Estate planning is often postponed because it feels complex or uncomfortable. However, one of the most practical and effective tools available is a trust. Establishing a trust can provide clarity, protection, and efficiency for your assets after you die, while also reducing stress for your loved ones. For homeowners in particular, placing a home into a trust and aligning your homeowners insurance accordingly can be a critical but often overlooked step.

What Is a Trust and Why Does It Matter?

A trust is a legal arrangement in which one party (the trustee) holds and manages assets on behalf of beneficiaries according to instructions you set. Unlike a will, many trusts allow assets to bypass probate, the court-supervised process that can be time-consuming, costly, and public.

Key benefits of a trust include:

Avoiding probate delays

Maintaining privacy

Providing clearer asset distribution

Offering continuity if you become incapacitated

Reducing the likelihood of disputes among heirs

For many families, these advantages alone justify serious consideration.

Why Include Your Home in a Trust?

For most people, their home is their largest asset. Placing your home into a trust can simplify its transfer to heirs and ensure continuity of ownership. However, doing so requires coordination beyond just updating a deed.

One critical step is updating your homeowners insurance policy.

If your home is owned by a trust, the trust should typically be listed as either:

The named insured, or

An additional insured on the policy

Failing to align insurance with ownership can create coverage gaps. In the event of a claim, an insurer may question whether the correct legal entity is covered, potentially delaying or complicating payouts. Properly titling the policy helps ensure:

Claims are paid without dispute

Liability protection extends to the trust

Coverage reflects the true owner of the property

This is a detail many homeowners miss and one that can have serious consequences if overlooked.

Things to Consider When Establishing a Trust (Beyond Insurance)

While insurance alignment is important, it is only one piece of the decision. When creating a trust, you should also consider:

1. Type of Trust

Revocable trusts offer flexibility and control during your lifetime.

Irrevocable trusts may provide tax or asset-protection benefits but limit your ability to make changes.

2. Trustee Selection Choosing a responsible trustee is critical. This can be a trusted individual or a professional institution. The wrong choice can lead to mismanagement or family conflict.

3. Asset Scope Decide which assets should go into the trust. Homes, investment accounts, and business interests are common, but not every asset belongs there.

4. Costs and Complexity Trusts involve upfront legal costs and ongoing administrative responsibilities. These should be weighed against the size and complexity of your estate.

5. State-Specific Laws Trust rules vary by state. What works well in one jurisdiction may not in another, making professional guidance essential.

What You Should Not Assume or Overlook

There are also common misconceptions and missteps to avoid:

Do not assume a trust eliminates all taxes. Many trusts offer no automatic tax advantage without specific planning.

Do not assume a trust replaces a will. Most people still need a “pour-over” will to address assets outside the trust.

Do not forget beneficiary updates. Retirement accounts and life insurance pass by beneficiary designation, not by trust instructions unless properly coordinated.

Do not create a trust and fail to fund it. A trust that holds no assets offers little value.

Do not ignore professional advice. DIY trusts may save money upfront but can create costly legal and tax issues later.

A Practical Step Toward Peace of Mind

Setting up a trust is not just about wealth it is about control, protection, and clarity. Including your home in a trust, and ensuring your homeowners insurance reflects that ownership, can prevent unnecessary complications during an already difficult time for your family.

While a trust is not right for everyone, it is a powerful planning tool worth discussing with qualified legal, tax, and insurance professionals. Thoughtful preparation today can make a meaningful difference tomorrow for you and for those you care about most.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As the Christmas decorations come down and routines begin to normalize, the period between the holidays and the New Year offers a valuable opportunity for reflection and preparation. Rather than rushing into resolutions on January 1, many individuals are using this quieter window to assess their priorities and make intentional plans for the year ahead. With 2026 approaching, two areas stand out as especially important: personal health and financial stability.

The end of the holiday season often brings extra spending, disrupted sleep schedules, and indulgent eating. Resetting now allows people to enter the New Year with clarity, momentum, and realistic goals. Experts across healthcare and financial planning consistently emphasize that small, proactive steps taken early can compound into meaningful long-term benefits.

