Amid busy schedules, constant digital noise, and everyday stressors, the pursuit of true happiness remains a timeless quest. While philosophers, poets, and leaders throughout history have debated the meaning of joy, many have also offered words of wisdom that continue to inspire generations.

Here are ten quotes to embrace true happiness, reminding us that contentment often lies in perspective rather than possessions:

Aristotle – “Happiness depends upon ourselves.” A reminder that joy is cultivated from within, not handed to us by circumstance.

Dalai Lama – “Happiness is not something ready-made. It comes from your own actions.” Echoing the idea that daily choices and kindness shape our state of mind.

Eleanor Roosevelt – “Happiness is not a goal… it’s a by-product of a life well lived.” Joy emerges as a natural result of living with purpose and integrity.

Albert Schweitzer – “Happiness is nothing more than good health and a bad memory.” A humorous yet practical perspective on letting go of the past and valuing well-being.

Victor Hugo – “The supreme happiness of life is the conviction that we are loved.” Happiness often thrives in the warmth of human connection.

Marcus Aurelius – “Very little is needed to make a happy life; it is all within yourself.” A Stoic truth that joy is less about excess and more about appreciation.

Audrey Hepburn – “The most important thing is to enjoy your life—to be happy—it’s all that matters.” A simple yet profound truth from a timeless icon.

Mahatma Gandhi – “Happiness is when what you think, what you say, and what you do are in harmony.” Alignment of values and actions remains key to peace of mind.

Buddha – “There is no path to happiness: happiness is the path.” A spiritual perspective emphasizing that joy is a way of living, not a final destination.

Ralph Waldo Emerson – “For every minute you are angry you lose sixty seconds of happiness.” A gentle reminder to choose joy over resentment.

Taken together, these insights highlight that happiness is less about external gains and more about cultivating gratitude, love, simplicity, and authenticity. In today’s fast-paced society, pausing to reflect on these words may help us rediscover the power of joy in everyday life.

As I’ve gotten older, I’ve realized that taking care of my mind is just as important as taking care of my body. It’s not just about preventing memory lapses; it’s about staying sharp, curious, and engaged with life. Over the years, I’ve adopted several habits that I truly believe have helped me keep my brain in good shape—and the science backs it up.

Exercise Is My Non-Negotiable I’ve found that moving my body daily, whether it’s a brisk walk, yoga, or light weightlifting, doesn’t just keep me physically fit—it clears my mind. Research shows that exercise increases blood flow to the brain and encourages the growth of new brain cells. I can feel the difference in my focus and energy on the days I move versus the days I don’t.

Food as Brain Fuel What I eat has changed a lot. I’ve cut back on processed foods and leaned more into fresh vegetables, fruits, nuts, and fish. The Mediterranean diet, which many doctors recommend, isn’t just about longevity—it’s about mental clarity. When I eat clean, my thoughts feel sharper and my mood steadier.

Protecting My Sleep In my younger years, I thought burning the candle at both ends was normal. Now, I treat sleep like medicine. Deep sleep helps my brain “clean house,” and when I get a solid 7–8 hours, my memory and problem-solving are noticeably better.

The Power of People I’ve learned that socializing isn’t just about fun—it’s brain protection. Conversations, laughter, and community keep me engaged and emotionally balanced. Isolation, on the other hand, makes my mind feel sluggish.

Challenging My Mind Daily Reading books, doing puzzles, or even trying to learn new skills keeps my brain on its toes. Recently, I started learning a new language—it’s humbling, but I can feel my brain stretching in ways it hasn’t in years.

Managing Stress the Hard Way Stress used to be my constant companion. Over time, I noticed how it clouded my judgment and wore me down mentally. Now, I practice mindfulness and deep breathing. Even a few minutes of stillness in the morning changes how my entire day feels.

Checking In on My Health Finally, I don’t ignore routine checkups anymore. Managing blood pressure, cholesterol, and overall health directly affects brain health. I’ve seen too many people neglect this, only to face cognitive issues later in life.

At the end of the day, brain health is not about one magic trick—it’s about small, consistent habits. For me, it’s a mix of movement, nourishment, rest, connection, curiosity, peace of mind, and medical awareness. And I can honestly say, these practices make me feel sharper, more alive, and ready for whatever comes next.

When I think about the biggest changes I’ve made to improve my health, sports are at the top of the list. For me, playing and staying active isn’t just about competition—it’s about feeling stronger, clearer, and more energized in my daily life.

