TAMPA – October 21, 2025 — The brokerage and trading-platform firm Webull Corporation (ticker BULL) finds itself trading near multi-year lows. For value-oriented investors, that raises a classic question: Is this a moment of opportunity, or a warning that things are worse than they appear?

Here’s what investors need to know:

1. The Case For: Potential Upside From a Low Base

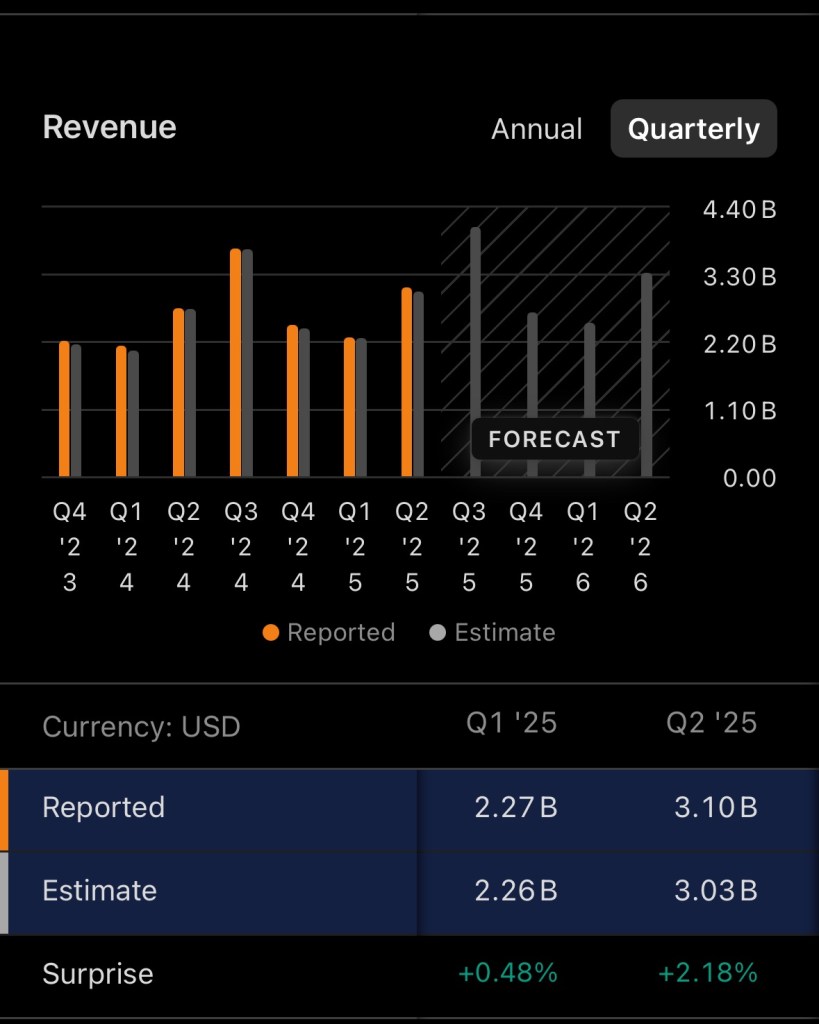

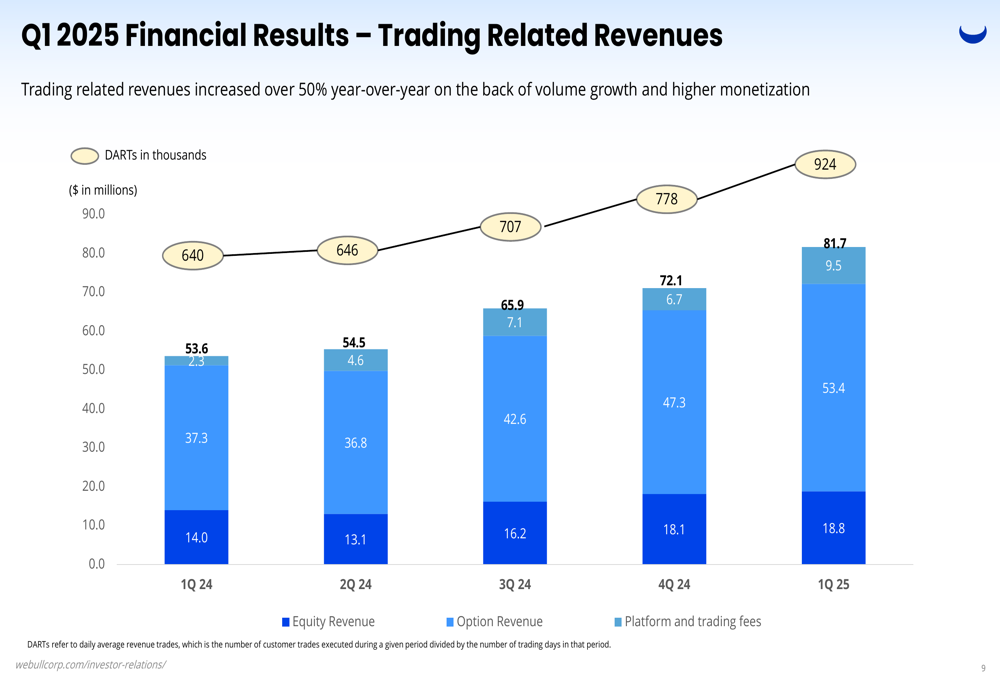

- Webull reported strong top-line growth in recent quarters. In Q1 2025, revenues rose by 32 % year-over-year to about US$117 million, and the company swung from a loss to a net income of around US$12.9 million. (PR Newswire+2StockAnalysis+2)

- In Q2 2025, revenue came in at roughly US$131.5 million, up ~46 % vs Q2 2024 (~US$90.1 million) — showing accelerating growth in that period. (Investing.com+2WallStreetZen+2)