Health Considerations to Prioritize Going Into 2026

Maintaining health is not about drastic changes, but about sustainable habits that support longevity and quality of life. As the New Year approaches, individuals may want to focus on the following:

Routine medical checkups: Scheduling annual physicals, dental visits, and vision exams early in the year helps catch issues before they become costly or serious.

Nutrition reset: Transitioning from holiday eating to balanced, nutrient-dense meals supports energy levels and metabolic health.

Consistent physical activity: Establishing a realistic exercise routine—whether walking, strength training, or flexibility work—improves both physical and mental well-being.

Sleep discipline: Returning to regular sleep and wake times can significantly improve focus, immune function, and stress management.

Stress management: Incorporating practices such as mindfulness, time blocking, or regular downtime can reduce burnout and improve overall resilience.

Wealth Considerations to Strengthen Financial Stability

The New Year is also an ideal time to reassess financial health and prepare for future opportunities and risks. Key areas to consider include:

Budget review: Evaluating holiday spending and updating monthly budgets helps prevent financial drift early in the year.

Emergency savings: Ensuring an emergency fund covers at least three to six months of expenses remains a foundational financial safeguard.

Debt strategy: Creating or refining a plan to reduce high-interest debt can free up cash flow and reduce long-term financial stress.

Retirement contributions: Reviewing contribution levels to retirement accounts and adjusting for income changes or new limits can significantly impact long-term outcomes.

Insurance coverage check: Confirming that auto, home, health, and life insurance policies remain appropriate for current circumstances helps protect against unexpected setbacks.

Investment alignment: Rebalancing portfolios to reflect updated goals, risk tolerance, and time horizons supports disciplined wealth-building.

Entering the New Year With Intention

Getting ready for the New Year does not require sweeping changes or unrealistic resolutions. Instead, it is about thoughtful preparation and alignment. By addressing health and wealth proactively, before January begins, individuals position themselves to move into 2026 with greater confidence, stability, and focus.

The days after Christmas are not just a cooldown from the holidays; they are a strategic pause. How that pause is used can make a measurable difference in the year ahead.

When it comes to staying insured and legally compliant on the road, few documents create more confusion than the SR-22. Contrary to popular belief, an SR-22 is not an insurance policy—it’s a certificate of financial responsibility filed with your state to prove you carry the minimum required auto insurance. For drivers who have encountered serious traffic violations or insurance lapses, filing an SR-22 can be critical to regaining or maintaining driving privileges.

Why You Might Need an SR-22

States typically require an SR-22 after certain high-risk incidents, including:

Driving without insurance If you’re caught driving uninsured—even once—many states will require an SR-22 to verify you remain insured moving forward.

DUI or DWI convictions One of the most common triggers. After a DUI/DWI, drivers must often carry an SR-22 for several years.

Multiple traffic violations or at-fault accidents Repeat offenders or drivers involved in severe collisions may be labeled “high-risk,” prompting the SR-22 requirement.

License suspension or revocation To reinstate your driver’s license, an SR-22 filing may be mandatory.

Serious moving violations Excessive speeding, reckless driving, or hit-and-run incidents sometimes lead to SR-22 mandates depending on the state.

How Long You Must Carry an SR-22

Most states require drivers to maintain an SR-22 for 3 years, though this varies by location and offense. If coverage lapses at any point, your insurance company must notify the state likely resetting the clock on your compliance period.

What an SR-22 Costs

The SR-22 filing fee itself is typically small around $15–$50. However, insurance premiums can increase based on your driving record. Working with a knowledgeable insurance agent can help reduce the financial impact by exploring policy options tailored to high-risk drivers.

The Filing Process: Getting Professional Help

The SR-22 must be filed by a licensed insurance provider on your behalf. Here’s how professionals typically assist:

Assess Your Situation An insurance professional reviews your state’s requirements and the circumstances behind your SR-22 need.

Secure an Eligible Policy Not all insurers offer SR-22 filings. Agents specializing in high-risk auto insurance can pair you with a policy that meets your state’s minimums.

File the SR-22 Electronically Most filings are sent directly to the state within 24–48 hours, speeding up reinstatement timelines.