Over the years, I’ve noticed how much better I feel when I make time for sports. My body is healthier, my mind is sharper, and even my outlook on life improves. The more I commit to staying active, the more I see the benefits build on each other.

What Sports Do for Me (and Can Do for You)

Here are some of the ways sports have made a positive impact on my health:

Boost my heart health – I can feel the difference in my stamina and endurance.

Build stronger muscles and bones – Staying active has helped me feel stronger and more balanced.

Help me manage weight – Playing sports burns off stress (and calories) at the same time.

Improve my flexibility and coordination – I move better and feel less stiff.

Reduce my stress and anxiety – There’s nothing like the mood boost after a good workout or game.

Help me sleep better – When I stay active, I fall asleep faster and rest deeper.

Strengthen my immune system – I notice I get sick less often.

Give me social connections – Team sports especially help me bond with others and feel part of something bigger.

Sharpen my focus – I concentrate better and make clearer decisions.

Add years to my life – Staying active makes me feel younger and healthier every day.

Why I Keep Playing

For me, sports are more than exercise—they’re a way to build confidence, relieve stress, and invest in my future health. No matter your age or skill level, there’s a sport out there for you. The key is finding something you enjoy and sticking with it.

I’ve learned that when I make time for sports, I’m not just playing a game—I’m building a better version of myself. And you can too.

Success is often measured in numbers—bank accounts, investments, or even social media followers—the deeper meaning of being both healthy and wealthy can sometimes get lost. For me, the phrase isn’t about chasing material excess, but about balance, fulfillment, and sustainability in both body and mind.

Health as the Foundation Health is more than the absence of illness; it’s the daily practice of treating your body and mind with respect. For me, that includes maintaining energy to do the things I love, fueling my body with good food, and taking time to reduce stress. Without health, even the greatest fortune feels empty. Wealth is meaningless if you don’t have the strength or clarity to enjoy it.

Wealth Beyond Money When I think of being “wealthy,” I don’t immediately picture luxury cars or sprawling mansions. Instead, I see freedom—the freedom to spend time with loved ones, pursue passions, and give back to the community. True wealth, to me, includes financial security, but also peace of mind, strong relationships, and opportunities to grow.

Healthy and Wealthy Together The two go hand in hand. Being healthy allows me to work toward financial stability with focus and determination. Being financially stable allows me to invest in my health—whether that’s quality healthcare, nutritious food, or the ability to take time off when I need it. Together, they create a cycle that builds not just a lifestyle, but a legacy.

A Personal Vision Ultimately, “healthy and wealthy” means living in a way that supports long-term happiness. It’s about waking up each day with energy, knowing I have the resources to handle life’s challenges, and feeling grateful for both the small and big wins. To me, that’s real success—being rich in health, rich in love, and rich in purpose.

As the sun rises on another Labor Day weekend, I can’t help but reflect on what this holiday really means to me. For most, it’s barbecues, beach trips, or one last long weekend before fall routines take over. But for me, Labor Day always feels like a bookmark—closing one chapter and opening another.

Summer has its own rhythm. The long days, the warmth, the freedom to move at a slower pace. Whether it’s evenings spent outside, family get-togethers, or just the simple joy of not having to rush through life, summer always seems to remind us that there’s more to living than just schedules and obligations.

Labor Day weekend, though, comes with a quiet shift. You feel it in the air—cooler mornings, earlier sunsets, a subtle reminder that fall is just around the corner. It’s not sad, exactly, but it does feel like the end of something special. Almost like the universe nudging us to reset, regroup, and get ready for what’s next.

For me, this weekend is less about mourning summer and more about appreciating it. I think about the memories made, the laughs shared, and the little adventures tucked in between ordinary days. Then I start looking forward to what fall brings: a new sense of focus, cooler weather, football season, and maybe even the motivation to chase down goals I let simmer over the summer months.

Labor Day is a reminder that every season has its purpose. Summer is about energy and freedom; fall is about discipline and progress. The balance between the two keeps life moving in the right direction. And so, while I say goodbye to summer with a smile, I also say hello to what’s next—with the same optimism that every new season deserves.

When it comes to protecting wealth and passing it on to loved ones, many families are discovering that a simple will may not be enough. Increasingly, individuals are turning to trusts as a more effective way to manage their assets and provide security for beneficiaries. While wills remain common, trusts offer unique advantages that make them an essential tool in modern estate planning.

A trust is a legal arrangement in which a trustee manages assets on behalf of beneficiaries. Unlike a will, which becomes public during probate, a trust can keep family financial matters private while ensuring assets are distributed according to the grantor’s wishes.