- The stock has already fallen steeply from its earlier highs. Some market commentary suggests that when a stock has dropped hard, it might set up for a rebound if fundamentals improve. (Value The Markets+1)

- Webull’s business model—zero-commission trading, fractional shares, global expansion—remains relevant in the growing world of retail finance and digital investing. Supportive structural tailwinds could help long-term. For example, the company claims global reach and a broad user base. (AInvest+1)

2. The Case Against: Key Risks That Still Loom

- While revenue is growing, the annual full-year revenue for 2024 was essentially flat compared to 2023 (~US$390.2 million in both years) — indicating growth isn’t guaranteed or smooth. (WallStreetZen+1)

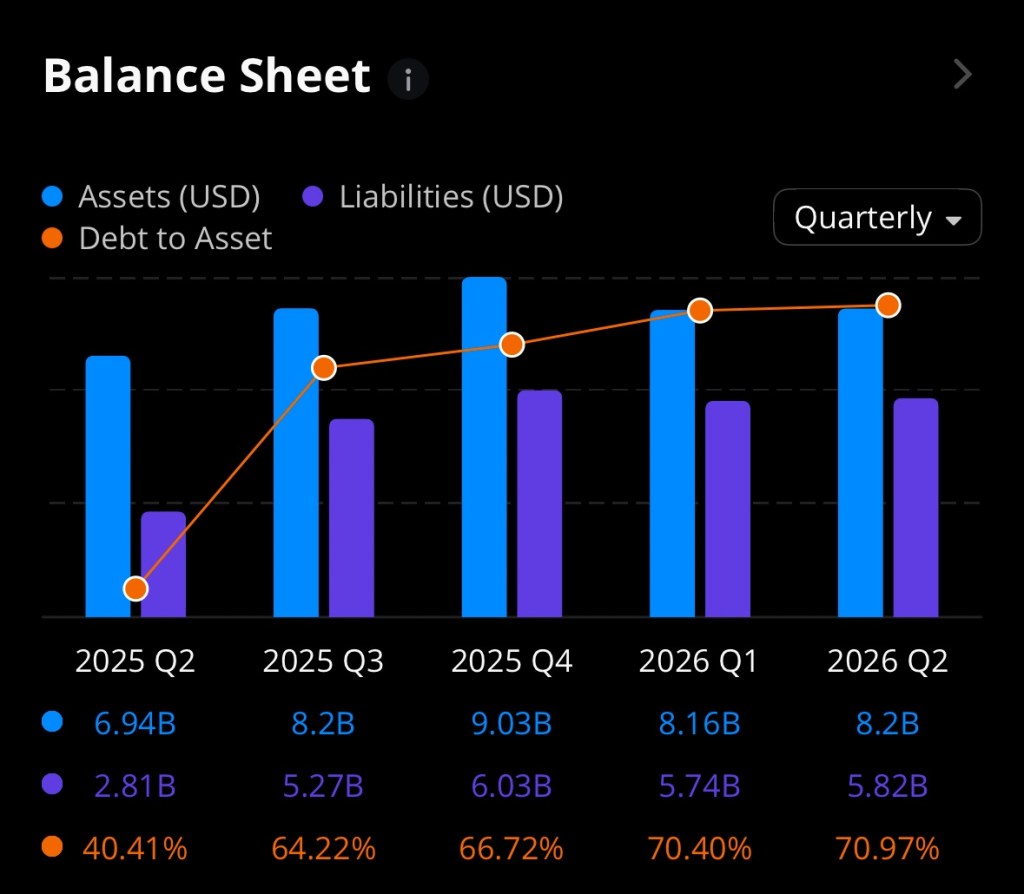

- Profitability remains a concern: Return on equity and profit margins are weak or negative in many recent periods. (Simply Wall St+1)