Provide Guidance and Follow-Up Agents can help you avoid lapses, set up reminders, and secure better rates once your SR-22 period ends.

Suggestions for Drivers Facing an SR-22 Requirement

Act quickly to prevent extended license suspensions.

Compare quotes—prices vary dramatically among providers.

Avoid coverage lapses at all costs.

Consider defensive driving courses to improve your record over time.

Stay insured continuously to begin rebuilding your driving profile.

Referrals and When to Seek Professional Help

If you’re unsure whether you need an SR-22 or how to file one, your best first step is connecting with:

A licensed auto insurance agent specializing in SR-22 filings

A traffic attorney if your requirement stems from a DUI, reckless driving, or a serious violation

Your state’s Department of Motor Vehicles (DMV) for official reinstatement guidelines

These professionals can clarify requirements, ensure proper filing, and help you move forward with confidence.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Planning for retirement isn’t something that should wait until your final working years. One of the smartest steps you can take today “no matter your age” is estimating your future Social Security benefits. Understanding these numbers early helps you make more informed financial decisions, set realistic expectations, and build a roadmap toward a more secure retirement.

Why Estimating Your Benefits Early Matters

1. It Helps You Understand How Much You’ll Actually Need Many Americans overestimate how much Social Security will provide. By checking your personalized benefit estimate now, you can see whether your projected income will cover your essential expenses—and how much more you may need to save.

2. You Can Adjust Your Savings Strategy Ahead of Time If your estimated monthly benefit is lower than expected, learning this early gives you years—even decades—to increase your contributions to a 401(k), IRA, or other retirement vehicles.

3. It Highlights the Value of Working Longer Your Social Security payout is based on your highest 35 years of earnings. Seeing your estimate can motivate you to improve your earnings record or reduce low-income years, increasing your benefit when retirement finally comes.

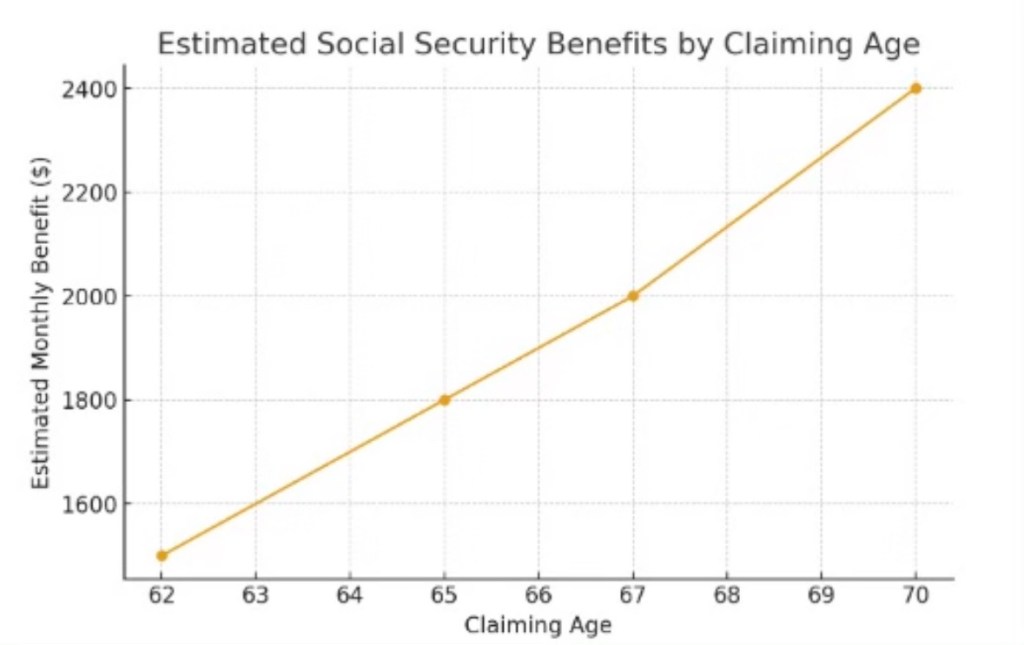

4. Claiming Age Makes a Huge Difference Whether you claim at 62, 67, or 70 dramatically changes your monthly income. Understanding this now helps you plan the right claiming strategy for your lifestyle and goals.