Avoiding Probate Delays and Costs One of the main reasons individuals choose a trust is to avoid probate—the court-supervised process of distributing an estate after death. Probate can take months or even years, and legal fees can significantly reduce what heirs actually receive. With a trust, assets are transferred more quickly and with fewer administrative costs.

Tax Efficiency and Asset Protection Certain types of trusts can also provide tax advantages. For high-net-worth individuals, this can mean minimizing estate taxes, while others use trusts to shield assets from creditors or lawsuits. Parents of minor children often create trusts to ensure their children’s financial needs are met in the event of an untimely death.

Control Over Distribution Unlike a will, which typically results in a lump-sum transfer of assets, a trust allows for customized distribution. For example, beneficiaries can receive funds at certain ages, in installments, or for specific purposes such as education or healthcare. This level of control provides peace of mind for those worried about heirs’ financial responsibility.

Peace of Mind for Families “Trusts aren’t just for the wealthy,” says estate planning attorney Sarah Mitchell. “They’re tools that provide structure, protection, and clarity—things every family can benefit from. For many clients, it’s about peace of mind knowing their loved ones are taken care of.”

As life expectancy increases and wealth is passed down through generations, experts predict that more families will explore trusts as part of their financial planning. Whether it’s avoiding probate, protecting assets, or ensuring responsible inheritance, trusts are becoming a cornerstone of modern estate planning.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

When it comes to motorcycles, boats, golf carts, and ATVs, most people think about the thrill of the ride, the open water, or a sunny day on the course-not the financial risks. But accidents, theft, and unexpected liabilities don’t take a holiday, and that’s why insurance for your recreational “toys” is worth serious consideration.

Required vs. Optional Coverage

The first step in understanding toy insurance is knowing what’s required by law and what’s optional.

Motorcycles: Like cars, most states require liability insurance if you’re taking your motorcycle on public roads. This covers injury or damage you may cause to others, but not your own bike. Collision and comprehensive coverage—protecting your motorcycle against accidents, theft, or weather damage are optional but highly recommended.

Boats: While boat insurance isn’t federally mandated, some states and marinas require proof of coverage. Even if it’s not required, carrying liability and property protection can shield you from costly repairs or lawsuits if an accident occurs on the water.

ATVs & Dirt Bikes: If you’re riding on private land, insurance is usually optional. However, many state parks, trails, and off-road areas require proof of coverage to operate. Considering the high rate of ATV accidents and theft, insuring your four-wheeler is a smart move.

Golf Carts: Most neighborhoods and golf courses don’t require golf cart insurance, but if you’re using the cart on public roads-or even just around your community-liability coverage can protect you if an accident happens. Some homeowners’ policies provide limited coverage, but standalone golf cart insurance can fill the gaps.

Why You Should Insure Even When It’s Optional

Just because coverage isn’t required doesn’t mean it isn’t essential. Repair costs, medical bills, or liability lawsuits can quickly outweigh the value of your toy itself. Theft is another growing concern-ATVs, motorcycles, and even boats are among the most commonly stolen recreational vehicles.

Insurance not only protects your investment but also your financial stability. For many, the peace of mind of knowing that a fun weekend won’t turn into a financial nightmare is worth the modest premium.

A Smarter Way to Protect Your Fun

Your recreational vehicles are more than just “toys”-they’re part of your lifestyle. Adding the right insurance ensures that your good times don’t come with unnecessary risks. Before the next ride, round of golf, or day on the water, check your coverage and make sure your adventures are backed by protection as strong as your passion.

About the Author:

David Dandaneau is a client relations analyst that covers the insurance and financial services industry. He is known for his insightful analysis and comprehensive coverage of market trends and regulatory developments.

Life in our home just got a little more exciting. We recently welcomed a new cat into the family, which now brings us to three cats and one dog. It’s a full house, and while it means more food dishes, more fur on the couch, and a bit more chaos, I can already feel the positive impact on my mental health.

For me, pets are more than just companions-they’re a steady source of comfort and joy. On stressful days, there’s something grounding about a cat curling up in my lap or the dog nudging me for a walk. Each animal adds a different type of support. The cats bring a sense of calm, their quiet purrs easing my anxiety, while the dog encourages me to stay active and present.

I’ve noticed that with multiple pets, the benefits seem to multiply. There’s always a warm presence in the house, always a reminder that I’m not alone. It keeps me connected, responsible, and often laughing at their playful antics. Science backs this up too-studies show pets can reduce stress, ease depression, and even help create structure in daily life.

