Halloween has always been more than just costumes and candy to me—it’s a celebration of creativity, community, and connection. Every October 31st, the air fills with excitement and the scent of autumn leaves, as neighborhoods come alive with laughter, decorations, and the unmistakable crunch of candy wrappers.

For me, Halloween is about sharing the fun. It’s the night when families come together, friends roam the streets in costume, and everyone—young or old—gets to feel like a kid again. Whether it’s carving pumpkins with family, trading candy with friends, or just admiring the creativity of neighborhood displays, Halloween brings people closer in ways few other holidays can.

The candy, of course, is part of the magic. I still get a nostalgic thrill seeing a bowl filled with mini chocolate bars and colorful wrappers. But even more than the treats, it’s the shared experiences that make the night unforgettable—the laughter, the spooky stories, and the small acts of kindness between neighbors.

As much fun as Halloween is, it’s also important to stay safe while celebrating. Here are a few simple reminders to keep the night full of treats and free of tricks:

🕯️ Halloween Safety Tips

Stay visible. Wear reflective tape or carry glow sticks to make sure drivers can see you.

Check costumes for safety. Avoid masks that block vision and make sure shoes fit properly to prevent tripping.

Stick with a group. Trick-or-treating is always safer—and more fun—with friends or family.

Watch for traffic. Use sidewalks and crosswalks, and never assume drivers can see you.

Inspect your candy. Check all treats before eating—especially anything unwrapped or homemade from strangers.

Keep pets inside. Halloween can be stressful for animals; make sure they’re safe and comfortable.

Be mindful of decorations. Open flames, cords, and fog machines can be hazards—keep pathways clear.

Respect others’ property. Stay on paths and avoid trampling lawns or decorations.

This Halloween, I’ll be out enjoying the fall air, greeting neighbors, and sharing laughs with the people who make the night so special. Because in the end, Halloween isn’t just about the candy—it’s about the memories we make along the way. 👻🍬

When it comes to trading stocks, investors often fall into two camps — those who focus on company fundamentals and those who rely on technical analysis. While fundamental analysis looks at balance sheets, earnings, and valuations, technical analysis dives into price action, chart patterns, and indicators to forecast future moves.

For traders aiming to make timely buy or sell decisions, technical analysis offers a crucial advantage — helping identify trends, reversals, and potential entry and exit points.

Below are some of the most widely used technical indicators, their purposes, and why they matter in today’s volatile market.

🔍 The Most Common Technical Indicators

Indicator

What It Measures

Why Traders Use It

Best For

Moving Average (MA)

Smooths out price data to identify trend direction over time.

Helps confirm whether a stock is in an uptrend or downtrend; filters out noise.

Trend-following and long-term investing.

Relative Strength Index (RSI)

Measures the magnitude of recent price changes to identify overbought or oversold conditions.

Warns when a stock may be overextended and due for a pullback or reversal.

Spotting reversals and short-term corrections.

Moving Average Convergence Divergence (MACD)

Compares two moving averages to identify changes in momentum.

Signals potential buy or sell opportunities when lines cross.

Momentum trading and confirming trend shifts.

Bollinger Bands

Uses standard deviation to define price volatility around a moving average.

Shows when prices may be too high or too low relative to recent movements.

Volatility trading and breakout detection.

Fibonacci Retracement Levels

Highlights potential reversal zones based on key percentage levels (23.6%, 38.2%, 61.8%).

Used to predict potential support or resistance levels.

Swing trading and pullback analysis.

Volume

Tracks the number of shares traded during a period.

Confirms the strength of price movements; rising volume supports the trend.

All trading styles.

Stochastic Oscillator

Compares a stock’s closing price to its price range over a period.

Helps pinpoint overbought and oversold conditions similar to RSI but more sensitive.

Short-term timing of trades.

Average True Range (ATR)

Measures market volatility by analyzing the range of recent price movements.

Helps set realistic stop-loss levels and position sizing.

Risk management and volatility assessment.

💡 Why Technical Tools Matter

Better Timing: Technical indicators help traders time their entries and exits more effectively — a critical edge in short-term trading.

Objective Decision-Making: Instead of relying on emotions or market rumors, indicators provide quantifiable signals based on data.

Risk Management: Tools like ATR and volume analysis help traders control risk exposure and avoid chasing unstable moves.

Market Confirmation: When multiple indicators align — such as RSI showing strength and MACD confirming a bullish crossover — confidence in a trade setup grows significantly.

⚠️ A Word of Caution

No single indicator guarantees success. In fact, overloading your chart with too many signals can cause “analysis paralysis.” The key is to combine two or three complementary indicators that confirm one another — such as using a moving average for trend, RSI for momentum, and volume for confirmation.