Estimated Social Security Benefits by Claiming Age

Below is a chart illustrating how estimated monthly benefits generally increase the longer you delay claiming:

How to Estimate Your Benefits Today

You can access your personalized estimate at any age by creating or logging into your mySocialSecurity account at SSA.gov. Once inside, you’ll see:

Your projected monthly benefit at age 62

Your full retirement age (typically 67)

Your estimated benefit at age 70

Your complete earnings record

Taking a few minutes to review this information now can help you avoid surprises later and give you the confidence to build a stronger retirement strategy.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As the year winds down, I’ve found myself taking stock of everything that has shaped the past twelve months. No holidays needed—just a quiet moment to appreciate what mattered, what changed me, and what I’m grateful for. And honestly, it’s been a year worth celebrating in its own way.

Thankful for: An Unforgettable Trip to Portugal

This year gave me the chance to travel to Portugal—an experience that left me with memories that still feel fresh every time I think about them. The food, the views, the history, the people… it all created something I’ll carry with me for the rest of my life. I’m thankful I got to see more of the world and step outside the normal routine long enough to appreciate just how big and beautiful life can be.

Thankful for: The Best Wife and Family Anyone Could Ask For

Above everything else, my gratitude starts with the people closest to me. I have a wife who supports me, challenges me, lifts me up, and stands with me through every high and low. I don’t take that for granted. And my family—there’s no better word for it—they’re the foundation. Their encouragement, humor, strength, and love have shaped every success and softened every setback. This year reminded me that I’m surrounded by people who make life better, brighter, and fuller.

Thankful for: Growth Instead of Loss in the Markets

The markets didn’t always make sense this year (do they ever?), but instead of losing, I gained—knowledge, perspective, patience, and confidence. From exploring new investments to studying market behavior, I came out smarter than I went in. Every dip, every rally, every confusing headline ended up teaching me something, and I’m thankful for the journey as much as the results.

Thankful for: Becoming More Insurance-Savvy Than I Ever Expected

This year wasn’t just about financial markets—it was also about sharpening what I know in the world of insurance. From policy details to coverage types, from understanding risks to explaining them, I learned more than I expected—and it’s knowledge that actually matters. It helps me protect myself, protect others, and make smarter decisions. I gained clarity and confidence, and that’s something to be grateful for.

Thankful for: The Lessons, the Growth, and the Wins

This year brought experiences I’ll never forget, people I’ll always be grateful for, and knowledge that will guide me for years to come. It wasn’t perfect—but it was meaningful. And that’s what gratitude is really about: recognizing the good, the growth, and the people who walk beside you.

Here’s to a year of learning, loving, exploring, and becoming better than before. And here’s to being thankful not just for what happened, but for who I’ve become along the way.

Waiting might be one of the few universal human experiences that transcends age, background, income, geography, and even personality. Whether we’re stuck in a doctor’s office long past our appointment time, refreshing a stock chart hoping for a green candle, or watching an insurance claim crawl its way through the system, waiting is a constant companion. And while it can be frustrating, it also reveals a lot about how modern life actually works.

The Doctor Will Be With You… Eventually

Anyone who has ever dealt with healthcare knows that time moves differently in a medical office. You check in early, only to wait 20 minutes to be called, 10 more in the exam room, and maybe another week to get your test results.

Doctors aren’t slow because they want to be; they’re slow because they must be. Every patient brings unpredictability. A quick check-up can instantly turn into a crisis, care requires paperwork, and healthcare systems are overloaded. But as patients, it doesn’t feel like logistics—it feels like we’re just waiting… and waiting.

Many people walk out feeling like they spent more time sitting than being seen. And that’s because they have.

Waiting on the Markets: The Slow Burn of Investing

If there’s any arena that tests patience like a doctor’s office, it’s the stock market. You can research the perfect company, run the numbers, time your entry… and still spend weeks or months waiting for the payoff.

