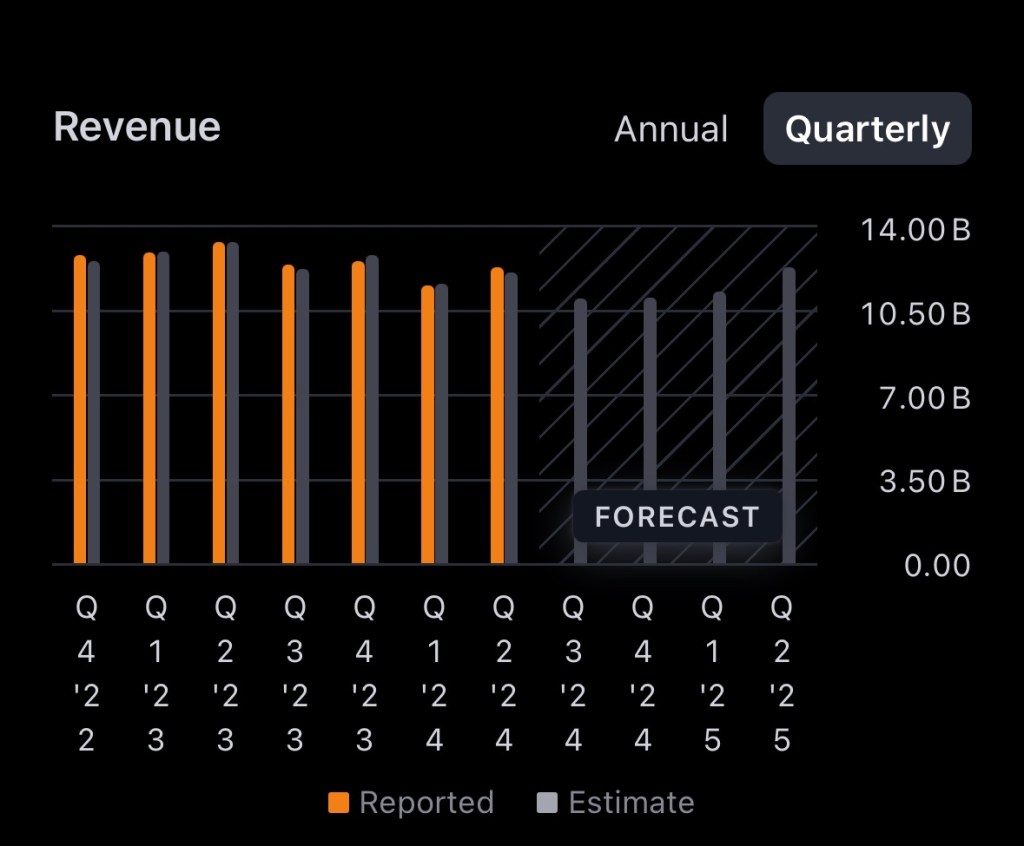

United Parcel Service (UPS) has recently experienced a significant decline in its stock value, with shares dropping over 16% following the announcement of a strategic shift to reduce its business with Amazon by more than 50% by the second half of 2026. This decision is part of UPS’s broader strategy to focus on more profitable segments, such as healthcare logistics and business-to-business deliveries, aiming to improve profit margins and reduce dependency on Amazon.