✅ The Takeaway

Technical analysis isn’t about predicting the future — it’s about improving probabilities. When used correctly, these tools help traders manage risk, find higher-probability trades, and stay disciplined through market noise.

Whether you’re day trading or swing trading, understanding the language of charts and indicators can help you make smarter, more confident investing decisions.

As retirement approaches, one of the biggest financial questions homeowners face is whether to pay off their mortgage early or hold on to the cash for flexibility and investments. Both paths have strong arguments, and the right choice often depends on your personal goals, financial stability, and tolerance for risk.

🔹 The Case for Paying Off Your Mortgage

1. Peace of Mind and Lower Expenses Eliminating your mortgage before retirement means you’ll enter your golden years without one of your biggest monthly bills. This can bring enormous peace of mind—especially for retirees living on a fixed income. Without a mortgage, your monthly expenses drop dramatically, making it easier to stretch your retirement savings further.

2. Guaranteed Return on Investment Paying off your mortgage is like earning a “risk-free” return equal to your interest rate. For example, if your mortgage rate is 6%, you’re effectively earning a guaranteed 6% return by eliminating that debt—a tough benchmark for low-risk investments to match.

3. Emotional and Financial Freedom Many homeowners simply like the feeling of owning their home outright. It provides a sense of security knowing that, no matter what happens to the market or the economy, you have a paid-off place to live.

🔸 The Case for Keeping the Mortgage and Saving the Cash

1. Liquidity and Flexibility Once you pay off your mortgage, that cash is locked into your home’s equity. While you can access it through a home equity line or reverse mortgage, those options can be costly or hard to qualify for in retirement. Keeping cash in savings or investments gives you flexibility for emergencies, healthcare costs, or opportunities.

2. Potential for Higher Returns If your mortgage rate is relatively low—say, under 4%—you might earn more by investing your money instead of paying off the loan. Historically, diversified portfolios have returned more than typical mortgage rates over the long term, allowing your wealth to grow faster while you continue making manageable payments.

3. Tax and Inflation Advantages For some retirees, mortgage interest may still be tax-deductible, reducing overall borrowing costs. Additionally, with inflation, the real value of your fixed mortgage payments decreases over time—meaning you’re repaying the loan with “cheaper” dollars in the future.

⚖️ Finding the Right Balance

Many experts suggest a hybrid strategy:

Pay down your mortgage enough to feel comfortable with the lower balance and payments.

Keep a healthy cash reserve or investment portfolio for flexibility.

Ultimately, the best choice depends on your individual circumstances—your mortgage rate, your savings, your risk tolerance, and how much you value financial security versus potential growth.

🧭 Final Thought

There’s no one-size-fits-all answer. The “right” move is the one that helps you sleep well at night, knowing your finances are positioned to support your lifestyle and goals. Whether that means living debt-free or keeping your investments working, it’s about creating a retirement plan that gives you confidence, comfort, and control.

When it comes to homeowners insurance, most people focus on protecting their property from fire, theft, or storm damage. But one of the most overlooked—and most important—aspects of your policy is liability coverage. This protection kicks in when someone is injured on your property or if you accidentally cause damage to someone else’s property. And if you’re hiring contractors to work on your home, ensuring they’re properly insured could save you from financial disaster.

Understanding Liability Limits

Every homeowners insurance policy includes personal liability coverage, typically starting around $100,000 but often ranging up to $500,000 or more. This coverage helps pay for medical bills, legal fees, and settlements if you’re found responsible for an injury or property damage.

For example, if a guest slips on your icy driveway or a tree from your yard damages your neighbor’s fence, your liability coverage helps cover those costs. But here’s the catch—if damages exceed your policy limit, you’re personally responsible for the rest.

That’s why many insurance professionals recommend reviewing your limits regularly and considering an umbrella policy for extra protection. An umbrella policy can provide an additional $1 million or more in liability coverage for a relatively small cost each year.

The Hidden Risk of Uninsured Contractors

Home improvement projects often involve hiring outside help—roofers, electricians, painters, or landscapers. But before you hand over the keys or cut that first check, it’s critical to make sure any contractor working on your property carries their own liability and workers’ compensation insurance.

If a contractor is uninsured and one of their workers gets hurt on your property, you could be held liable for medical expenses, lost wages, or even lawsuits. Similarly, if they accidentally damage your home or a neighbor’s property, and they’re not covered, your own insurance might have to step in—potentially driving up your premiums or leaving you with out-of-pocket costs.