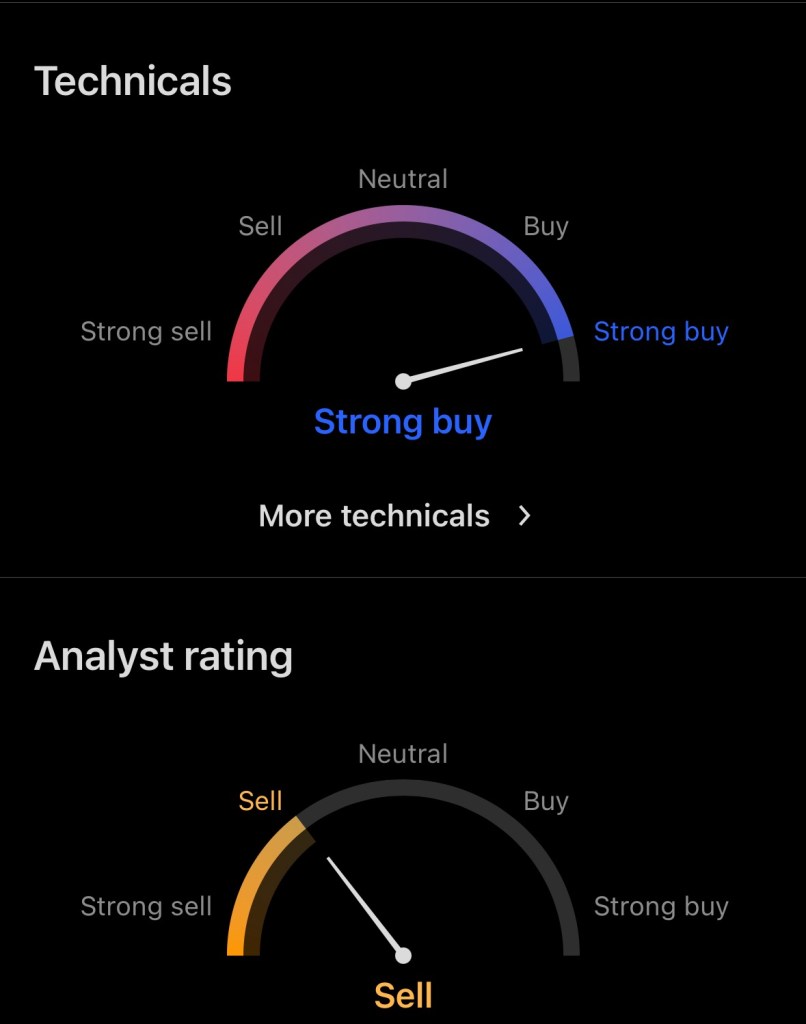

- The company competes in a crowded sector (digital brokerages, fintech platforms) with strong incumbents like Robinhood Markets. Analysts have flagged slower growth vs bigger rivals. (Webull+1)

- There are corporate-structure complexities and lock-up/share dilution risks. A financial-news piece noted that if the stock trades above US$12 for 20 days, up to 25 % of locked shares might be released, potentially expanding supply. (Money Morning)

3. Why “At All-Time Lows” Could Be a Turning Point

Many stocks trade at depressed levels because the market has lost confidence. That creates a scenario where:

- The “bad news” may be largely baked into the price, so incremental positive surprises can have outsized impact.

- A low base offers more upside potential if things go well (i.e., less downside cushion).

For Webull, if growth continues and profitability improves, the market could reward the turnaround possibility. On the flip side, if risks intensify, the low price could still go lower.

4. What to Monitor Going Forward

Investors considering Webull should keep a close eye on:

- Upcoming quarterly results: Are revenues continuing to grow at high rates? Are expenses under control?

- Account growth and trading volume: How many active/funded accounts? What is customer asset growth?

- Profit margins and net income: Are they trending toward consistent profitability?

- Share-count / dilution risk: Are there significant new shares coming? Are previously locked shares being released?

- Competitive dynamics and regulatory risks: Any new regulatory headwinds? How is Webull distinguishing itself vs other brokers?

5. Summary: A High-Risk, High-Potential Setup

In short: Webull is not a safe, boring investment. It carries meaningful operational and structural risk. But the combination of decent recent growth, a depressed share price, and a business model aligned with retail investing trends makes it plausible that at these levels, the upside could be interesting if things go right.