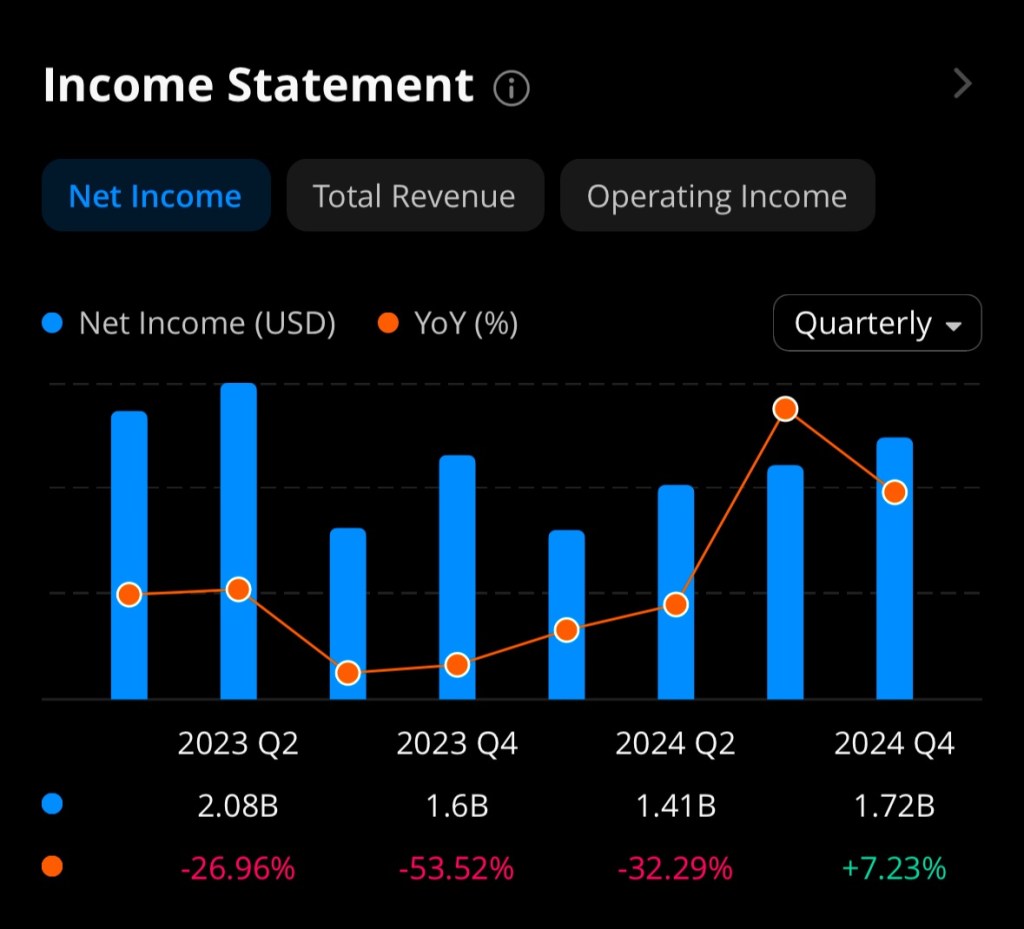

Despite the immediate negative market reaction, some analysts view this move as a positive step for UPS’s long-term profitability. By decreasing reliance on high-volume, low-margin shipments from Amazon, UPS plans to enhance operational efficiency and focus on higher-margin businesses. This strategic pivot is expected to save the company approximately $1 billion annually.