Protecting Yourself and Your Investment

Your homeowners insurance does more than protect your house—it protects your financial future. By maintaining sufficient liability limits and ensuring contractors are properly insured, you can avoid costly surprises if something goes wrong. A few minutes of due diligence today can save you thousands—and a lot of stress—tomorrow.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

TAMPA – October 21, 2025 — The brokerage and trading-platform firm Webull Corporation (ticker BULL) finds itself trading near multi-year lows. For value-oriented investors, that raises a classic question: Is this a moment of opportunity, or a warning that things are worse than they appear?

Here’s what investors need to know:

1. The Case For: Potential Upside From a Low Base

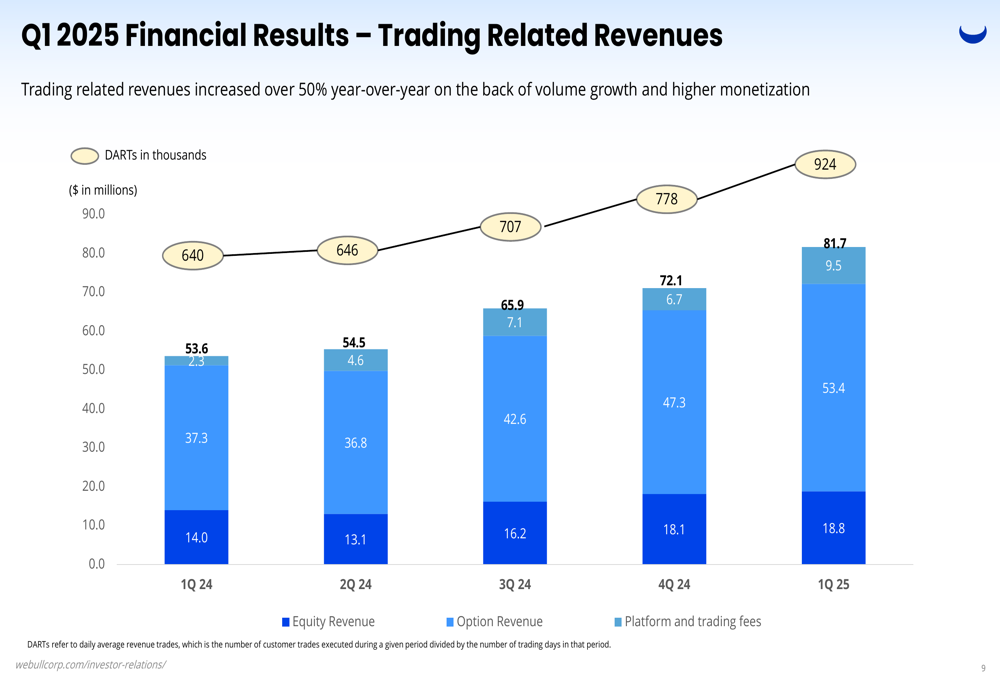

Webull reported strong top-line growth in recent quarters. In Q1 2025, revenues rose by 32 % year-over-year to about US$117 million, and the company swung from a loss to a net income of around US$12.9 million. (PR Newswire+2StockAnalysis+2)

In Q2 2025, revenue came in at roughly US$131.5 million, up ~46 % vs Q2 2024 (~US$90.1 million) — showing accelerating growth in that period. (Investing.com+2WallStreetZen+2)

The stock has already fallen steeply from its earlier highs. Some market commentary suggests that when a stock has dropped hard, it might set up for a rebound if fundamentals improve. (Value The Markets+1)

Webull’s business model—zero-commission trading, fractional shares, global expansion—remains relevant in the growing world of retail finance and digital investing. Supportive structural tailwinds could help long-term. For example, the company claims global reach and a broad user base. (AInvest+1)

2. The Case Against: Key Risks That Still Loom

While revenue is growing, the annual full-year revenue for 2024 was essentially flat compared to 2023 (~US$390.2 million in both years) — indicating growth isn’t guaranteed or smooth. (WallStreetZen+1)

Profitability remains a concern: Return on equity and profit margins are weak or negative in many recent periods. (Simply Wall St+1)

The company competes in a crowded sector (digital brokerages, fintech platforms) with strong incumbents like Robinhood Markets. Analysts have flagged slower growth vs bigger rivals. (Webull+1)

There are corporate-structure complexities and lock-up/share dilution risks. A financial-news piece noted that if the stock trades above US$12 for 20 days, up to 25 % of locked shares might be released, potentially expanding supply. (Money Morning)

3. Why “At All-Time Lows” Could Be a Turning Point

Many stocks trade at depressed levels because the market has lost confidence. That creates a scenario where:

The “bad news” may be largely baked into the price, so incremental positive surprises can have outsized impact.