Stocks rarely move on our schedule. Bull markets take time to build, bear markets linger longer than anyone likes, and sideways trading can feel like a cosmic joke designed to test your discipline. You watch your screen, refresh your app, maybe check the news again—just in case something changed in the last 45 seconds.

But over the long run, waiting is the strategy. The real returns historically come not from timing the market, but time in the market. Yet even knowing that, we still find ourselves impatient, hoping our future arrives faster.

Insurance: The Art of Hurry Up and Wait

Insurance is another world where waiting feels baked into the design. You file a claim and expect progress. Instead, you’re asked for more documentation, another photo, a follow-up call, a review, an inspection… and then another review.

Insurance companies aren’t trying to delay—they’re trying to verify. Risk assessment requires accuracy, and accuracy takes time. But when it’s your car, your home, your medical bill, or your livelihood on the line, the process can feel like a slow-motion movie you can’t fast-forward.

Ironically, we pay for insurance to create peace of mind, but the waiting period is often when we feel the least at peace.

Everyday Waiting: The Silent Theme of Modern Life

Outside those big moments, waiting quietly follows us everywhere:

Waiting for a package that says “Out for delivery” for eight hours

Waiting for traffic to move

Waiting for approval, promotion, or a simple call-back

Waiting for the next phase of life—marriage, career change, retirement

Waiting for things to “finally calm down” (which never seems to happen)

Humans weren’t built to sit in uncertainty. Psychologically, waiting triggers the same stress response as danger. Our brains want clarity and control—two things waiting rarely provides.

The Hidden Reason We Wait: Progress Takes Time

Whether it’s the doctor, the market, insurance, or our daily errands, waiting is ultimately a byproduct of systems in motion. Progress doesn’t happen in a straight line or on a schedule we set.

In many ways, waiting is proof that something is happening:

The doctor is giving someone else the attention you’ll soon get

The stock market is adjusting, recalibrating, and preparing for the next move

The insurance company is verifying everything you need to protect your future

Life is unfolding in real time—not rushed, not delayed, simply moving at its own pace

We wait because the world is constantly working behind the scenes, even when we can’t see it.

Turning Waiting Into Something Useful

While we can’t eliminate waiting, we can change what it means to us. Waiting offers a rare chance to pause—a moment to reflect, reset, or simply breathe. It forces us to surrender a little control and trust the process, uncomfortable as that may be.

Because when the moment finally comes—whether it’s the doctor walking in, your stock finally breaking out, or the insurance claim resolving—waiting reminds us that good things often take time.

And maybe, just maybe, learning to wait is one of the most valuable skills we’ll ever develop.

As more Americans approach retirement, many are finding that the path to a secure and fulfilling post-work life is more complex than they expected. While saving money is an important first step, a successful retirement hinges on avoiding common pitfalls that can derail even the most carefully built plans. Here are some of the most frequent retirement traps—and smarter strategies to consider instead.

Trap 1: Relying Too Heavily on Social Security

Many retirees assume Social Security will replace most of their income, only to discover their benefits cover far less than expected. With the average monthly benefit hovering around modest levels, relying on Social Security alone can put retirees at risk of falling behind rising costs of living and healthcare expenses.

A smarter alternative: Build a layered income plan that includes Social Security, retirement accounts like 401(k)s or IRAs, pensions (if available), and supplemental income sources. Consider part-time work or consulting if feasible. The key is diversifying your income streams so one isn’t carrying the entire load.

Trap 2: Underestimating Healthcare Costs

Healthcare is one of the biggest retirement expenses, and Medicare doesn’t cover everything. Many retirees are shocked by premiums, deductibles, dental costs, and long-term care needs.

A smarter alternative: Plan early. Look into long-term care insurance or hybrid life-insurance policies with LTC riders. Create a dedicated healthcare fund within your retirement savings. And don’t overlook supplemental Medicare plans that can greatly reduce out-of-pocket expenses.

Trap 3: Cashing Out Retirement Accounts Too Early

Taking large withdrawals early in retirement—especially before age 59½—can trigger steep taxes and penalties, diminishing your long-term nest egg. Even after that age, withdrawing too aggressively can make savings run out sooner than expected.