For investors comfortable with risk and looking for speculative exposure in the fintech/brokerage space, BULL might offer a worthwhile “bet.” For more conservative investors, the uncertainty may be too large.

Before investing, one should do their own due diligence, weigh risk vs reward carefully, and consider how this fits into an overall portfolio.

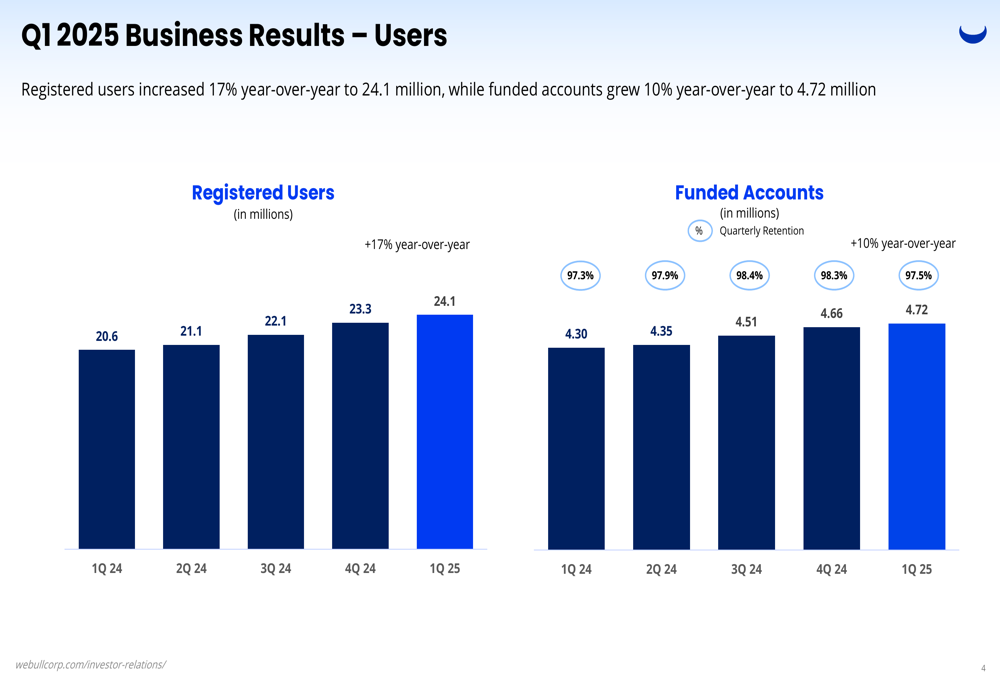

Above: Representative charts showing (1) share-price path of Webull (BULL), (2) recent revenue growth, (3) user growth/expansion metrics.

Disclaimer

This is not financial advice. The information above is for educational and informational purposes only. Investing involves risks, including loss of principal. Always consult a qualified financial advisor regarding your specific situation.

References

AINVEST. (2025, April 20). Webull stock: 2 reasons to buy, 4 reasons to sell. AINVEST.com. https://www.ainvest.com/news/webull-stock-2-reasons-buy-4-reasons-sell-2504-63/

Investing.com. (2025, August 8). Webull Q2 2025 slides: Revenue jumps 46%, achieves third profitable quarter. Investing.com. https://www.investing.com/news/company-news/webull-q2-2025-slides-revenue-jumps-46-achieves-third-profitable-quarter-93CH-4215463

Money Morning. (2025, April 14). Warning: Read this before you buy Webull (BULL) stock. MoneyMorning.com. https://moneymorning.com/2025/04/14/warning-read-this-before-you-buy-webull-bull-stock/

PR Newswire. (2025, May 13). Webull reports first quarter 2025 financial results. PR Newswire. https://www.prnewswire.com/news-releases/webull-reports-first-quarter-2025-financial-results-302463555.html

Simply Wall St. (2025). Webull Corporation (NASDAQ: BULL) past performance and analysis. SimplyWall.st. https://simplywall.st/stocks/us/diversified-financials/nasdaq-bull/webull/past

Value The Markets. (2025, June 30). Webull Corporation stock (BULL): Is it a buy at these levels? ValueTheMarkets.com. https://www.valuethemarkets.com/analysis/webull-corporation-stock-bull

WallStreetZen. (2025). Webull (BULL) revenue 2023–2025. WallStreetZen.com. https://www.wallstreetzen.com/stocks/us/nasdaq/bull/revenue

Webull. (2025, July 22). Webull news update: Market and company overview. Webull.com. https://www.webull.com/news/12711197501137920