potential for Higher Returns If your mortgage rate is relatively low—say, under 4%—you might earn more by investing your money instead of paying off the loan. Historically, diversified portfolios have returned more than typical mortgage rates over the long term, allowing your wealth to grow faster while you continue making manageable payments.

3. Tax and Inflation Advantages For some retirees, mortgage interest may still be tax-deductible, reducing overall borrowing costs. Additionally, with inflation, the real value of your fixed mortgage payments decreases over time—meaning you’re repaying the loan with “cheaper” dollars in the future.

⚖️ Finding the Right Balance

Many experts suggest a hybrid strategy:

Pay down your mortgage enough to feel comfortable with the lower balance and payments.

Keep a healthy cash reserve or investment portfolio for flexibility.

Ultimately, the best choice depends on your individual circumstances—your mortgage rate, your savings, your risk tolerance, and how much you value financial security versus potential growth.

🧭 Final Thought

There’s no one-size-fits-all answer. The “right” move is the one that helps you sleep well at night, knowing your finances are positioned to support your lifestyle and goals. Whether that means living debt-free or keeping your investments working, it’s about creating a retirement plan that gives you confidence, comfort, and control.

When it comes to homeowners insurance, most people focus on protecting their property from fire, theft, or storm damage. But one of the most overlooked—and most important—aspects of your policy is liability coverage. This protection kicks in when someone is injured on your property or if you accidentally cause damage to someone else’s property. And if you’re hiring contractors to work on your home, ensuring they’re properly insured could save you from financial disaster.

Understanding Liability Limits

Every homeowners insurance policy includes personal liability coverage, typically starting around $100,000 but often ranging up to $500,000 or more. This coverage helps pay for medical bills, legal fees, and settlements if you’re found responsible for an injury or property damage.

For example, if a guest slips on your icy driveway or a tree from your yard damages your neighbor’s fence, your liability coverage helps cover those costs. But here’s the catch—if damages exceed your policy limit, you’re personally responsible for the rest.

That’s why many insurance professionals recommend reviewing your limits regularly and considering an umbrella policy for extra protection. An umbrella policy can provide an additional $1 million or more in liability coverage for a relatively small cost each year.

The Hidden Risk of Uninsured Contractors

Home improvement projects often involve hiring outside help—roofers, electricians, painters, or landscapers. But before you hand over the keys or cut that first check, it’s critical to make sure any contractor working on your property carries their own liability and workers’ compensation insurance.

If a contractor is uninsured and one of their workers gets hurt on your property, you could be held liable for medical expenses, lost wages, or even lawsuits. Similarly, if they accidentally damage your home or a neighbor’s property, and they’re not covered, your own insurance might have to step in—potentially driving up your premiums or leaving you with out-of-pocket costs.

Protecting Yourself and Your Investment

Your homeowners insurance does more than protect your house—it protects your financial future. By maintaining sufficient liability limits and ensuring contractors are properly insured, you can avoid costly surprises if something goes wrong. A few minutes of due diligence today can save you thousands—and a lot of stress—tomorrow.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

TAMPA – October 21, 2025 — The brokerage and trading-platform firm Webull Corporation (ticker BULL) finds itself trading near multi-year lows. For value-oriented investors, that raises a classic question: Is this a moment of opportunity, or a warning that things are worse than they appear?

Here’s what investors need to know:

1. The Case For: Potential Upside From a Low Base

Webull reported strong top-line growth in recent quarters. In Q1 2025, revenues rose by 32 % year-over-year to about US$117 million, and the company swung from a loss to a net income of around US$12.9 million. (PR Newswire+2StockAnalysis+2)

In Q2 2025, revenue came in at roughly US$131.5 million, up ~46 % vs Q2 2024 (~US$90.1 million) — showing accelerating growth in that period. (Investing.com+2WallStreetZen+2)

The stock has already fallen steeply from its earlier highs. Some market commentary suggests that when a stock has dropped hard, it might set up for a rebound if fundamentals improve. (Value The Markets+1)

Webull’s business model—zero-commission trading, fractional shares, global expansion—remains relevant in the growing world of retail finance and digital investing. Supportive structural tailwinds could help long-term. For example, the company claims global reach and a broad user base. (AInvest+1)