A smarter alternative: Use a structured withdrawal plan, such as the 4% rule or dynamic withdrawal strategies that adjust based on market performance. Pair withdrawals with tax-efficient strategies like Roth conversions before RMD age to reduce future tax burdens.

Trap 4: Failing to Account for Inflation

Inflation has made a fierce comeback in recent years. Retirees with fixed incomes or overly conservative portfolios risk losing purchasing power over time.

A smarter alternative: Include growth investments—like diversified stock funds—even in retirement, to stay ahead of inflation. Treasury Inflation-Protected Securities (TIPS) and annuities that offer inflation adjustments can also provide peace of mind.

Trap 5: Overlooking Housing Costs

Many retirees assume their housing expenses will drop once the mortgage is gone, but property taxes, insurance, and maintenance continue—and often increase.

A smarter alternative: Evaluate your housing situation realistically. Downsizing, relocating to a lower-cost area, or exploring 55+ communities may reduce expenses. Some retirees also use a portion of home equity strategically through downsizing or a Home Equity Conversion Mortgage (HECM) as part of their financial plan.

Trap 6: Not Preparing Emotionally for Retirement

Retirement isn’t just a financial transition—it’s a lifestyle change. Without structure, purpose, or social engagement, many retirees face loneliness, boredom, or even depression.

A smarter alternative: Design your retirement life as intentionally as your financial strategy. Volunteer, join clubs, take classes, or explore part-time work in a field you enjoy. Staying mentally and socially active is essential for long-term well-being.

Smart Alternatives for Soon-to-Be and Current Retirees

Beyond avoiding traps, here are simple, proactive steps that make retirement more stable and satisfying:

Create a retirement income roadmap that outlines exactly where your money will come from and how long it should last.

Meet with a financial professional to stress-test your plan against inflation, market downturns, and health surprises.

Diversify income, including predictable sources like annuities, rental income, dividends, or guaranteed pension payouts.

Stay flexible—your retirement plan should evolve as life, health, and markets change.

Review your insurance coverage, including life, home, auto, and long-term care, to ensure you’re protected.

Stay active and engaged, both socially and physically, to support overall happiness and health.

Long and Short

Retirement doesn’t have to be uncertain. By steering clear of common traps and embracing a well-rounded financial and lifestyle strategy, retirees can build a future that’s not only secure—but rewarding. With thoughtful planning and the right support, this next chapter can be the best one yet.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As we approach the end of 2025, the property insurance marketplace is navigating a mix of change, challenge and opportunity. Here’s a look at the key trends shaping the sector — and what they might mean for insurers, brokers and property owners alike.

1. Climate-Driven Losses Are Now the New Normal

The pace and severity of natural catastrophes continue to place major pressure on the property insurance market. The Swiss Re Institute estimates that global insured losses from natural catastrophes hit roughly US $80 billion in the first half of 2025, nearly double the 10-year average. (Reuters+2Insurance Journal+2) For insurers, that means heavier claims, tougher underwriting decisions and heightened scrutiny of exposures in high-risk zones.

What to watch:

Insurers will increasingly pull back or raise rates in high-catastrophe zones — e.g., coastal and wildfire-prone areas.

Property owners in those zones will receive stronger signals to invest in resilience (storm hardening, wildfire mitigation, flood defence).

Coverage gaps may grow where private insurers no longer provide adequate support, leading to more reliance on state/last-resort markets.

2. Pricing and Coverage Conditions Are Mixed — Softening in Some Segments, Hardening in Others

While recent years were characterised by sharp rate increases and tightening terms, there are signs that some parts of the market are stabilising or even softening. For example:

The Alera Group in its 2025 P&C update notes greater market stability, with disciplined underwriting, improving investment yields, and signs that premium growth may moderate. (Alera Group)

In commercial property, accounts with favourable loss history and limited catastrophe exposure may now see flat to single-digit rate increases, rather than the double-digit hikes of earlier years. (Dominion Risk+1)

On the flip side, in the homeowners/home-insurance space, average premiums remain elevated, and the insurers’ “combined ratio” suggests limited profitability in some segments. (Rate)

Key take-aways:

For well-performing risks, carriers are competing — more capacity, more flexible terms.