A low base offers more upside potential if things go well (i.e., less downside cushion). For Webull, if growth continues and profitability improves, the market could reward the turnaround possibility. On the flip side, if risks intensify, the low price could still go lower.

4. What to Monitor Going Forward

Investors considering Webull should keep a close eye on:

Upcoming quarterly results: Are revenues continuing to grow at high rates? Are expenses under control?

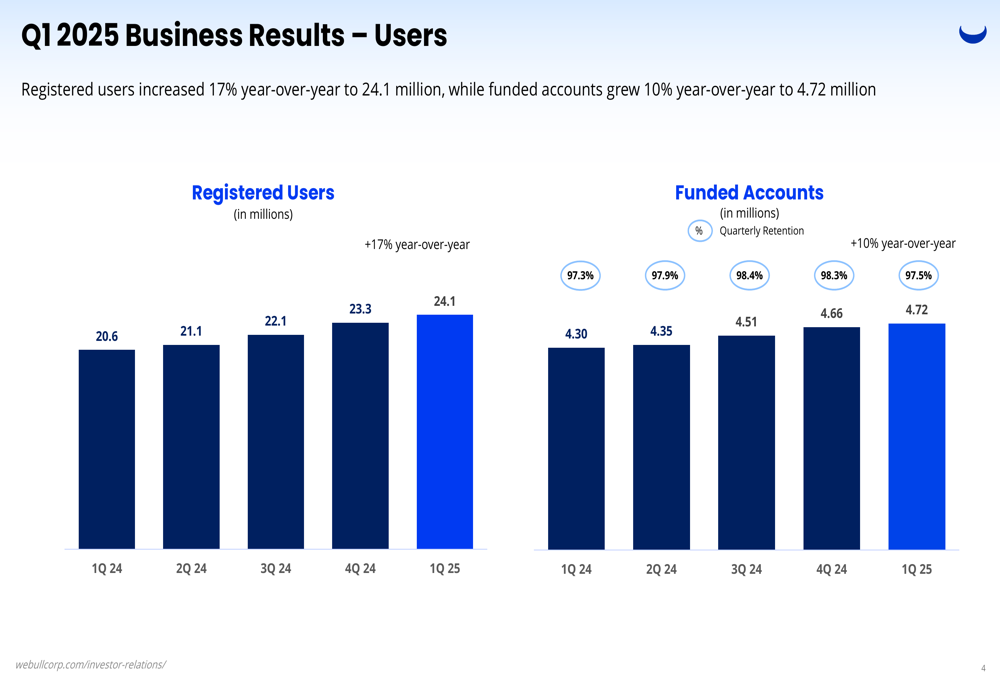

Account growth and trading volume: How many active/funded accounts? What is customer asset growth?

Profit margins and net income: Are they trending toward consistent profitability?

Share-count / dilution risk: Are there significant new shares coming? Are previously locked shares being released?

Competitive dynamics and regulatory risks: Any new regulatory headwinds? How is Webull distinguishing itself vs other brokers?

5. Summary: A High-Risk, High-Potential Setup

In short: Webull is not a safe, boring investment. It carries meaningful operational and structural risk. But the combination of decent recent growth, a depressed share price, and a business model aligned with retail investing trends makes it plausible that at these levels, the upside could be interesting if things go right.

For investors comfortable with risk and looking for speculative exposure in the fintech/brokerage space, BULL might offer a worthwhile “bet.” For more conservative investors, the uncertainty may be too large.

Before investing, one should do their own due diligence, weigh risk vs reward carefully, and consider how this fits into an overall portfolio.

Above: Representative charts showing (1) share-price path of Webull (BULL), (2) recent revenue growth, (3) user growth/expansion metrics.

Disclaimer

This is not financial advice. The information above is for educational and informational purposes only. Investing involves risks, including loss of principal. Always consult a qualified financial advisor regarding your specific situation.

For many homeowners, rising home values have created an opportunity to tap into their property’s equity — the difference between what you owe on your mortgage and what your home is worth. Using home equity can be a smart financial move, especially if you’re looking to pay off high-interest debt or fund major home improvements. But it’s not without risk.

Turning Equity Into Opportunity

Home equity loans and home equity lines of credit (HELOCs) allow you to borrow against the value of your home, often at lower interest rates than credit cards or personal loans. This can make them an appealing tool for consolidating high-interest debt, such as credit card balances that can quickly spiral out of control.

For example, replacing 25% interest credit card debt with a 7% home equity loan can save thousands in interest payments. Others use their home’s equity to finance renovations that can increase property value — like updating kitchens, adding energy-efficient systems, or finishing basements.

