In an era where financial stability and long-term planning are paramount, universal whole life insurance emerges as a beacon of security for individuals and families alike. This form of insurance offers a comprehensive package that not only provides death benefits but also serves as a strategic financial tool during one’s lifetime. Let’s delve into the benefits that make universal whole life insurance a valuable asset in today’s uncertain world.

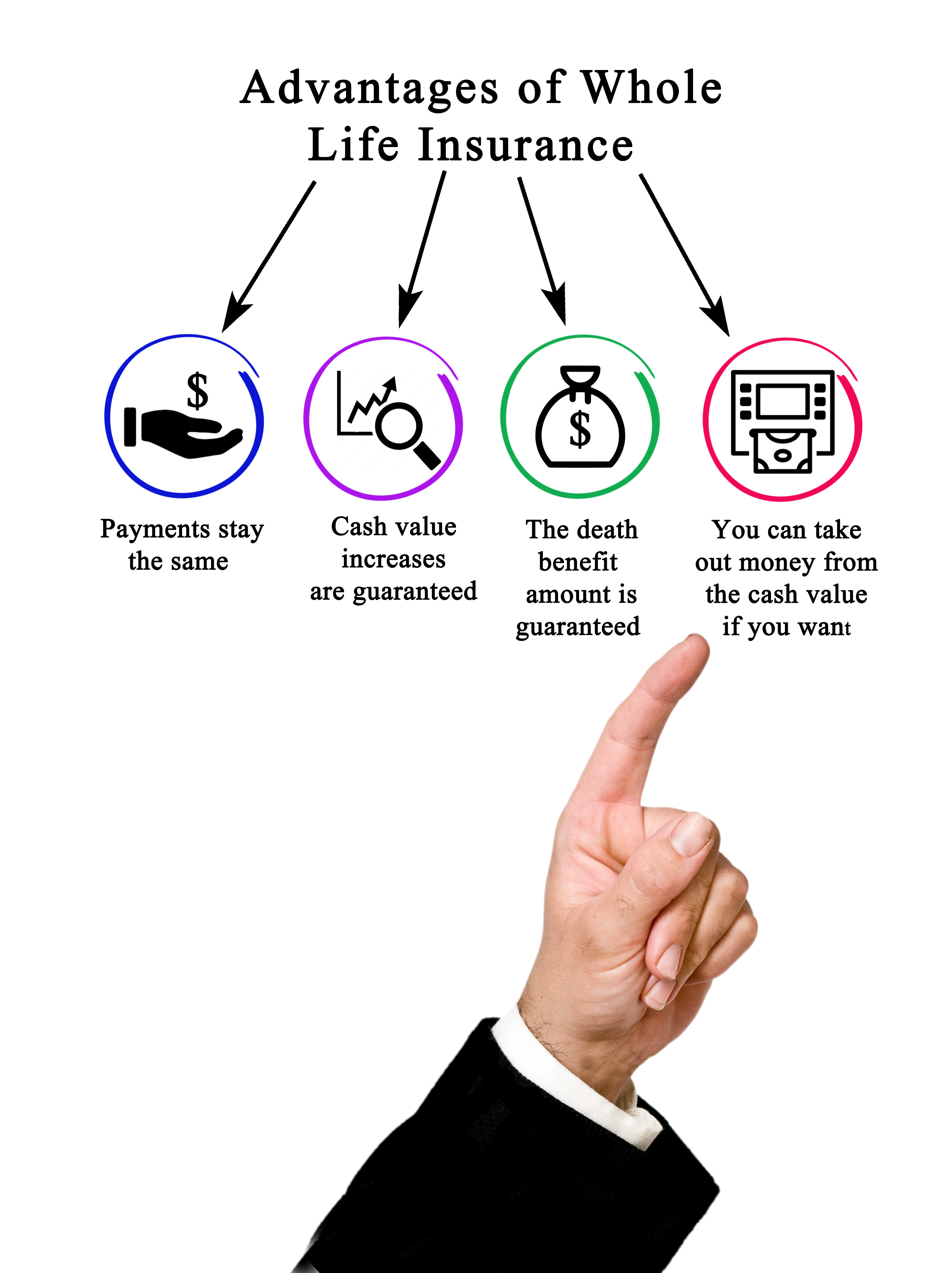

1. Lifetime Coverage: Unlike term life insurance, which covers a specific period, universal whole life insurance guarantees coverage for the entirety of one’s life. This permanence ensures that loved ones are provided for regardless of when the policyholder passes away, offering peace of mind and stability to families.

2. Cash Value Accumulation: One of the most appealing aspects of universal whole life insurance is its cash value component. A portion of the premiums paid accumulates as cash value over time, which policyholders can access through loans or withdrawals. This feature serves as a financial safety net, offering liquidity and flexibility during emergencies or to supplement retirement income.

3. Tax Advantages: The tax benefits associated with universal whole life insurance further enhance its appeal. The cash value growth within the policy is tax-deferred, meaning that policyholders are not required to pay taxes on the earnings until they withdraw them. Additionally, death benefits are typically received by beneficiaries tax-free, providing a substantial financial advantage to heirs.

4. Estate Planning Tool: Universal whole life insurance is a powerful tool for estate planning. It allows policyholders to transfer wealth to future generations efficiently, as the death benefit bypasses the probate process, ensuring a smooth and timely transfer of assets to beneficiaries. Moreover, the liquidity provided by the policy can help cover estate taxes and other expenses, preserving the integrity of the estate.

5. Financial Security and Stability: In an unpredictable world, universal whole life insurance offers a sense of financial security and stability. It provides a guaranteed death benefit, ensuring that loved ones are protected financially in the event of the policyholder’s passing. Moreover, the cash value component can be utilized to weather financial storms or pursue opportunities without compromising long-term goals.

Universal whole life insurance stands as a pillar of financial strength, offering comprehensive coverage, cash value accumulation, tax advantages, and estate planning benefits. In an uncertain world, having a reliable financial plan is essential, and universal whole life insurance provides individuals and families with the security and peace of mind they need to navigate life’s journey with confidence.

As always, individuals interested in purchasing insurance should consult with a qualified financial advisor to determine the most suitable options based on their unique circumstances and financial goals. Or if I can help you decide what coverage is best for your particular situation, please reach out, drop me a line or give me a call and I will be happy to assist you.