Brokers and agents who can help clients demonstrate strong mitigation/maintenance will be in demand.

3. Technology & Risk-Modelling Innovations Are Moving From “Nice to Have” to “Must-Have”

Insurers are rapidly expanding their use of technology — sensors, drones, satellite imagery, IoT monitoring, artificial intelligence — to refine risk assessments, improve underwriting and streamline claims. According to a recent legal-firm insight, insurers are deploying drones, satellite-imagery and IoT to track damage and property condition in real time. (Greenberg Traurig) Meanwhile, homeowners are seeing insurers push risk-mitigation incentives (smart-home sensors, leak detectors, fire-resistant construction) as a way to differentiate risk. (Rate)

What this means:

Risk-differentiation will widen: properties with upgraded resilience features may enjoy better terms/discounts.

Older or non-mitigated properties may face fewer options or harsher terms.

Agents and insurers who embrace these tools will have a competitive edge, especially in emerging hazard-zones.

4. Reinsurance and Capacity Pressures Remain Real

While direct insurance pricing may be moderating for some risks, the broader ecosystem — especially reinsurance — remains under strain. The costs of reinsurance for catastrophe risk continue to climb as global natural hazard exposures grow. (Greenberg Traurig) Also, some last-resort markets (state-backed, residual lines) are under pressure to raise rates or adjust eligibility, particularly in states with chronic exposure. (San Francisco Chronicle)

Implication: Insurers must manage their reinsurance treaties carefully, be selective about exposures they carry, and pass through appropriate pricing and terms to stay sustainable.

5. Market Size is Growing — With Geographic and Product Gaps Emerging

From a volume perspective, the property-insurance market remains on a growth path. For example, in North America the market for property insurance was projected to reach about US $365 billion in 2025, with a five-to-seven-year compound annual growth rate (CAGR) of nearly 7%. (Statista) Globally, a report projects the property-insurance market to be around US $364.75 billion in 2025, growing toward ~US$591 billion by 2034. (Business Research Insights)

Yet, growth is uneven:

Regions with escalating risk (wildfire, flood, storm) may struggle with supply and affordability.

Specialized products (wildfire-only, flood-only, resiliency add-ons) are gaining traction.

Bundled products (home + auto) and value-added services (risk-engineering, smart-home upgrades) are becoming differentiators.

6. Homeowners Face Increasing Burden — Affordability, Availability and Risk

For homeowners, especially in climate-exposed states (e.g., coastal Florida, wildfire-prone California), the challenges are mounting:

Rising premiums and deductibles: some reports show average home-insurance premiums nationally up ~20 % year-over-year in certain markets. (Rate+1)

Higher deductibles and more peril-specific deductibles (wind/hail, wildfire, flood) are becoming more common. (Matic Insurance)

Coverage availability is still strained in many high-risk ZIP codes; the E&S (Excess & Surplus) market is filling gaps. (Matic Insurance)

For agents and homeowners:

Risk mitigation (roof upgrades, fire-resistant landscaping, flood mitigation) is no longer optional—it can materially affect access and cost of coverage.

The choice of market (traditional carrier vs. surplus market) matters more than ever; early renewal/placement is advised.

For homeowners in highly exposed zones, budgeting for rising insurance costs (and potential policy non-renewals) is prudent.

7. Regulatory & Geographic Regulation Shifts

Regulators in states like Hawaii, Florida and California are responding to the stability challenges in property-insurance markets. For example, in Hawaii legislators pledged efforts to stabilise the market in the face of rising rates and insurers pulling out. (AP News) Rate filings and underwriting criteria adjustments are happening in several jurisdictions — meaning agents must stay abreast of local regulatory changes that could affect availability, coverage form, or premium.

Looking Ahead to Late 2025 and Early 2026

As we close out 2025, a few strategic themes for stakeholders:

For insurers and brokers: Market segmentation will deepen. Strong, well-mitigated risks will benefit from capacity and competition. Weakly mitigated risks will face greater terms and possibly coverage erosion.