Understanding the Risks

While the benefits are clear, borrowing against your home’s equity comes with significant responsibilities. If you can’t make payments, you risk losing your home through foreclosure.

Home equity loans also increase your overall debt load, and if home prices fall, you could owe more than your property is worth — a situation known as being “underwater.” It’s also easy to fall into a debt cycle: paying off high-interest credit cards with a home loan only to run up balances again.

When It Makes Sense — and When It Doesn’t

Experts suggest using home equity strategically — for investments that add long-term value, like home improvements or education, not for short-term expenses or vacations. If you’re consolidating debt, make sure to address the spending habits that created it in the first place.

Before borrowing, compare rates, fees, and terms from multiple lenders, and consider talking to a financial advisor.

Key Takeaway

Home equity can be a valuable financial tool when used wisely — but it’s not “free money.” Every dollar you borrow is secured by the roof over your head. The best strategy is to borrow with purpose, have a clear repayment plan, and ensure the benefits outweigh the long-term costs.

Our bodies are incredible machines—constantly adjusting, healing, and protecting us from harm. But when something goes wrong, from infection to stress or injury, the body has a built-in set of alarms and defense systems that kick into gear. Understanding these reactions can help you recognize early warning signs and take better care of your health.

1. The Stress Response

When the brain senses danger—physical or emotional—it signals the adrenal glands to release adrenaline and cortisol. This is the “fight or flight” reaction. Your heart rate speeds up, blood pressure rises, and muscles tense, preparing your body to act fast.

Common triggers: Anxiety, trauma, or sudden physical exertion. What to watch for: Rapid heartbeat, sweating, or feeling “on edge.”

2. The Immune Response

When bacteria, viruses, or toxins invade, the immune system launches an attack. White blood cells swarm to the area, causing inflammation—redness, swelling, and warmth—as part of the healing process.

Common triggers: Infection, injury, or allergic reactions. What to watch for: Fever, fatigue, or localized pain.

3. The Pain Response

Pain is the body’s alarm system. Nerves send signals to the brain to warn that something is wrong. Acute pain helps you react quickly—like pulling your hand away from a hot surface—while chronic pain can signal ongoing issues that need attention.

Common triggers: Injury, inflammation, or nerve damage. What to watch for: Persistent pain that doesn’t improve with rest or medication.

4. The Hormonal Response

Hormones regulate nearly every process in the body. When something goes off balance—like blood sugar or thyroid function—the body compensates by adjusting hormone levels. Over time, these shifts can lead to fatigue, mood swings, or weight changes.

Common triggers: Stress, poor diet, lack of sleep, or illness. What to watch for: Sudden changes in energy, appetite, or emotional state.

5. The Cellular Repair Response

Cells are constantly repairing themselves. When DNA is damaged—by sun exposure, toxins, or normal aging—the body sends repair enzymes to fix it. If this process fails, it can lead to mutations or diseases.

Common triggers: UV light, pollution, smoking, or aging. What to watch for: Slow healing wounds or unusual skin changes.

📊 Chart: How the Body Responds When Something Goes Wrong

Body System

Trigger

Response

Common Symptoms

Purpose

Nervous System

Stress, fear, trauma

Fight-or-flight (adrenaline surge)

Fast heartbeat, sweating, tension

Prepare for danger

Immune System

Infection or injury

Inflammation, fever

Swelling, fatigue, pain

Destroy invaders and heal tissue

Endocrine System

Hormonal imbalance

Hormone release or suppression

Mood swings, weight change

Maintain internal balance (homeostasis)

Musculoskeletal

Injury or strain

Muscle contraction, repair signals

Pain, swelling, stiffness

Protect and heal damaged tissue

Cellular/DNA Repair

UV, toxins, aging

DNA repair or apoptosis

Slow healing, fatigue

Prevent mutation and maintain function

Why it Matters

Recognizing how your body responds to stress, injury, or imbalance helps you take control of your health. Awareness leads to action—and action leads to prevention.

Quick take: Zeta Global, the AI-driven marketing cloud, has delivered a string of better-than-expected quarters, is guiding to another year of strong revenue growth, and just made a big acquisition to expand its loyalty and enterprise footprint. That combination — accelerating revenue, improving profitability guidance, and strategic M&A — is why some investors are re-rating the stock. Below: the facts, the catalyst, a compact risk view, and a chart/table that show the growth story.