Of course, caring for four animals comes with challenges. It requires patience, time, and commitment. But the rewards-companionship, unconditional love, and a boost to my overall well-being-far outweigh the effort.

As I adjust to life with our newest cat, I’m reminded how much these animals give back. In a world that can feel overwhelming at times, their presence is a gentle reminder that joy can be found in small, furry packages. For me, a purr or a wagging tail isn’t just cute… it’s therapy.

Airbnb delivered $11.1 billion in revenue for 2024, marking a 12% year-over-year increase, driven by higher booking volume and sustained average daily rates. Gross booking value surged to $81.8 billion (+10.6% YoY), while free cash flow hit $458 million in Q4 (18% margin) (AInvest).

Moreover, Airbnb’s global market share in short-term rentals climbed to 44% in 2024, up from 28% in 2019—far ahead of Booking.com (18%) and Expedia/Vrbo (9%) (AInvest).

2. Efficient Asset-Light Business Model

Airbnb’s strategy avoids owning properties, enabling high-margin operations. Their gross margin soared to approximately 83% in early 2024 (The Motley Fool), and their asset utilization metrics demonstrate tightening efficiency. Notably, the net fixed-asset turnover leaped from 12.5 in 2020 to 75.5 in 2024, reflecting strong revenue delivery with minimal asset base (Stock Analysis on Net).

3. Strategic Diversification into Services & Experiences

In recent quarters, Airbnb has repositioned itself beyond homestays into an integrated travel ecosystem-offering localized experiences, services like spa treatments, personal training, and lodging alternatives-all within its revamped app ecosystem (AInvestMarketWatch).

This diversification is not trivial: management projects that the “Services & Experiences” vertical could generate $1 billion in annual revenue within 3–5 years, backed by a $200–250 million investment earmarked for 2025 (AInvestMarketWatch).

4. Recent Strong Earnings Momentum

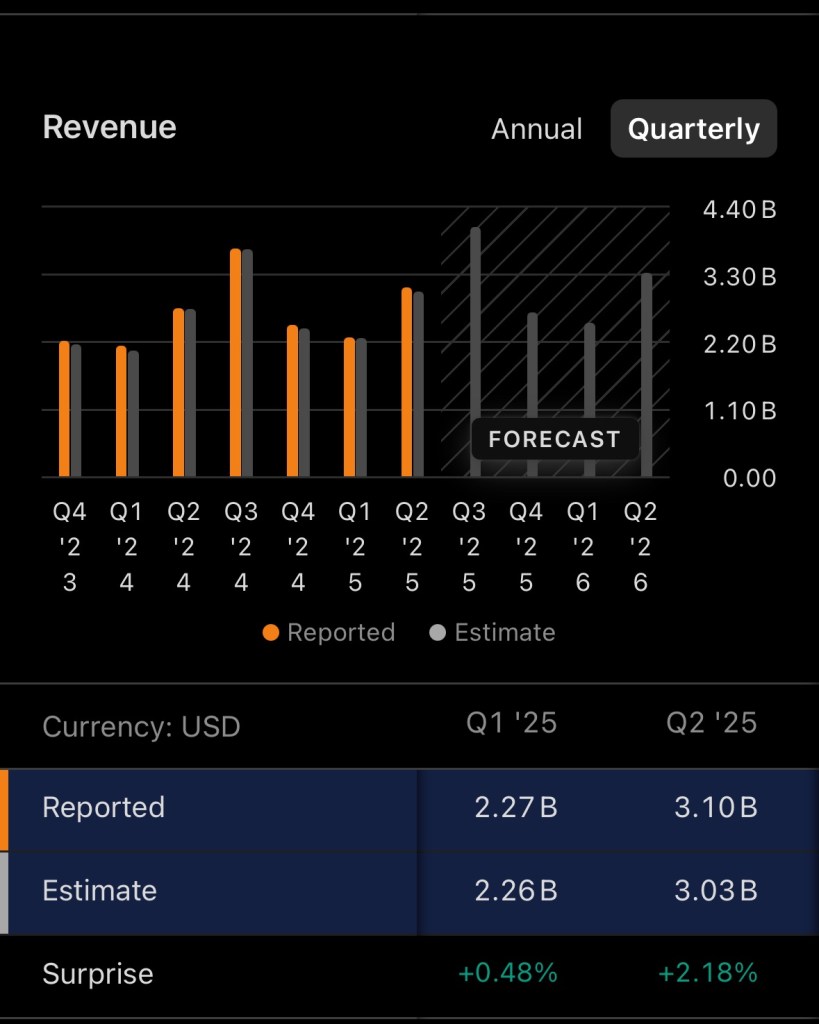

Airbnb outperformed expectations in Q2 2025:

Earnings per share: $1.03 (+99% YoY vs. $0.94 expected)

Revenue: $3.1 billion (+13% YoY)

Gross bookings: $23.5 billion (+11% YoY)

Despite these strong results, caution around margin trajectory and investment pace weighed on sentiment, causing a ~7% dip in premarket trading Investors.