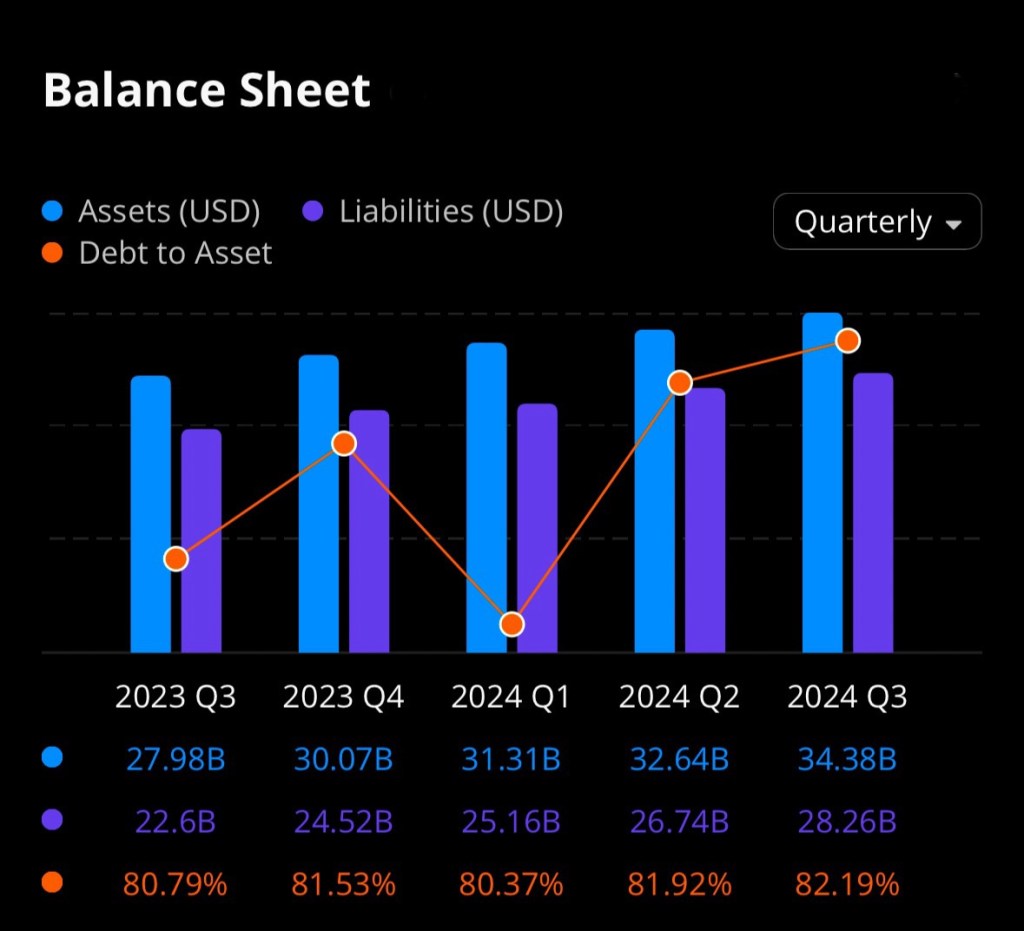

Additionally, UPS’s decision to insource operations previously handled by the U.S. Postal Service, such as the SurePost product, is aimed at optimizing service and reducing costs. While these changes may present short-term challenges, they are designed to position the company for sustainable growth and improved profitability in the future.

For long-term investors, UPS’s current stock decline may present a buying opportunity. The company’s strategic initiatives to focus on higher-margin segments and reduce operational dependencies are expected to strengthen its market position over time. While the transition may involve near-term uncertainties, UPS’s efforts to enhance profitability and operational efficiency could lead to substantial long-term gains for patient investors.

Disclosure: I currently hold a position in United Parcel Service ($UPS). This article reflects my personal opinions and analysis, and is not intended as financial advice. Please conduct your own research or consult a financial advisor before making any investment decisions.

References

Barron’s. (2024, January 30). UPS and Amazon may be headed for a split—and the stock is paying the price. Retrieved from https://www.barrons.com/articles/ups-earnings-stock-price-amazon-1a32be4f

Business Insider. (2025, January 30). UPS plunged after saying it would deliver fewer Amazon packages. Its CEO says it’s about ‘taking control of our destiny.’ Retrieved from https://www.businessinsider.com/ups-ship-fewer-amazon-packages-shares-drop-2025-1

Investopedia. (2024, January 30). UPS Q4 earnings report FY2024. Retrieved from https://www.investopedia.com/ups-earnings-q4-fy2024-8780982

MarketWatch. (2024, January 30). UPS’s stock falls after a revenue miss, deal with largest customer to cut volume. Retrieved from https://www.marketwatch.com/story/upss-stock-falls-after-a-revenue-miss-deal-with-largest-customer-to-cut-volume-1984fcb7

The Motley Fool. (2025, January 30). Why UPS stock is plunging today. Retrieved from https://www.fool.com/investing/2025/01/30/why-ups-stock-is-plunging-today

The Wall Street Journal. (2024, January 30). UPS’s boss is under pressure from unhappy investors—its own retirees. Retrieved from https://www.wsj.com/business/logistics/upss-boss-is-under-pressure-from-unhappy-investorsits-own-retirees-f01a8dd3