Headlines and the data points you need

Zeta reported Q2 2025 revenue of $308.4 million, a ~35% year-over-year increase vs. the prior year quarter. (Nasdaq)

For full-year 2024 Zeta generated about $1.01 billion in revenue. (Zeta Global)

Management has repeatedly “beat and raise” — most recently increasing full-year 2025 revenue guidance to $1,258–$1,268 million (midpoint ~$1.263B) and raising Adjusted-EBITDA and free-cash-flow ranges as well. Those revisions reflect faster growth and improving margins. (Zeta Global+1)

Zeta announced a large acquisition (Marigold’s enterprise business — including Cheetah Digital, Selligent, Sailthru and other assets) to strengthen loyalty and enterprise offerings, a move management says accelerates international reach and cross-sell opportunities. (Zeta Global+1)

Market snapshot (at time of writing): share price ≈ $20.37 and market cap in the mid-$4 billion range — investors are paying for fast growth but also a path to profitability. (Yahoo Finance)

Why this could be an attractive investment (the bull case)

High single- to double-digit top-line growth that’s accelerating. Zeta’s recent quarters show consistent revenue acceleration (Q2 ’25 +35% YoY), a key signal for growth investors in the martech/adtech space. Management’s upward guidance for FY-2025 reinforces that it’s not just one quarter of outperformance. (Nasdaq+1)

Improving operating leverage and cash generation. The company has raised Adjusted-EBITDA and free-cash-flow guidance, pointing to margin expansion. That’s important: investors reward companies that can turn revenue growth into sustainable profits and cash. (Zeta Global)

Strategic M&A that fills capability gaps and expands addressable market. The Marigold enterprise business deal adds loyalty platforms and prominent enterprise customers (and EMEA coverage), enabling more cross-sell inside an existing customer base and a larger recurring revenue pool. If integration goes smoothly, this can boost both revenue and churn resilience. (Zeta Global+1)

Compelling unit economics at scale. Zeta reports improving ARPU (average revenue per scaled customer) and strong net revenue retention metrics, which suggest existing customers are spending more — a powerful multiplier for SaaS-like businesses. (Company disclosures highlight rising Scaled and Super-Scaled customer ARPU.) (Zeta Global+1)

Positive technical / market interest. Stock research outlets have recently upgraded technical scores (e.g., IBD RS rating rise), indicating renewed investor interest that can amplify returns if fundamentals keep improving.( Investors.com)

Visual: revenue comparison (Q2 vs prior year, FY 2024 vs FY 2025 guidance)

I created a compact chart and table comparing:

Q2 2024 (estimate) vs Q2 2025 actual, and

FY 2024 actual vs FY 2025 guidance midpoint.

(Chart and table were prepared from the company reporting and guidance figures cited above).

Sources for the plotted numbers: Q2 2025 revenue and YoY change, FY 2024 totals, and FY 2025 guidance. (Nasdaq+2Zeta Global+2)

Risks — what could go wrong

Execution risk on M&A and integration. The Marigold enterprise assets are substantial; integration issues, customer churn, or higher-than-expected costs could blunt the benefits. (Zeta Global)

Valuation vs. growth tradeoff. The stock price reflects future growth expectations. If revenue growth slows or margin expansion stalls, multiples can compress quickly. (Yahoo Finance)

Adtech / martech competition and cyclicality. The market is competitive (large incumbents and many specialists). Ad/spend cyclicality could affect revenue. Company performance depends on continued client spend and retention. (Zeta Global)

Profitability not yet fully GAAP positive. Zeta has narrowed losses but still reports GAAP net losses; investors should watch sustained EBITDA and free-cash-flow conversion. (Zeta Global)

Bottom line (concise)

Zeta Global presents a classic high-growth martech investment case: accelerating revenue, improving profitability guidance, and strategic M&A that extends its product footprint and international reach. That combination can create durable revenue expansion and margin improvement — the ingredients growth investors pay for. But the stock still carries execution and integration risk and depends on preserving high retention and ARPU. If you like fast growth with a clear path to margin expansion and accept the M&A/integration risk, Zeta is a name to research further; if you are risk-averse or need immediate GAAP profitability, it may not fit.

Disclosure:

I do not own any stock or have any financial interest in Zeta Global Holdings (NYSE: $ZETA). This article is for informational purposes only and should not be considered financial or investment advice. Investing in stocks carries risks, and past performance is not indicative of future results. Always conduct your own research and consult with a qualified financial professional before making any investment decisions.