2. The Case Against: Key Risks That Still Loom

While revenue is growing, the annual full-year revenue for 2024 was essentially flat compared to 2023 (~US$390.2 million in both years) — indicating growth isn’t guaranteed or smooth. (WallStreetZen+1)

Profitability remains a concern: Return on equity and profit margins are weak or negative in many recent periods. (Simply Wall St+1)

The company competes in a crowded sector (digital brokerages, fintech platforms) with strong incumbents like Robinhood Markets. Analysts have flagged slower growth vs bigger rivals. (Webull+1)

There are corporate-structure complexities and lock-up/share dilution risks. A financial-news piece noted that if the stock trades above US$12 for 20 days, up to 25 % of locked shares might be released, potentially expanding supply. (Money Morning)

3. Why “At All-Time Lows” Could Be a Turning Point

Many stocks trade at depressed levels because the market has lost confidence. That creates a scenario where:

The “bad news” may be largely baked into the price, so incremental positive surprises can have outsized impact.

A low base offers more upside potential if things go well (i.e., less downside cushion). For Webull, if growth continues and profitability improves, the market could reward the turnaround possibility. On the flip side, if risks intensify, the low price could still go lower.

4. What to Monitor Going Forward

Investors considering Webull should keep a close eye on:

Upcoming quarterly results: Are revenues continuing to grow at high rates? Are expenses under control?

Account growth and trading volume: How many active/funded accounts? What is customer asset growth?

Profit margins and net income: Are they trending toward consistent profitability?

Share-count / dilution risk: Are there significant new shares coming? Are previously locked shares being released?

Competitive dynamics and regulatory risks: Any new regulatory headwinds? How is Webull distinguishing itself vs other brokers?

5. Summary: A High-Risk, High-Potential Setup

In short: Webull is not a safe, boring investment. It carries meaningful operational and structural risk. But the combination of decent recent growth, a depressed share price, and a business model aligned with retail investing trends makes it plausible that at these levels, the upside could be interesting if things go right.

For investors comfortable with risk and looking for speculative exposure in the fintech/brokerage space, BULL might offer a worthwhile “bet.” For more conservative investors, the uncertainty may be too large.

Before investing, one should do their own due diligence, weigh risk vs reward carefully, and consider how this fits into an overall portfolio.

Above: Representative charts showing (1) share-price path of Webull (BULL), (2) recent revenue growth, (3) user growth/expansion metrics.

Disclaimer

This is not financial advice. The information above is for educational and informational purposes only. Investing involves risks, including loss of principal. Always consult a qualified financial advisor regarding your specific situation.

For many homeowners, rising home values have created an opportunity to tap into their property’s equity — the difference between what you owe on your mortgage and what your home is worth. Using home equity can be a smart financial move, especially if you’re looking to pay off high-interest debt or fund major home improvements. But it’s not without risk.

Turning Equity Into Opportunity

Home equity loans and home equity lines of credit (HELOCs) allow you to borrow against the value of your home, often at lower interest rates than credit cards or personal loans. This can make them an appealing tool for consolidating high-interest debt, such as credit card balances that can quickly spiral out of control.

For example, replacing 25% interest credit card debt with a 7% home equity loan can save thousands in interest payments. Others use their home’s equity to finance renovations that can increase property value — like updating kitchens, adding energy-efficient systems, or finishing basements.

Understanding the Risks

While the benefits are clear, borrowing against your home’s equity comes with significant responsibilities. If you can’t make payments, you risk losing your home through foreclosure.

Home equity loans also increase your overall debt load, and if home prices fall, you could owe more than your property is worth — a situation known as being “underwater.” It’s also easy to fall into a debt cycle: paying off high-interest credit cards with a home loan only to run up balances again.

When It Makes Sense — and When It Doesn’t

Experts suggest using home equity strategically — for investments that add long-term value, like home improvements or education, not for short-term expenses or vacations. If you’re consolidating debt, make sure to address the spending habits that created it in the first place.

Before borrowing, compare rates, fees, and terms from multiple lenders, and consider talking to a financial advisor.

Key Takeaway

Home equity can be a valuable financial tool when used wisely — but it’s not “free money.” Every dollar you borrow is secured by the roof over your head. The best strategy is to borrow with purpose, have a clear repayment plan, and ensure the benefits outweigh the long-term costs.