Simultaneously, long-term confidence remains steady-Akre Capital boosted its Airbnb allocation by 10%, signaling belief in the company’s growth trajectory (AInvest).

5. Favorable Industry Trends

In the broader travel space, analysts remain positive. A recent Barron’s feature highlights secular travel growth outpacing GDP and the rising demand for experiences. Although other travel players like hotels and airlines benefit, OTAs and platforms like Airbnb must adapt and diversify to stay competitive-something Airbnb is actively doing (Barron’s).

Industry Positioning: How Airbnb Compares

Here’s a snapshot comparing Airbnb to its main competitors in the travel lodging and experiences sector:

Company

Market Share (2024)

Business Model

Key Differentiator

Airbnb

44%

Asset-light platform

Large host network, high margins, diversified services

Booking.com

18%

Hybrid (hotels + rentals)

Strong hotel partnerships, AI integration

Expedia/Vrbo

9%

Hybrid OTA

Bundle offerings, traditional OTA presence

Airbnb leads clearly in short-term rental share and continues to build stronger differentiation through vertical integration and digital enhancements (AInvest+1MarketWatchBarron’s).

Points of Caution

Valuation: Forward P/E sits above 30x (e.g., ~34.5x), relatively high compared to peers like Expedia (~10x) or Booking (~18x) (The Motley FooleToro).

Regulatory Headwinds: Local restrictions (e.g., New York City) and evolving laws could curtail growth in certain markets (eToroMarketWatch).

Execution Risk: Scaling new offerings and achieving the $1 billion services target will take time—short-term margins may remain under pressure (AInvestInvestorsMarketWatch).

Final Take

Airbnb demonstrates the hallmarks of a high-upside, long-term growth stock:

Strong financials, efficient operations, and leading share in a growing market.

Expanding revenue streams beyond traditional listings.

Strategic execution evidenced by earnings beats and fund manager conviction.

That said, elevated valuation and near-term execution risks suggest that patient investors may benefit from disciplined entry points or staged allocation.

Disclaimer: The author holds a position in $ABNB AIR BNB and this article should not be considered financial advice. Always conduct your own research before making any investment decisions.

As August rolls on, I’m preparing for a major life shift-sending not one, but two kids off to college.

This fall, my daughter will begin her journey as a freshman at Florida Gulf Coast University (FGCU), ready to explore a new chapter in the sunshine-filled town of Fort Myers. Meanwhile, my son is entering his second year at the University of South Florida (USF), well on his way toward earning his degree and carving out his own path.

I’m incredibly proud of both of them. But I’d be lying if I said it wasn’t bittersweet.

The house that once echoed with teenage chatter, shared meals, and last-minute school deadlines is starting to feel a little quieter-and emptier.

I’ve been bracing for the ‘empty nest’ for a while. And now that it’s actually happening, it feels surreal.

Watching Their Independence Take Flight

One of the most rewarding parts of parenting-yet also the most emotional-is watching your kids grow into their independence. It’s happening right before my eyes. They’re making decisions for themselves, solving their own problems, setting their own goals. And while I’ll always be their biggest cheerleader, I know this next stage is about them leading their own lives.

My daughter is eager to make new friends, figure out her place in the world, and maybe even learn how to do laundry without help. My son is more confident this year-he’s navigating his classes, campus life, and adulthood with a little more ease. It’s a beautiful thing to witness, even if it tugs at my heart.

This growing independence doesn’t mean I’m any less involved. It just means I’m learning how to support them from a different seat-more in the stands now than on the field.

While emotions are running high, so is the excitement. My daughter is already shopping for dorm supplies and dreaming of beachside study breaks, while my son is eager to reunite with friends and dive deeper into his major at USF.

Still, the looming quiet at home is a reality that’s setting in fast.

Everything is changing-the routines, the conversations-it’s all shifting. I’ll miss them deeply, but this is their time to soar.

As the suitcases pile up and the goodbyes draw near, one thing is clear: while my nest may be emptying, my heart is fuller than ever-with love, pride, and hope for what’s ahead.