References

Zeta Global Holdings Corp. (2025, August 8). Zeta reports second quarter 2025 financial results; raises full-year 2025 guidance. Zeta Global Investor Relations. Retrieved from https://investors.zetaglobal.com/

Zeta Global Holdings Corp. (2024, February 28). Zeta reports fourth quarter and full-year 2024 results. Zeta Global Investor Relations. Retrieved from https://investors.zetaglobal.com/

Investor’s Business Daily. (2025, September). Zeta Global stock analysis and relative strength update. Investor’s Business Daily. Retrieved from https://www.investors.com/

Reuters. (2025, September). Zeta Global Holdings Corp. company profile and financial summary (ZETA.O). Reuters Markets. Retrieved from https://www.reuters.com/

MarketWatch. (2025, October). Zeta Global Holdings Corp. stock quote & financials (ZETA). MarketWatch. Retrieved from https://www.marketwatch.com/

Business Wire. (2025, July 31). Zeta Global announces acquisition of Marigold’s enterprise business to expand loyalty and EMEA presence. Business Wire. Retrieved from https://www.businesswire.com/

Yahoo Finance. (2025, October 9). Zeta Global Holdings Corp. (ZETA) stock price and market cap data. Yahoo Finance. Retrieved from https://finance.yahoo.com/

From classrooms to careers, the ability to learn quickly and remember effectively has become one of the most valuable skills a person can develop. Strong memory and sharper learning don’t just lead to better grades or job performance—they also support long-term health and financial success. A stronger mind means better choices, less stress, and greater opportunities.

1. Embrace Active Learning Engaging with material—summarizing, teaching, or using flashcards—creates stronger memory pathways. Beyond academics, this skill translates into sharper thinking in business and personal finance, where quick recall of information can mean smarter money choices.

2. Use Spaced Repetition By reinforcing knowledge over time, you’re not only improving retention but also reducing the stress that comes with last-minute cramming. Lower stress means healthier blood pressure and better long-term focus—both of which are linked to higher productivity and earning potential.

3. Prioritize Sleep Sleep is the body’s reset button. It strengthens memory, sharpens focus, and promotes better decision-making. Studies show well-rested people are less likely to make impulsive purchases, more effective at managing investments, and healthier overall.

4. Exercise for Brain Health Movement increases blood flow and oxygen to the brain, boosting memory and creativity. Regular exercise has also been tied to higher lifetime earnings by improving workplace performance and reducing healthcare costs.

5. Practice Mindfulness and Meditation Mindfulness lowers stress hormones, improves concentration, and sharpens memory. The payoff is twofold: better mental health and more disciplined financial habits, since mindfulness helps people avoid emotional, costly decisions.

6. Fuel Your Brain with the Right Nutrition A diet rich in brain-boosting foods like salmon, nuts, and leafy greens not only strengthens cognitive function but also reduces the risk of costly long-term health problems. Investing in nutrition today saves on medical expenses tomorrow.

7. Limit Multitasking Single-tasking leads to better retention and fewer mistakes—whether you’re learning new skills, balancing your budget, or making a career move. Fewer mistakes in health and financial decisions directly translate to long-term gains.

8. Use Mnemonics and Visualization Simple memory tools like acronyms or visualization techniques make learning easier. Applied to personal finance or career growth, these methods help people remember key strategies, deadlines, and opportunities—small advantages that compound into wealth.

Looking Ahead Improving how you learn and remember doesn’t just give you an edge in the classroom or workplace. It’s also a blueprint for healthier living and greater financial success. By combining proven learning strategies with lifestyle habits that strengthen the brain, you can build a sharper mind, a stronger body, and a wealthier future.

Herzliya, Israel / U.S. Markets — Beamr Imaging Ltd. (NASDAQ: BMR) is a tiny, high-volatility tech play in the video compression / optimization space. In recent months, it has attracted attention from speculative investors betting on its ability to break into high-growth verticals like autonomous vehicles (AV). Below is a breakdown of its recent developments, risks, and upside potential.

What Does Beamr Do?

Beamr provides software and hardware-accelerated video encoding, transcoding, and optimization solutions. Its product lineup includes:

Beamr IP blocks (for integration into ASICs / GPUs / application processors)

JPEGmini photo optimization technology

Its customer base spans streaming platforms, media companies, content distributors, and now increasingly, autonomous vehicle and machine-vision use cases. (Yahoo Finance+2investors.beamr.com+2)

In 2025, the company has doubled down on pushing into the AV market by unveiling a GPU-accelerated video compression solution designed to handle petabyte-scale video data generated by autonomous vehicle fleets. (Investing.com+2Stock Titan+2)

A key value proposition: its compression technology reportedly delivers 20%–50% savings in storage and data transfer costs for customers, without degrading model accuracy in machine vision applications. (Stock Titan+1)

Recent Financials & Metrics

Below is a simplified financial snapshot based on the public disclosures (primarily for 1H 2025). Because Beamr is small and reporting is limited, the data should be taken as directional rather than precise.