For homeowners/property owners: Now is a contact point: review your property’s risk profile, invest in mitigation where possible, explore multiple carriers, and monitor renewal dates early.

For agents in your position (auto/property insurance): There’s an opportunity to advise clients on the “property side” in addition to auto — helping them understand risk exposures, mitigation, bundling opportunities, and market shifts. For example, bundling home + auto may give you more leverage.

For regulatory watchers: The interplay of climate risk, insurance affordability, and public policy will remain front-and-centre. Watch for state-level reforms, changes in last-resort insurers, and potential new coverage mandates or premium subsidies.

What Lies Ahead

The property-insurance market at the end of 2025 is in a state of transition. Big picture: demand is growing, but risk is mounting and not evenly distributed. Pricing and terms are moderating in some segments — yet for high-exposure zones the pressure remains acute. Technology, mitigation and geographic nuance will distinguish winners from laggards.

For you (and your clients) this means: be proactive. Know the risks. Position properties (or clients’ homes) for reward (through mitigation) rather than punishment. And stay flexible — the “next renewal” is likely to look quite different from the last.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

As daylight fades and drivers take to the roads after sunset, the risks rise dramatically. According to the National Safety Council, the fatal crash rate at night is about three times higher than during the day. Despite making up only a small portion of total driving time, nighttime driving accounts for nearly 50% of all traffic deaths in the United States each year.

Experts point to one primary reason: reduced visibility. Even with streetlights and modern vehicle technology, the human eye struggles in low-light conditions. But what many drivers don’t realize is how much their own vehicle’s headlights can contribute to the danger.

Over time, headlight lenses become cloudy or yellowed from oxidation, cutting light output by as much as 50%. Bulbs can also dim gradually, often without the driver noticing, and misaligned headlights may shine too low or too high, limiting visibility or blinding oncoming traffic.

“Headlights are your first line of defense at night,” says a local automotive safety technician. “Keeping them clean, bright, and properly aimed can make the difference between spotting a hazard in time or not at all.”

Regular maintenance—such as cleaning lenses, checking bulb brightness, and ensuring correct alignment—can dramatically improve safety. Replacing bulbs in pairs and restoring headlight covers can also restore lost visibility and reduce glare for others.

Drivers should also be mindful of when they’re on the road. Statistics show that the hours after midnight are the most dangerous, as fatigue, alcohol impairment, and reduced alertness peak. For the safest travel, experts recommend getting home before midnight whenever possible.

In short, maintaining your headlights isn’t just about looks—it’s about safety. As nights grow longer, take a few minutes to check your car’s lights. It could be one of the simplest ways to protect yourself and everyone else on the road.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

When it comes to homeowners insurance, accuracy is everything. One of the most critical tools used to protect your biggest investment is the Replacement Cost Estimator (RCE)—a system that helps determine how much it would actually cost to rebuild your home from the ground up after a covered loss. Unfortunately, many homeowners underestimate their home’s true value, leading to painful surprises when disaster strikes.

The RCE takes into account today’s construction costs, materials, labor, and local building codes to calculate an accurate rebuilding cost—not the market price of your home. With inflation in construction and fluctuating material prices, relying on outdated or ballpark figures can leave you dangerously underinsured. If your policy doesn’t reflect your home’s current replacement cost, you could end up paying tens—or even hundreds—of thousands—out of pocket after a total loss.

It’s not just the structure that matters. Personal property coverage—the protection for your belongings like furniture, electronics, and clothing—should also reflect their true replacement value. Too often, people underestimate what it would take to replace everything they own. And don’t overlook loss of use coverage, which helps pay for temporary housing and living expenses if your home becomes uninhabitable. Skimping on this area could make a tough situation even harder if you’re displaced for months during repairs.

The bottom line: an accurate RCE ensures your dwelling, personal property, and loss of use coverages keep pace with reality. Take time to review your policy annually, ask your agent to update your RCE, and avoid the false comfort of being “covered” for less than what you’d actually need. When life’s unexpected moments happen, being properly insured is what helps you rebuild—not just your home, but your peace of mind.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.