From alternative data sources, Reuters lists Beamr’s total assets at USD 22.095M (latest) and notes negative cash flows from operations, consistent with a growth / development stage firm. (Reuters)

Caveats & caveats:

The company is unprofitable and burning cash.

Operating expenses are rising aggressively.

Revenue scale is still extremely modest.

Reporting is limited, making forecasting uncertain.

The stock is highly volatile and likely illiquid in many trading periods.

Recent Developments & Catalyst Events

AV Market Push: In mid-2025, Beamr formally launched its GPU-accelerated video compression solution for autonomous vehicles, executing multiple proof-of-concept (PoC) deals and aiming to position itself as a bridge between AV fleets (which generate enormous video data) and cost-efficient storage/processing infrastructure. (Yahoo Finance+4Investing.com+4Stock Titan+4)

Strong Price Movement on Announcement: When Beamr announced the AV compression launch at the NVIDIA GTC Paris event, the stock spiked ~17% intraday. (RTT News)

Oracle Cloud Marketplace Listing & Recognition: Beamr’s product became available in Oracle’s Marketplace (earning “Powered by Oracle Cloud Expertise” status), driving a stock move of ~48% on that news. (The Wall Street Journal)

Partnership & Ecosystem Moves: The company joined AWS’s ISV Accelerate program, participated in major industry events (NVIDIA GTC, NAB Show), and secured awards (e.g. NAB Show Product of the Year) for its video technology. (Quiver Quantitative+3Stock Titan+3investors.beamr.com+3)

Strong Liquidity Ratio: Reports suggest Beamr had a current ratio (current assets / current liabilities) of ~17.77 in H1 2025, indicating a solid short-term liquidity buffer. (Investing.com)

Why Some Speculators Believe Upside Is Possible

Here’s the bullish thesis (with caveats) for why investors might view Beamr as a high-risk, high-reward play:

Large addressable markets

The explosion of video data (streaming, 5G, ML/AI, edge computing) presents tailwinds for efficient compression/optimization.

The AV industry is a nascent but rapidly expanding consumer of video/vision data; any solution that materially reduces cost could attract high-value contracts.

Technical differentiation (if proven)

If Beamr’s compression can deliver promised 20–50% reductions in storage + network cost without compromising model accuracy or visual quality, that’s a compelling ROI proposition for customers.

Their GPU-accelerated and content-adaptive approach may be more scalable and future-forward than legacy compression tools.

Low valuation / optionality

As a microcap trading near its cash value, much of the upside is tied to growth and execution (i.e., if they convert PoCs to commercial contracts).

If one or two large AV or cloud customers adopt their technology, the “optional upside” is significant.

Momentum & narrative-driven upside

In small, speculative tech stocks, favorable press, partnerships, and media hype can drive rapid re-rating.

Their association with big names (NVIDIA, AWS, Oracle) lends credibility and can accelerate business traction.

Liquidity cushion

Having nearly $14M in cash for a company of this size gives it runway to invest in growth, product development, and marketing (assuming no major execution failure).

Risks That Temper the Speculation

To balance the bullish perspective, here are key risks:

Execution risk: Converting PoCs into recurring, large-scale revenue is harder than it looks.

Competitive risk: Many large players (cloud providers, codec developers, chipmakers) might replicate or undercut.

Burn & dilution risk: Continued losses may force equity raises, which could dilute existing holders.

Thin trading / volatility: Stock may swing wildly on news (or lack thereof).

Dependence on marquee wins: A few large contracts must validate the model.

Technology risk: Compression for human vision is a different problem than “machine vision / AV grade” compression; errors or compromises in accuracy could kill the value proposition.

Outlook & Scenarios

Base Case (moderate success): Beamr secures a handful of mid-sized AV or cloud contracts over the next 1–2 years; revenue grows meaningfully, losses narrow, and the stock re-rates modestly (e.g. 2×–3× current valuation).

Bull Case (breakthrough): A marquee deal or partnership (e.g. with a top AV OEM or cloud provider) turns into a large recurring revenue stream. The market begins to value Beamr as a strategic infrastructure play, leading to 5×+ upside.

Bear Case: Execution falters, PoCs don’t convert, cash burns down, and the company faces liquidity or solvency challenges, dragging the stock back toward cash value (or below).

Disclosure: I currently hold a position in Beamr Imaging Ltd. (NASDAQ: BMR). This article reflects my personal opinions and analysis, and is not intended as financial advice. Please conduct your own research or consult a financial advisor before making any investment decisions.